Case 1: CCIR to KYIV

Kyivstar Group (KYIV): Ukraine's Telecom Titan

Kyivstar Group (NASDAQ: KYIV) is Ukraine's largest telecommunications operator and the first pure-play Ukrainian enterprise to list on the US NASDAQ. While its core telecom business firmly holds the number one market position, its digital ecosystem—encompassing Uklon mobility, Helsi healthcare, Tabletki pharmacy, and Kyivstar TV streaming—is accelerating its transformation from a conventional operator into a comprehensive "digital platform."

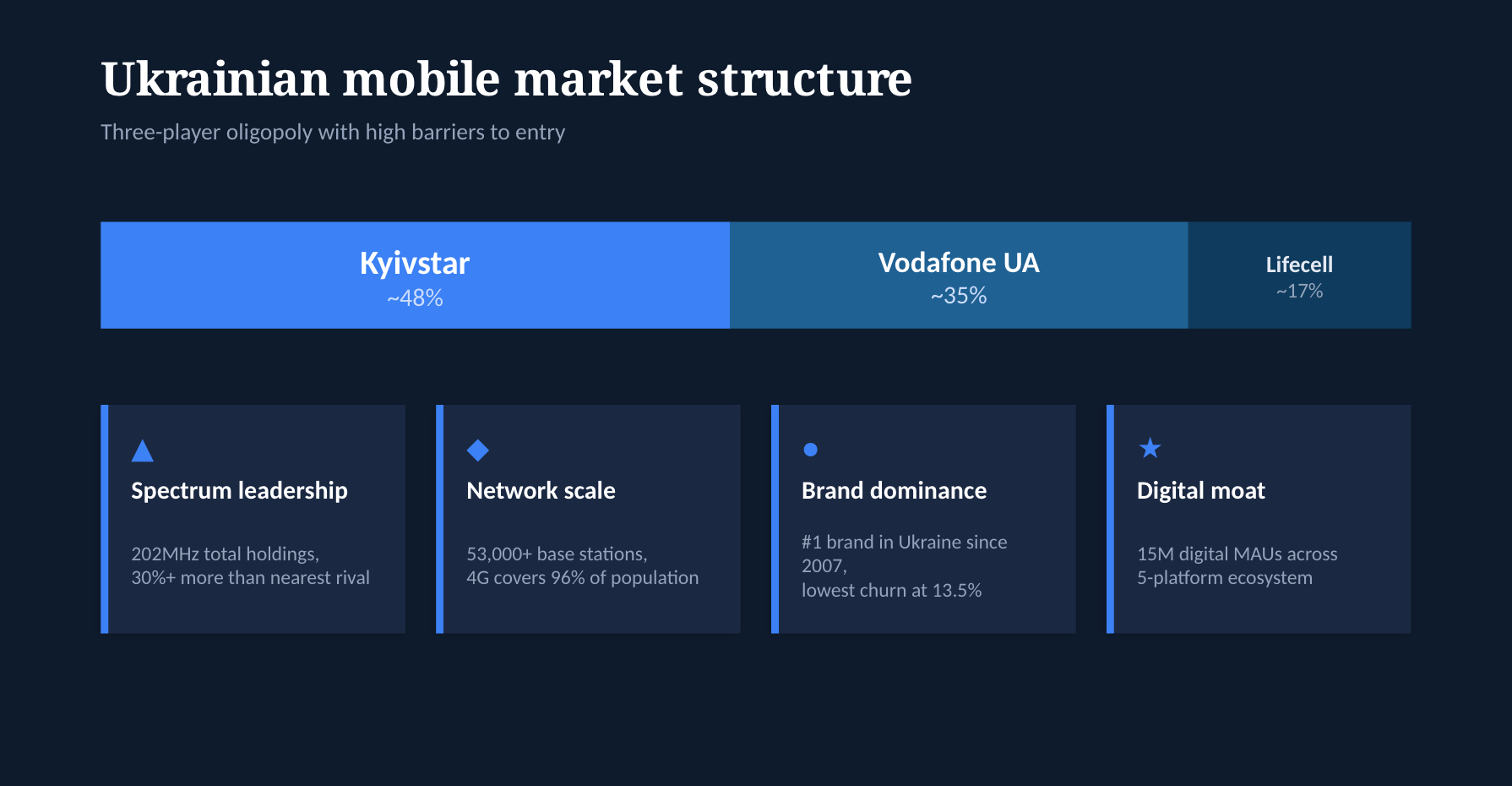

The Ukrainian mobile communications market is characterized by a three-player oligopoly. Kyivstar maintains its dominant lead with approximately 47% market share, followed by Vodafone Ukraine (NEQSOL/Azerbaijani holding) with about 35%, and Lifecell (Xavier Niel's NJJ consortium) at roughly 17%. Together, the top three operators serve over 47.5 million mobile subscribers.

The ongoing war has profoundly altered the market landscape: approximately 6 million Ukrainians have fled abroad, 3.5 million are internally displaced, and roughly 5 million residing in Russian-occupied territories have transitioned to Russian operators. Consequently, the total mobile subscriber base has contracted from its 2013 peak of 60.8 million to the current 47.5 million. Despite these headwinds, Kyivstar has successfully preserved its market dominance by leveraging superior network coverage and robust brand loyalty.

Genesis and Historical Evolution

Founded in 1994 under the nascent name "Bridge" by Ukrainian entrepreneurs including Ihor Lytovchenko, Kyivstar officially commenced commercial operations upon completing its inaugural call on December 9, 1997. During an era when the average Ukrainian monthly salary was less than $100 and mobile connection fees hovered at an exorbitant $850, the company capitalized on aggressive network expansion and brand cultivation. It rapidly ascended to become Ukraine's foremost mobile operator, earning the accolade of Ukraine's most valuable brand by 2007.

2009-2010 marked a pivotal juncture: Norway's Telenor and Russia's Alfa Group (via Altimo) brokered an agreement to integrate Kyivstar into the VimpelCom (later rebranded as VEON) ecosystem. By 2010, Kyivstar had rolled out its fiber-optic fixed-line broadband service, "Home Internet." In July 2018, on the heels of Ukraine's inaugural 1800MHz spectrum auction, Kyivstar spearheaded the launch of 4G LTE services across Kyiv, Lviv, and Odesa.

The Digital Transformation Strategy

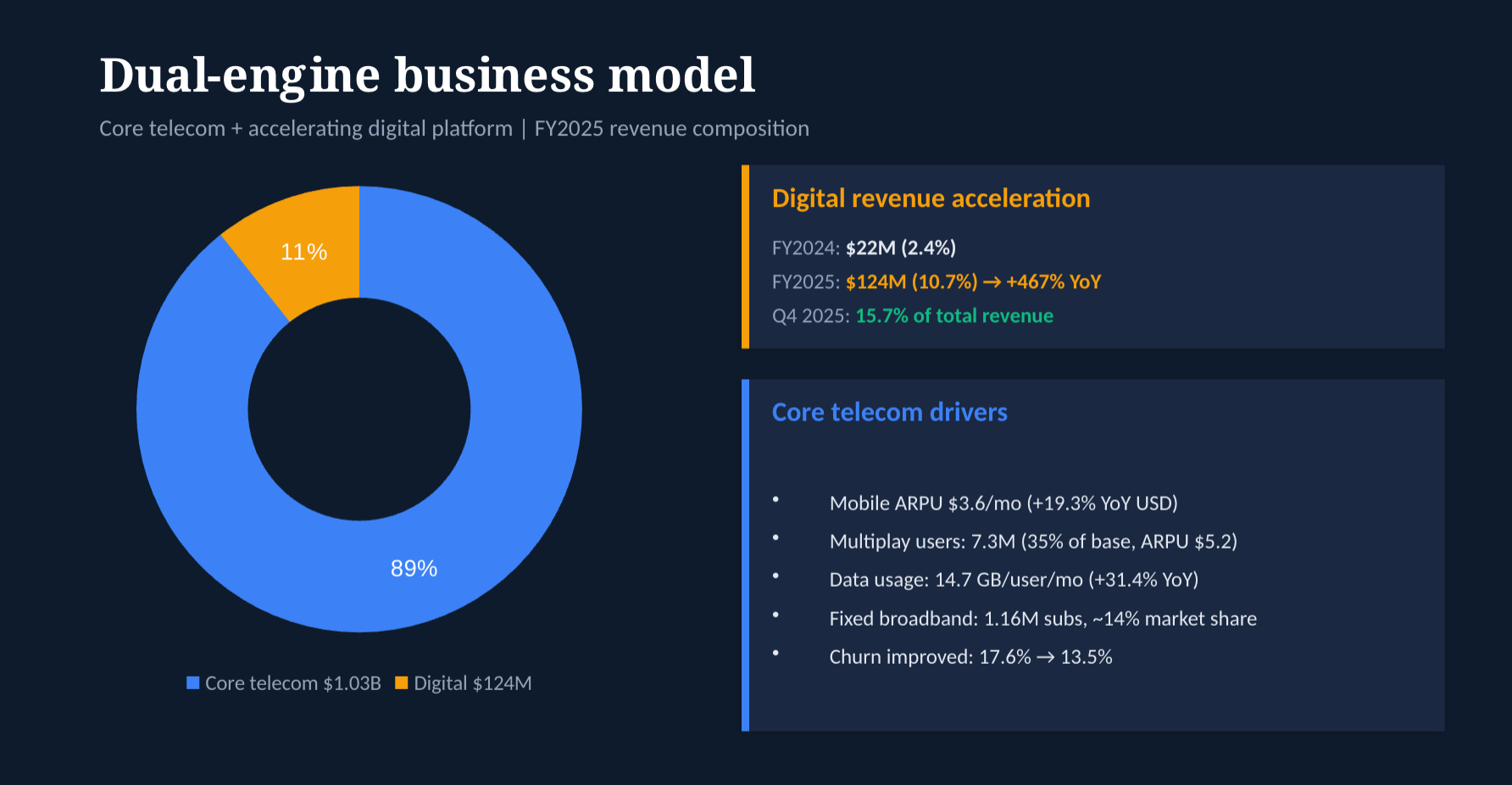

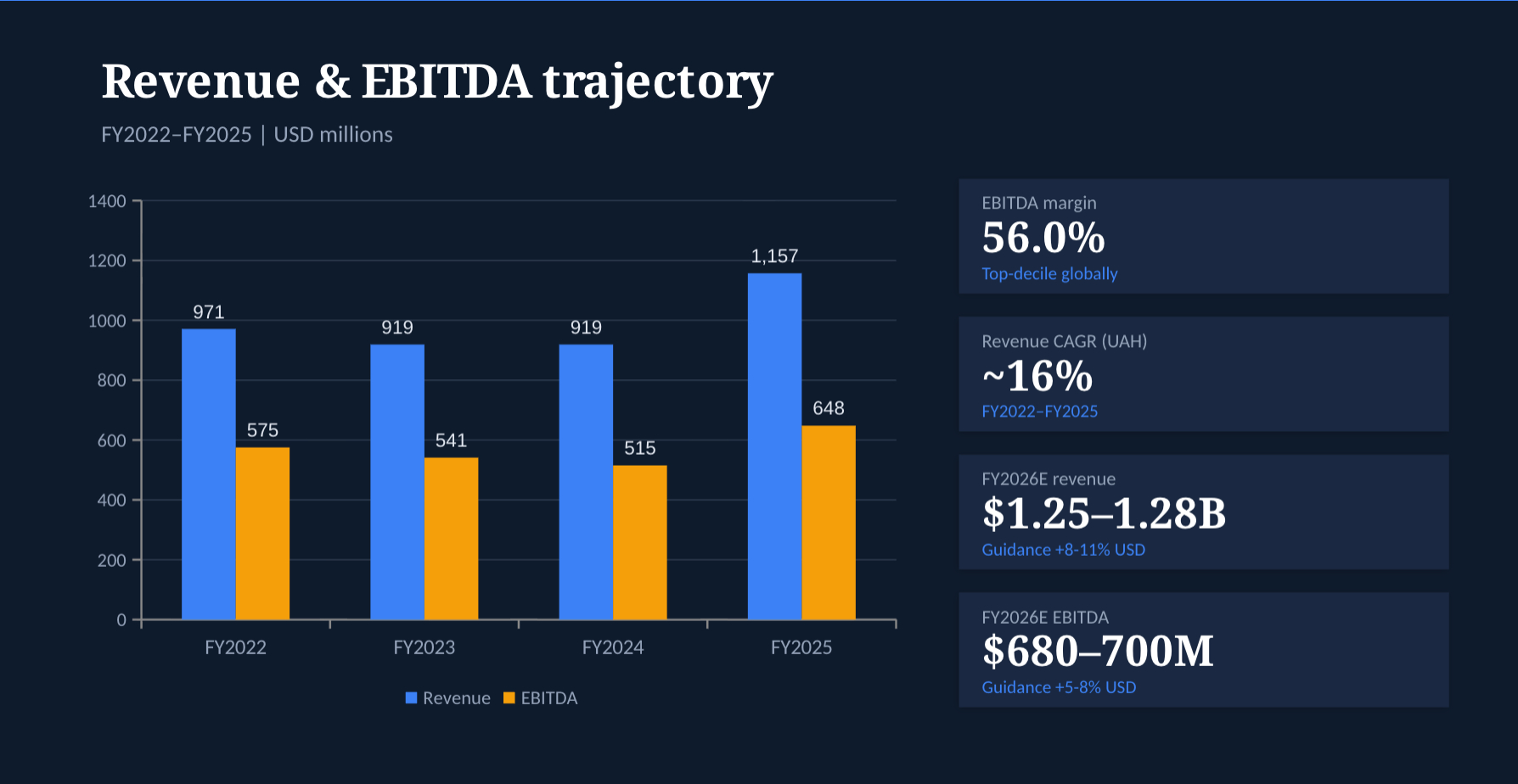

Kyivstar's business paradigm is undergoing a profound strategic metamorphosis from a traditional telecom provider to a pioneering "Digital Operator." Within the FY2025 revenue composition, the core telecom operations generated $1.033 billion (89.3%), while the digital ventures contributed $124 million (10.7%). Tellingly, by the fourth quarter of 2025, the digital revenue slice had surged to 15.7%, undeniably signaling an accelerating transformation.

Core Telecom Operations

The Multiplay strategy acts as the primary growth engine. As of Q4 2025, 7.3 million subscribers had opted for bundled services (representing 35% of active mobile users). The Average Revenue Per User (ARPU) for multiplay subscribers achieved $5.2 (UAH 220), significantly surpassing single-service users. Concurrently, mobile subscriber churn rates demonstrated dramatic improvement, descending from 17.6% (Q4 FY2024) to a healthier 13.5% in FY2025.

Mobile Connectivity

The mobile segment remains the foundational rock of revenues, injecting approximately $980 million in FY2025. By year-end 2025, Kyivstar commanded 22.4 million mobile subscribers alongside 1.16 million fixed broadband users, while its 4G base expanded to 15.4 million (reflecting a 68.7% penetration rate). Mobile ARPU illustrated formidable ascending momentum: the FY2025 annualized ARPU averaged $3.6/month (UAH 149.3), posting robust year-over-year gains of 19.3% in USD and 23.5% in UAH. By Q4 2025, ARPU peaked at $3.8/month (UAH 161.1). Key growth catalysts included disciplined pricing architectures, elevated multiplay penetration, surging data consumption (scaling to 14.7GB/user/month in Q4, a 31.4% YoY surge), and perpetually climbing 4G penetration.

Network Infrastructure Resilience

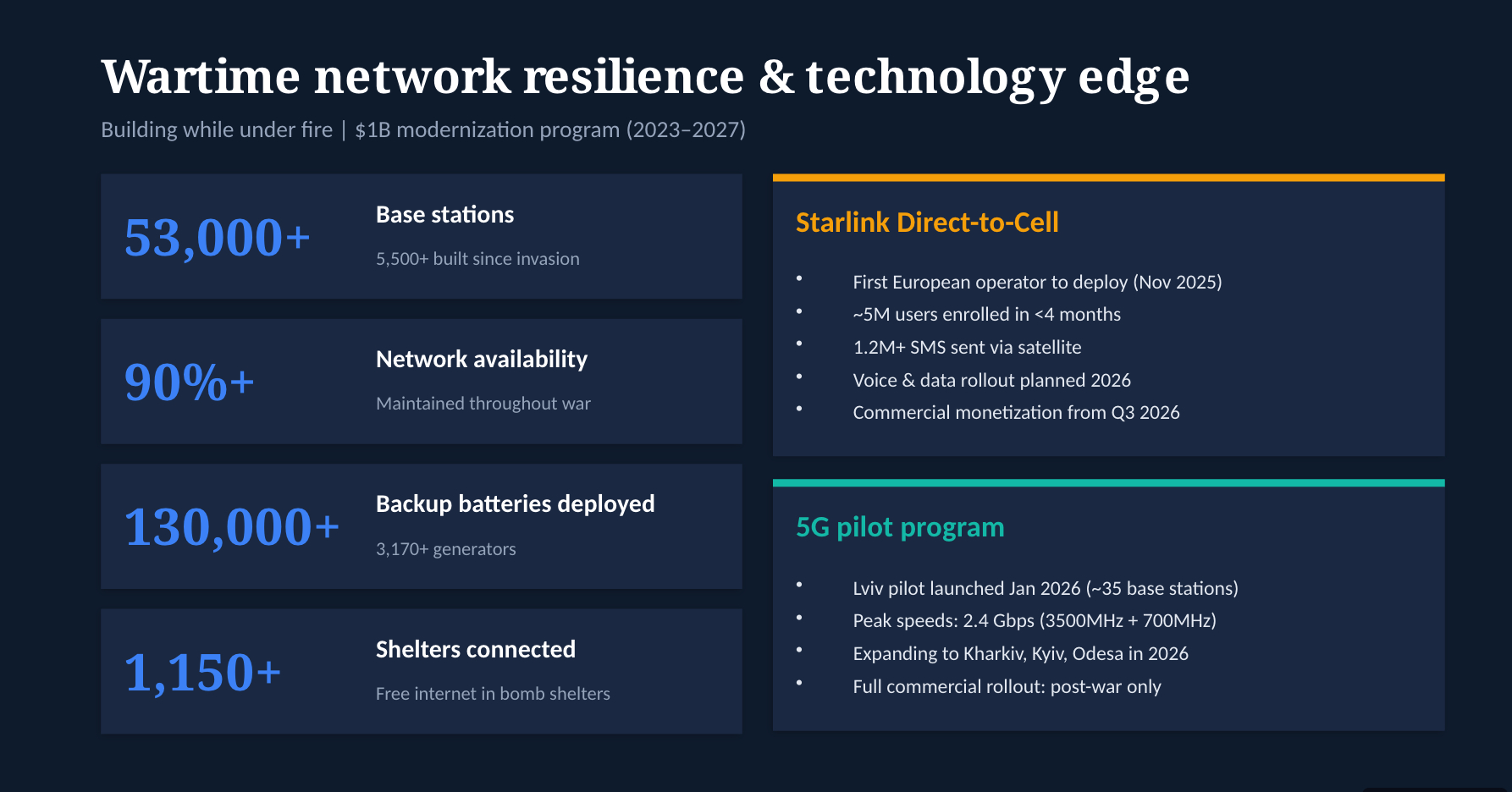

Kyivstar marshals a formidable network exceeding 53,000 base stations. Its 4G LTE canopy blankets 96% of the populace within Ukrainian government-controlled territories (targeting 98% by late 2026), enveloping all urban centers and upwards of 28,000 rural municipalities. Intriguingly, since the full-scale invasion commenced in February 2022, the corporation has constructed over 5,500 nascent base stations and upgraded 13,000+ existing sites to 4G, ironically resulting in a post-invasion 4G site count that eclipses pre-war metrics.

The network's operational resilience is staggering: average network availability has stubbornly held above 90% since the comprehensive invasion. Proactively countering Russia's systemic bombardments against energy infrastructure, Kyivstar deployed over 130,000 four-hour backup batteries alongside 3,170+ backup generators, assuring critical hubs retain a minimum of 72 hours of autonomous power. Furthermore, 1,150+ air raid shelters have been equipped with complimentary internet access. December 2025 marked another milestone with the acquisition of the SUNVIN 11 solar power facility (12.9MW)—capable of supplying roughly 4% of the corporation's annual electrical demand—representing a pivotal stride toward energy independence. This tenacious resilience garnered the prestigious "Best Mobile Innovation for Emergency/Humanitarian Situations" at the 2024 GSMA Global Mobile Awards.

In the fixed-line broadband arena, Kyivstar has propagated fiber-optic networks across 130+ metropolises. The February 2026 buyout of ISP Shtorm (adding 50,000+ users for UAH 420 million) resolutely fortified its estimated 14% leadership command over the Ukrainian fixed broadband domain.

Starlink Direct-to-Cell Integration

On November 24, 2025, Kyivstar formally introduced its Starlink Direct-to-Cell service, coronating itself as the inaugural European operator, and among the vanguard globally, to deploy this bleeding-edge technology. Harnessing SpaceX's constellation of 650+ low Earth orbit satellites, the protocol empowers conventional 4G LTE smartphones to transmit and receive SMS messages within terrestrial dead zones without necessitating bespoke hardware, seamlessly registering as the "Kyivstar-SpaceX" network.

By the Q4 2025 earnings dispatch, nearly 5 million users had engaged the service (eclipsing 20% of the mobile cohort), channeling over 1.2 million SMS messages via satellite. The maiden phase encompasses SMS capabilities (bundled gratuitously within existing tariffs), with voice and fundamental data architectures targeted for 2026 rollouts. Commercial monetization is slated to commence in Q3 2026. Amidst wartime scenarios riddled with infrastructure blackouts, this technological leap possesses profound humanitarian and commercial gravity.

The 5G Roadmap

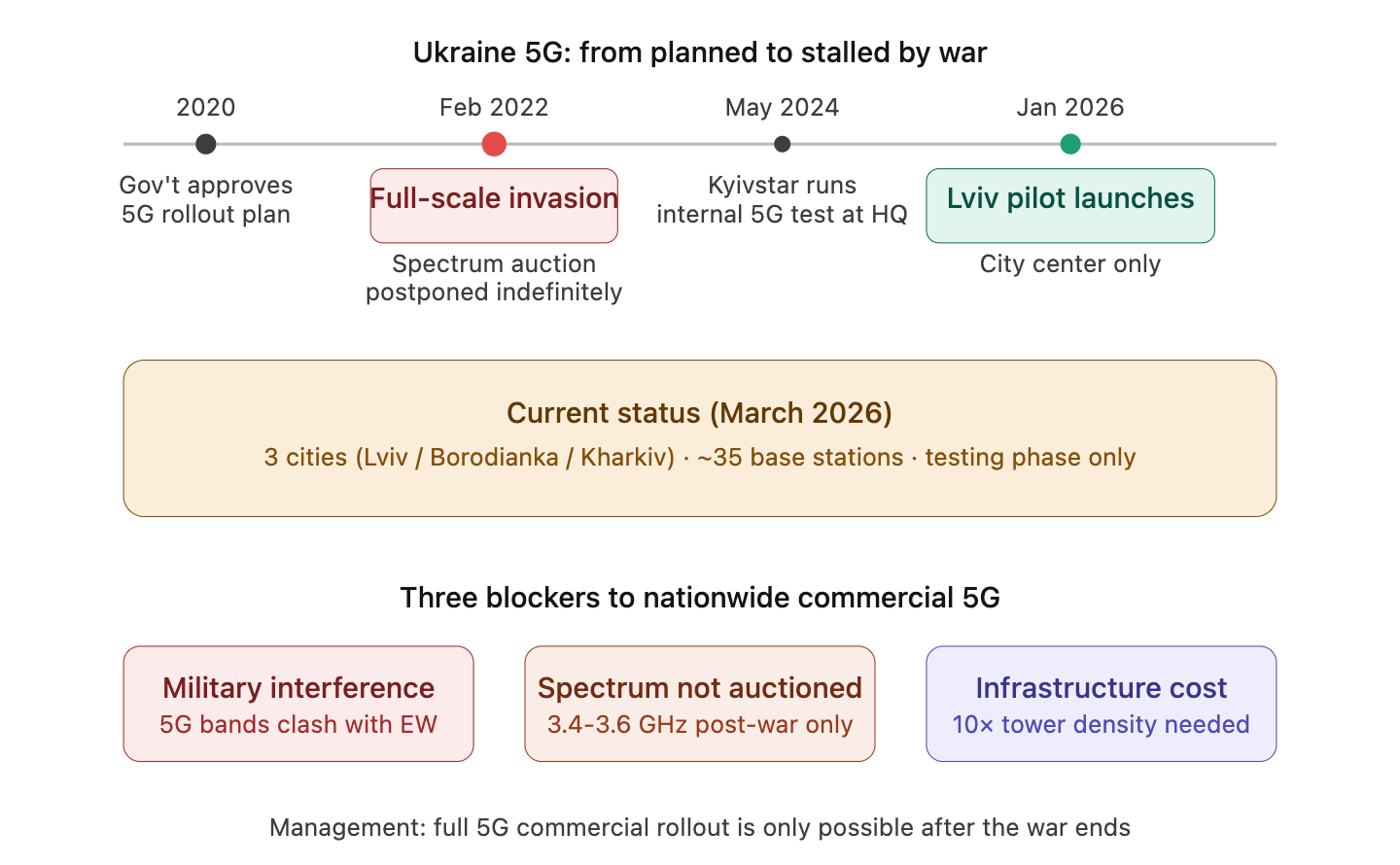

Preliminary blueprints slated a 5G spectrum auction for February 2022, yet Russia's comprehensive invasion abruptly derailed this trajectory. The indispensable 3400/3600MHz frequency bands remain monopolized by military operations, indefinitely deferring the spectrum auction until post-conflict stabilization.

On January 12, 2026, Kyivstar propelled Ukraine's maiden localized 5G pilot initiative within Lviv's historic quarter, utilizing dual 3500MHz and 700MHz bands to clock staggering peak download velocities exceeding 2.4Gbps. Expansions are earmarked for Kharkiv, Borodianka, Kyiv, and Odesa. Nonetheless, holistic commercial 5G saturation will overwhelmingly depend on post-war realities, given the suspended 3.4-3.6GHz auctions. Concurrently, Kyivstar inked a Letter of Intent with Rakuten Symphony targeting Open RAN collaborations, investigating open 5G architectures to systematically sever reliance upon Huawei/ZTE infrastructure (Chinese OEMs currently comprise roughly 60-70% of the network; complete eradication costs are projected to surpass $1 billion).

The $1 Billion Network Modernization Mandate (2023-2027) envelops infrastructure rehabilitation, energy hardening, 4G proliferation, digital ecosystem expansion, 5G groundwork, and strategic M&A. FY2025 capital expenditures registered at $351 million (consuming 30.3% of revenues), but are projected to temper toward 23-26% capital intensity ratios by FY2026, indicative of the culmination of macro-scale energy resilience outlays.

B2B Enterprise Solutions

B2B and enterprise faculties—encompassing Big Data analytics, cloud architectures (supporting 1,400+ corporate clients), cybersecurity (deploying 24/7 SOC overwatch), IoT implementations, and Microsoft Azure synergies—are aggressively pivoting toward integrated, extended 3-year recurring contract frameworks.

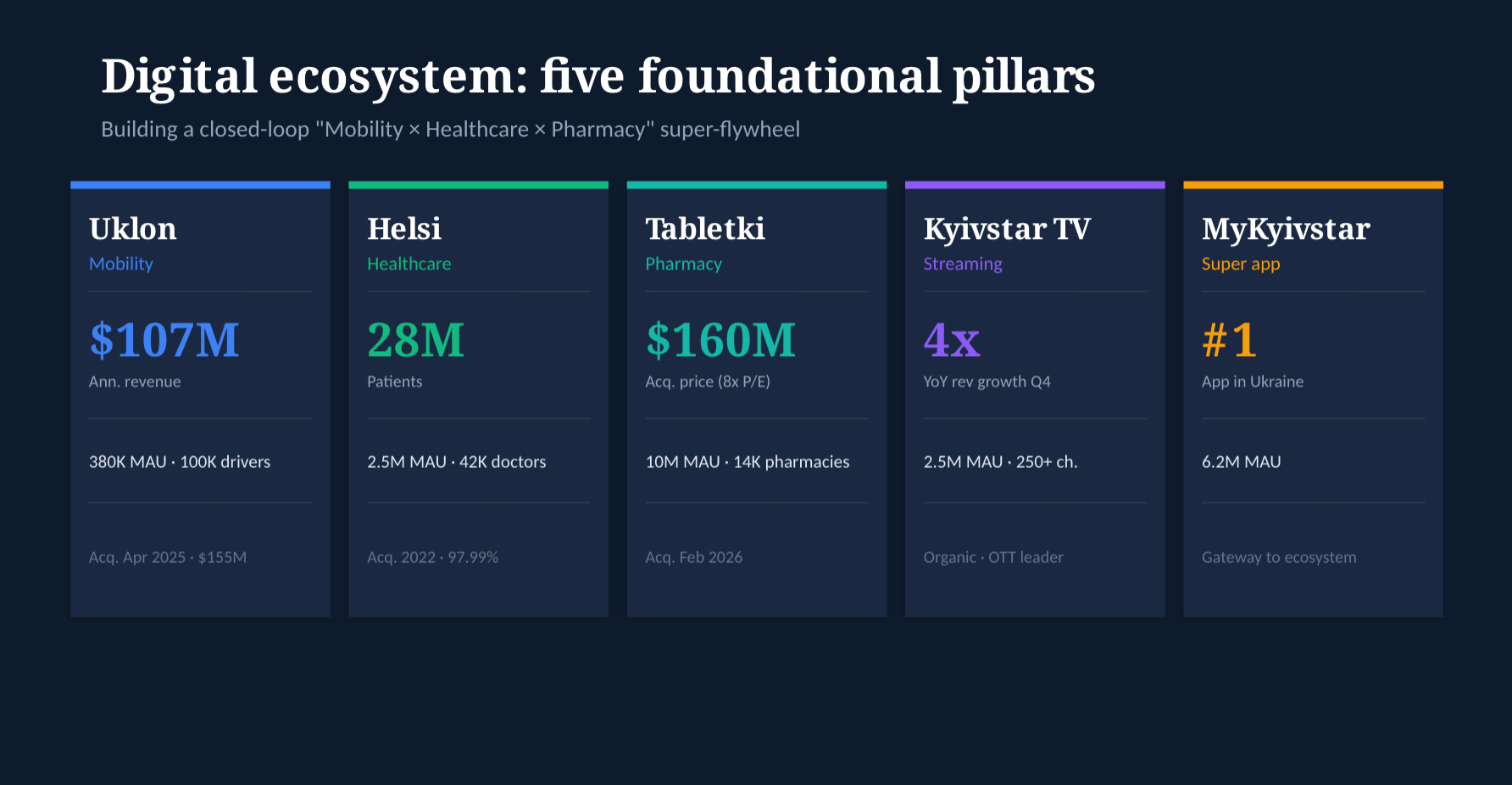

The Digital Ecosystem: Five Foundational Pillars

Legacy telecom operators perpetually confront agonizing commoditization, plateauing ARPU metrics, and excruciating CapEx burdens. Kyivstar's strategic countermeasure involves a radical architectural overhaul, crystallized by its "DO1440" (Digital Operator 1440) and "AI1440" institutional doctrines. The underlying philosophy dictates: comprising 1440 minutes daily, Kyivstar strives to engineer interaction value across every conscious minute through an impenetrable matrix of digital services, effectively transmuting low-frequency telecom billing touchpoints into hyper-frequency mobility, medical, entertainment, and financial engagements.

Digital sector revenues exploded from $22 million (2.4% share) in FY2024 to an astonishing $124 million (10.7% proportion) in FY2025, piercing 15.7% strictly within Q4 2025. Propelled by the annualized consolidation of Uklon, the integration of Tabletki.ua (consolidated Feb 2026), alongside organic surging from Kyivstar TV and Helsi, FY2026 digital revenues are forecasted to strike the $250-$300 million bracket (capturing an 18-22% share). While executive stewardship has withheld explicit terminal digital mix targets, the trajectory uncompromisingly telegraphs: "telecom + digital = platform company."

Uklon (The Mobility Nexus)

During April 2025, Kyivstar unleashed approximately $158 million to swallow a 97% controlling stake in Uklon, Ukraine's paramount ride-hailing and localized delivery titan. Consolidating Uklon acted as the supreme catalyst igniting digital gross revenue expansions. Throughout Q3 2025, Uklon executed 42.2 million passenger rides coupled with 1.2 million delivery dispatches; throughout the isolated Q4 period, Uklon furnished roughly $34 million (UAH 1.4 billion) in top-line returns alongside nearly $9 million (UAH 386 million) in EBITDA. Progressing into 2026, Uklon broadened its commercial dominion by launching "Travel"—an integrated intercity and international bus ticketing reservation matrix embedded natively within its app. Framed against wartime suspensions of commercial aviation and hyper-congested rail networks, this functionality instantly saturated a gaping void within long-haul transit markets, evolving Uklon from a singular ride-hailing app into an omnipresent mobility platform enclosing localized transit, courier dispatch (Uklon Delivery), advertising networks (Uklon Ads), and extended passenger transport. The deeper commercial genius lies in Kyivstar exploiting its 22.4 million captive telecom user base to aggressively funnel volume into Uklon operating atop phenomenally reduced Customer Acquisition Costs (CAC), cementing brilliant cross-monetization.

Helsi (Digital Healthcare) & Tabletki.ua (Digital Pharmacy)

Healthcare architectures constitute an equally vital artery coursing through the DO1440 agenda. Kyivstar optimally positioned itself early by seizing control (97.99%) of Helsi, Ukraine's preeminent digital healthcare SaaS apparatus, backward in 2022. Exiting 2025, Helsi commanded 2.5 million Monthly Active Users (MAUs), with premium subscription tiers witnessing an astronomical 283% YoY explosion scaling toward 57,000 paid users, dragging fourth-quarter revenues upward 65.7% touching $2.3 million.

To resolutely seal the commercial loop encapsulating healthcare ecosystems, Kyivstar publicized its February 2026 all-cash acquisition (valued at $160 million) encompassing 100% equity within Tabletki.ua, Ukraine's absolute leading pharmaceutical e-commerce and algorithmic price-comparison juggernaut. Interlocking a staggering 14,000+ national pharmacies, Tabletki.ua routinely processed roughly 14 million digital reservations each month throughout 2025, parlaying its trailing twelve-month (LTM) Gross Merchandise Volume (GMV) to a towering $1.19 billion, unlocking $24 million generating EBITDA alongside $20 million traversing net profitability. This transaction valuation screams profound attractiveness (modeling approximately an 8.0x P/E multiplier). Architecturally, President Oleksandr Komarov outlines a flawlessly frictionless user journey: utilizing Helsi applications, patients execute virtual consultations culminating in physician-dispatched electronic prescriptions, whereby operating systems intrinsically catapult patients directly into Tabletki.ua empowering universal price-comparison and pharmaceutical reservation, concluding seamlessly with Uklon Delivery couriers physically dispatching medications straight to residential thresholds. Upon achieving ubiquitous synchronization, this "Medical + Pharmacy + Delivery" super-flywheel will architect moats profoundly impenetrable against standalone internet counterparts.

Kyivstar TV (Streaming Media)

Commanding Ukraine's paramount OTT streaming dominion, supplying 250+ broadcasting channels alongside VOD libraries. Capturing 2.5 million MAUs, Q4 2025 revenues exploded toward UAH 351 million (printing a massive 4x YoY expansion), notably transitioning away from rudimentary revenue-sharing constructs toward platform leasing paradigms, whilst aggressively escalating concentrated capital deployments funding proprietary Ukrainian-language original productions.

MyKyivstar Super App Ecosystem

Acting as the definitive gateway dictating account oversight, service clustering, and overarching digital ecosystem penetrations, cultivating 6.2 million MAUs, unequivocally reigning as the single most voluminous platform within the portfolio.

M&A Pipeline Trajectory

Completed and active acquisitions encompass: Helsi (2022), Uklon (April 2025, $155M), SUNVIN 11 Solar (Dec 2025, $8.2M), Tabletki.ua (Feb 2026, $160M), and Shtorm ISP (Feb 2026, UAH 420M). Executive stewardship overtly communicates intentions to continuously deploy its approximated $400M in trapped localized liquidity financing strategic takeovers, honing targeting parameters precisely upon digital fintech/insurtech verticals juxtaposed alongside regional ISP consolidations.

Financial Health Check

Accelerating Performance Guidance

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue (USD) | $971M | $919M | $919M | $1.157B |

| YoY Revenue Growth (USD) | — | -5.4% | 0.0% | +25.9% |

| YoY Revenue Growth (UAH) | — | +8.0% | +10.3% | +30.3% |

| EBITDA (USD) | $575M | $541M | $515M | $648M |

| EBITDA Margin | 59.2% | 58.9% | 56.0% | 56.0% |

| Adjusted Net Income | — | — | $283M | $286M |

| Adjusted EPS | — | — | $1.37 | $1.32 |

FX Volatility persistently corrodes USD-denominated reporting thresholds. FY2023-2024 USD revenue stagnancy predominantly mirrored the Hryvnia's structural depreciation (UAH/USD softening from 32.34 toward 40.16), however, underlying localized currency revenues tenaciously maintained 8-10% bedrock growth rates. FY2025 unleashed violent upside breakouts propelled uniformly stemming from Uklon consolidations, formidable ARPU escalations, and digital explosions.

Quarterly momentum telegraphs unambiguous accelerations: Q1 $255M → Q2 $284M → Q3 $297M → Q4 $321M (+28.4% YoY), driving digital revenue concentrations soaring outward from sub-5% Q1 metrics breaching 15.7% throughout Q4 run-rates.

Fortress Balance Sheet

Crossing December 31, 2025, the corporation gripped cash and cash equivalents totaling $455 million, rendering a net cash stronghold equating $352 million subsequent to lease liability deductions. The debt architecture remains profoundly conservative: combined bond and loan principal obligations register a minuscule $104 million (overwhelmingly parent-company VEON intra-loans), framing external leverage as "functionally immaterial." Lingering $374 million lease liabilities principally reflect IFRS 16 recognition mandates stemming from legacy telecom tower divestitures channeling Ukrainian Tower Company (UTC). Gross equity commands $1.299 billion, establishing an exceptionally low 0.63 debt-to-equity ratio.

The overriding constraint underscores: Capital liquidity remains fundamentally trapped domestically. National Bank of Ukraine (NBU) wartime capital control protocols strictly embargo foreign enterprises from upstreaming profit distributions or forex repatriations supporting offshore parent entities. The nominal exemption established during May 2024 (yielding a paltry €1 million per entity monthly) falls drastically short regarding engineering meaningful capital extractions.

Robust Cash Generation

FY2025 operating cash flows eclipsed $558 million (+29.8% YoY), dropping potent Free Cash Flow to Equity (subsequent to lease and license extractions) touching $194 million. Total $351 million capital expenditures allocated $247 million traversing PP&E alongside $86 million regarding intangible assets. Additionally, FY2025 unleashed $157 million targeting direct M&A (dominantly Uklon).

The Valuation Divergence

| Valuation Metric | KYIV | Emerging Market Telecom Peers Mean | Discount Magnitude |

|---|---|---|---|

| Forward EV/EBITDA | ~4.7x | ~5.5-6.5x | 25-40% |

| Forward P/E | ~7.2x | ~10-12x | 35-40% |

| EV/Revenue | ~2.1x | ~2.5-3.0x | ~20-30% |

| P/FCF | ~5-7x | ~8-12x | ~35-45% |

| PEG Ratio | ~0.9x | — | Under 1.0x |

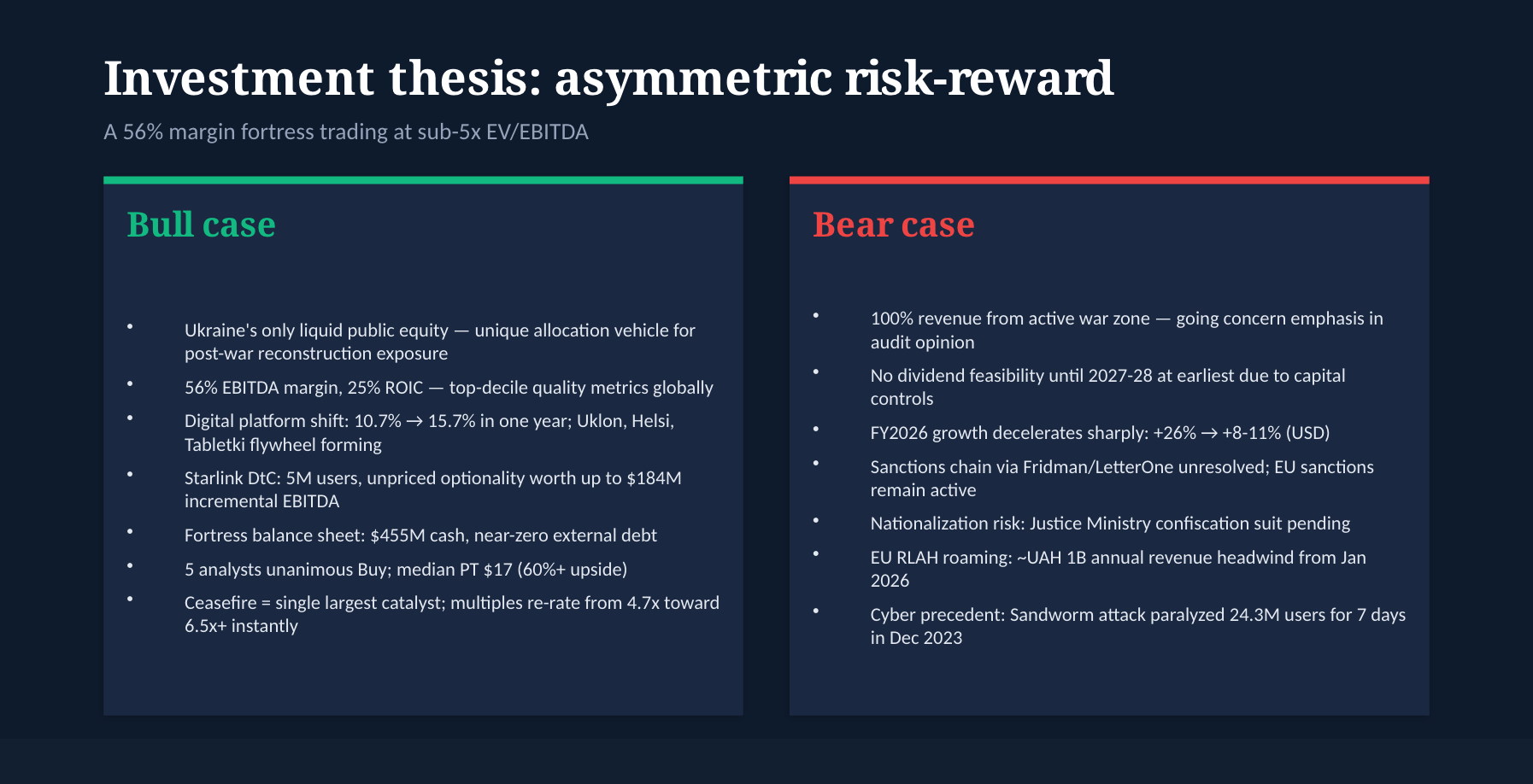

Commanding a 56% EBITDA margin, the entity sits comfortably atop global telecom hierarchy tierings (measured against emerging peer baselines hugging roughly 35-45%), validating profound Ukrainian market pricing leverage combined alongside ruthless operational efficiencies. Unearthing stellar 25.2% ROIC metrics substantiates sublime capital allocation competency.

The Trifold Risk Depressing Valuation

Conflict/Geopolitical Hazards dictate overwhelmingly as the supreme primary existential threat. Capturing absolutely 100% of top-line revenues internally from Ukraine natively exposes the enterprise violently toward TAM contractions fueled by 6 million+ expatriated refugee out-migrations. Systematized Russian bombardments obliterating underlying power grids trigger persistent blackout parameters, ostensibly countered nonetheless by Kyivstar injecting UAH 1.4B+ architecting localized backup power grids. Crucially, external audit mechanisms definitively inscribed an emphasis of matter paragraph highlighting profound material uncertainty surrounding going concern classifications, unambiguously articulating "severe unrest stemming from relentless Russian military hostility might cast pronounced doubt combating the entity’s continuous operational viability."

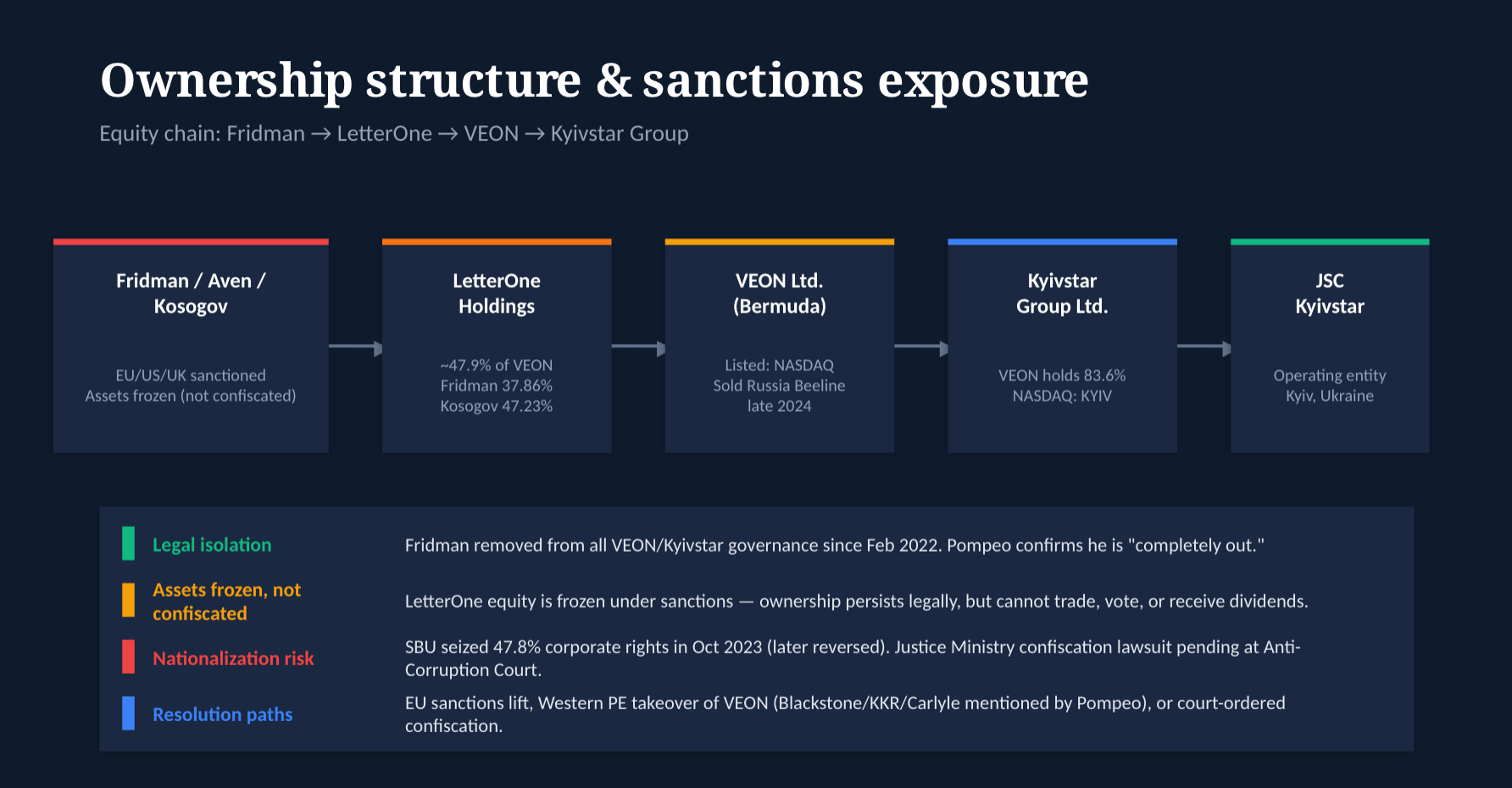

Sanctions Contagion proliferates ominously throughout the overarching VEON → LetterOne → Fridman equity cascading chain. Mikhail Fridman alongside Petr Aven incurred sweeping EU/US/UK embargos dating February 28, 2022, while Fridman commands approximately 37.86% holdings spanning LetterOne, which correspondingly secures about 45.46% of VEON. VEON vehemently argues sanctioned personnel exercise "absolute zero capacity" dictating operational commands, emphasizing Fridman abdicated VEON board standings entirely. VEON successfully jettisoned its Russian Beeline assets rounding late 2024, significantly attenuating sanctions exposure.

Nationalization Peril maintains chilling authenticity. Tracking October 2023, the Security Service of Ukraine (SBU) controversially sequestered 47.8% of Kyivstar's corporate rights (mirroring corresponding LetterOne VEON holdings), although Kyiv courts subsequently rescinded said seizure by November 2024. Nevertheless, Justice Ministry officials have formally petitioned High Anti-Corruption Courts demanding comprehensive confiscation relating Fridman-associated property, highlighting broad statutory combat-powers available authorizing wartime governments overtaking strategic equity. Traversing theoretical legal governance channels, Fridman cohorts encounter complete insulation; conversely, bridging economic equity realism, they invariably persist representing dominant indirect beneficiaries despite encountering freeze parameters. Such deeply structural opacity intrinsically underpins capital markets applying brutal "sanctions discounts." Ascendant critical pivot variables traverse precisely whether Ukrainian courts ultimately authorize total confiscation, whether EU bodies repeal Fridman's embargo status, or whether tier-one Western PE institutions (explicitly citing Pompeo mentioning Blackstone, KKR, or Carlyle frameworks) enact amicable VEON takeovers completely amputating historical Russian capital tethers.

Cyber-Warfare Intrusion commands horrifying precedents. Marking December 12, 2023, the heralded Russian GRU subordinate element Sandworm (Unit 74455) unleashed "arguably among the most catastrophic cyber-strikes historically targeting civilian communications infrastructure" directly assaulting Kyivstar, piercing fundamental perimeter defenses exploiting hijacked employee credentials secured initially tracing back to May 2023, achieving absolute administrative oversight ultimately obliterating thousands of core processing virtualization instances alongside terrestrial PCs. Severe ramifications disrupted 24.3 million mobile alongside 1.1 million broadband consumers, enforcing absolute service blackouts spanning approximately seven trailing days, rendering regional Kyiv and Sumy emergency air raid alerting architecture temporarily defunct. Restoration mandates commanded intensive Ericsson and Microsoft support synergies, paring finalized structural financial damages toward refined ~$24 million assessments (initially speculated challenging $100M).

Analysts universally establishing coverage flanking KYIV endorse Buy matrices, culminating converging median target valuations circling $17:

- Oppenheimer (Tim Horan): Outperform, Target $20.00

- Northland Securities (Tim Savageaux): Outperform, Target $19.00 (Upgraded February 2026)

- Cantor Fitzgerald: Overweight, Target $17.00

- New Street Research (Chris Hoare): Buy, Target $16.00

- Redburn Atlantic (Stephen Malcolm): Buy, Target $15.30

Fundamental bullish tenets advocate: Absolute dictatorial Ukrainian market hierarchy positioning, top-decile EBITDA margin structures, hyper-growth trajectory digital platform elements, decisive Starlink vanguard positioning, an impenetrable fortress-grade balance sheet, immensely depressed valuation multiples (PEG < 1), coupled alongside theoretical peace-catalysts theoretically unlocking 40%+ pricing discrepancy corrections. Conversely, cardinal bearish underpinnings emphasize: Singularly concentrated 100% active theater-of-war exposure profiles, fundamentally non-existent dividend probabilities, going-concern operational fragility, terminal-tail sanctions/nationalization catastrophe risk, juxtaposed alongside tempered 2026 top-line velocity regressions (compressing from 26% toward 8-11% trajectories).

The Quintessential High-Risk / High-Reward Investment Profile

Kyivstar Group engineers a fascinatingly anomalous investment hypothesis—a commanding top-tier telecom operator generating staggering 56% EBITDA margins alongside 25% ROIC constructs, incubating an explosively expanding digital ecosystem while pioneering globally exclusive Starlink direct-to-cell integrations, trading paradoxically sub-5x forward EV/EBITDA multiples entirely attributable to overarching conflict dynamics. The profound operational resilience exhibited navigating extreme terminal hostilities (Sustaining 90%+ network availability baselines, instantiating 5,500+ novel towers, equipping 1,150+ subterranean bunkers, bounding back recovering core functionalities within 72 hours traversing humanity's premier telecommunications cyber-attack) intrinsically establishes breathtaking intangible asset valuation accompanied simultaneously by absolute managerial crisis-competency vindication.

Ukrainian asset scarcity bestows unreplicable allocation utility flanking KYIV. Acting uniformly as U.S. capital markets' solitary and pioneering pure-play Ukrainian listed instrument, Kyivstar outfits global allocators unprecedented explicit, highly liquid equity conduits directly engaging Ukrainian macroeconomic trajectories—an ascending frontier market spanning 37 million populace commanding roughly $180 billion underlying GDP, progressively accelerating alongside EU integration roadmaps. Entrenched within Ukraine's ICT sector, Kyivstar commands supreme maximum taxpayer categorization alongside largest foreign capital enterprise distinctions, consequentially decorated serially by Forbes Ukraine affirming "Paramount International Ukrainian Investor" status. This supreme pinnacle ensures definitively that regardless of subsequent post-war structural reconstruction capital deluge pathways flooding Ukrainian economies, Kyivstar systematically captures position as an undisputed direct paramount beneficiary.

The defensive moat registers phenomenally deep, progressively fortifying amidst enduring conflict. Hoarding comprehensive 48% mobile market penetration, amassing 202MHz spectrum allocations (supplanting nearest combatants beyond 30%+ margins), blanketing comprehensive topological footprints bridging 28,000+ communities, while guaranteeing commanding $1 billion investment agendas bridging 2023-2027 timelines constructs virtually impenetrable competitive entry blockades. Crucially paramount however, sustaining three agonizing years of unrelenting capital commitments—exactly precisely when contemporaries executed full-scale retreats or adopted paralyzed spectating postures—endowed Kyivstar possessing monumental unquantifiable yet supremely priceless "wartime dividends" measuring brand fanaticism, sovereign government alignment alongside immense societal credibility. Seating former U.S. Secretary of State Michael Pompeo upon sovereign corporate boards unequivocally constitutes an unmistakable endorsement signifying immense aggregate strategic gravitas.

Digital transmutation rigorously evolves traversing conceptual visions toward absolute concrete actualization. Securing formidable 10.7% annualized digital revenue compositions (touching 15.7% strictly traversing Q4 intervals), compiling 15 million active monthly digital participants (surging +41.6% YoY), actively architecting impregnable Uklon+Helsi+Tabletki.ua "Locomotion × Biomedical × Pharmacology" closed-loop ecosystems fundamentally guarantees Kyivstar transcends simplistic traditional telco categorizations. FY2025 digital top-lines detonated 467% YoY striking $124M; Uklon annualized run-rates decisively breached $100M benchmarks retaining 34% EBITDA conversion; Tabletki.ua integration at $160M (merely 8x P/E) guarantees instantaneous accretive yield enhancement. Should disparate capital markets algorithmically partition encompassing digital platform conglomerates isolating 7-10x EV/EBITDA independent valuations, this exact fragment theoretically commands $500-$900 million standalone—functionally accounting reaching approximately twenty-five toward thirty-three percent covering overarching combined corporate capitalization multiples. Ultimate executive ambitions projecting conversion bridging 6.2 million legacy MyKyivstar MAUs integrating cross-vertical consumer metrics vividly telegraph evolutionary leaps departing from simplistic "connectivity providers" hurdling comprehensively becoming definitive "daily life platforms."

Starlink Space-to-Cell Integration engineers profound unpriced optionality vectors. Anchoring global commercial pioneering deploying SpaceX Starlink Direct-to-Cell architecture, Kyivstar forcefully captured five million participating consumers clocking less than four operational months, systematically verifying explosive latent market appetites demanding definitive "satellite coverage eliminating hardware retrofit prerequisites." With sequential commercial monetization launch targeting Q3 2026 overlapping cascading deployment phasing incorporating voice and light data capacity modules. Aggressive optimistic financial modeling posits Starlink yielding monumental $368 million top-line incremental augmentation compounding $184 million incremental EBITDA expansion—roughly corresponding adding phenomenal 28% supplementary lift atop prevailing baseline EBITDA profiles, rendering profound paradox considering marketplace algorithms essentially attribute absolute zero correlative premium valuation.

Nevertheless, all exuberant prognostications remain fundamentally tethered contingent upon conflict trajectories achieving stabilization or definitive termination. Navigating underlying audit dimensions, simple regulatory 20-F documentation filings intersecting March 2026 instantaneously sparked violent 7.2% equity routs exactly upon submission dating. Overt nationalization perils harbor deeply ingrained authentic operational precedence: SBU mechanics forcefully impounded 47.8% corporate structural rights circling 2023, while subsequent judicial annulments achieved partial deterrence, Ministry of Justice institutional asset confiscation proceedings actively populate Anti-Corruption Court dockets. The sweeping VEON → LetterOne → Fridman sanctions continuum maintains operational compartmentalization insulating management channels further reinforced following Russian Beeline divestitures, yet sweeping EU sweeping embargos currently retain pervasive validity. Entrenched Ukrainian wartime capital control parameters effectively immobilize $455 million onshore localized liquidity rendering baseline dividend policies structurally unfeasible stretching forecasting horizons spanning trailing 2027-2028 boundaries minimum. Finally, FY2026 overarching forward guidance telegraphs significant velocity decompression traversing downward from aggressive 26% baselines contracting returning toward 8-11% USD trajectories, compounded by descending EU roaming legislative implementations engineering estimated UAH 1 billion underlying revenue headwinds, constantly perpetually battling depreciating localized Hryvnia foreign exchange differentials incessantly eroding fundamental dollarized reporting frameworks. These dynamics represent unyielding immutable structural constraints fundamentally transcending simplistic "transitory market mispricing" theorems.

DE-SPAC Analytics Deep-Dive

Architectural Trajectory Timelines

| Categorization Dates | Sequential Event Horizons |

|---|---|

| January 13, 2025 | Distinctive Letter of Intent (LOI) ratification spanning VEON alongside Cohen Circle frameworks |

| March 7, 2025 | Foundational Kyivstar Group Ltd. (PubCo) structural integration executed within Bermuda domains |

| March 13, 2025 | Varna Merger Sub Corp. subsidiary architecture formalized crossing Cayman Island jurisdictions |

| March 18, 2025 | Definitive binding Business Combination Agreement (BCA) signatures executing public transaction reveals |

| June 5, 2025 | Kyivstar Group publishes foundational overarching F-4 Registration Statement traversing SEC pipelines |

| June 24, 2025 | Initial BCA revision implementation (Authorizing foundational share re-allocations bridging Sellers and Sponsors) |

| July 10, 2025 | Secondary BCA amendment implementation; formalizing overarching NRA architectures (accounting roughly $52.3M) |

| July 21, 2025 | Concluding Shareholder Assembly Record Dates |

| August 12, 2025 | Special Shareholder Assemblies concretely voting confirming underlying transaction ratification |

| August 14, 2025 | Concluding Business Combination settlement mechanics finalized |

| August 15, 2025 | Primary KYIV alongside derivative KYIVW ticker initiation commencing NASDAQ marketplace integration |

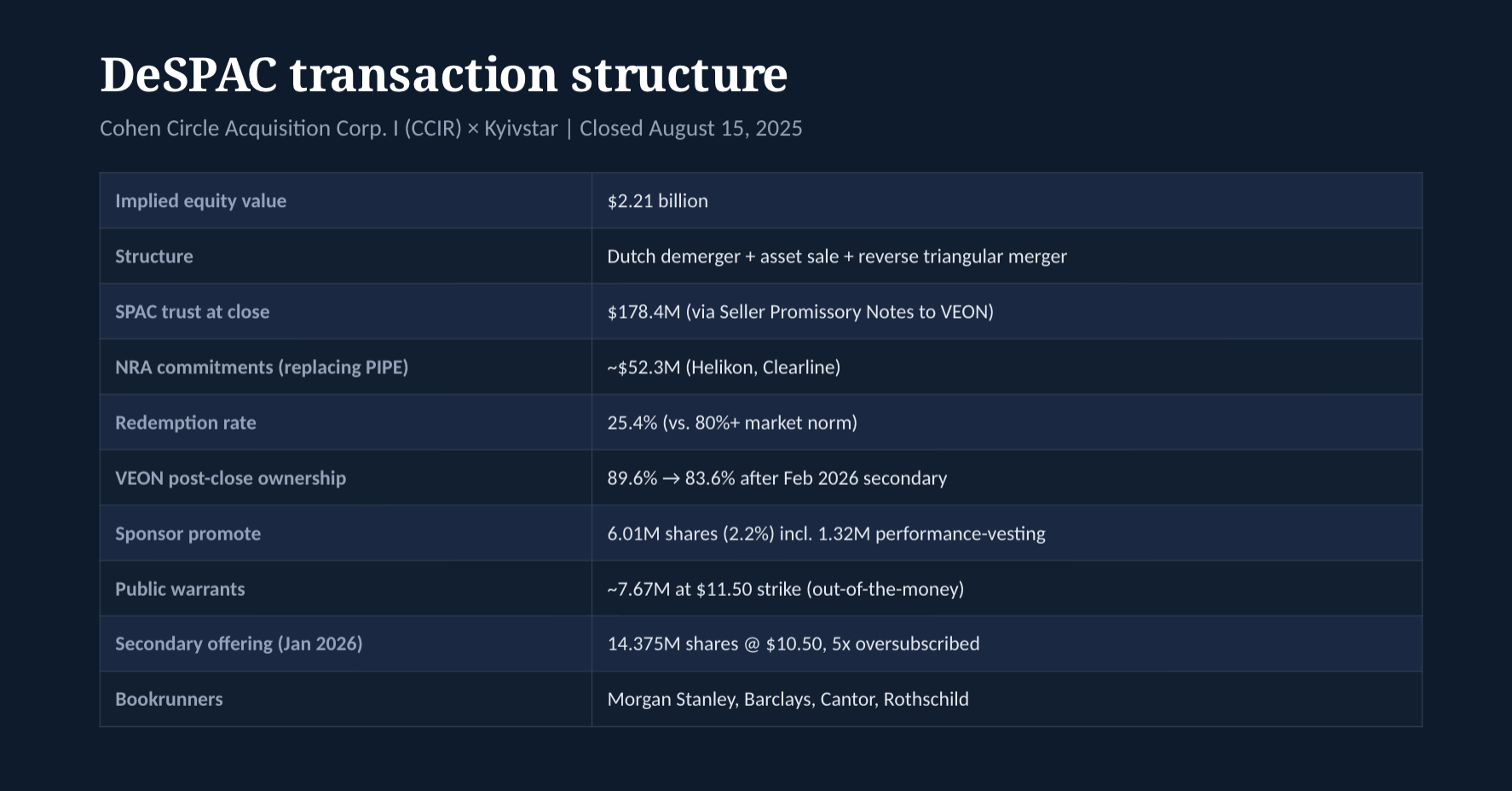

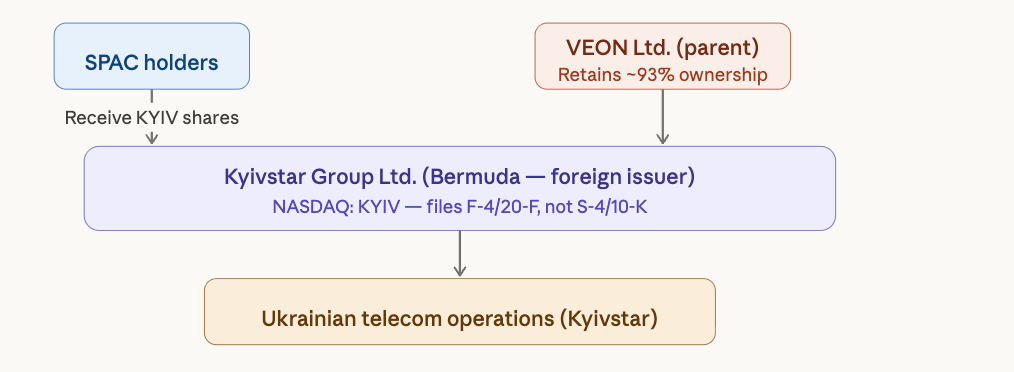

Structural Transaction Architecture

The overarching corporate infrastructure implements definitive Bermuda Holding Company frameworks (Incorporation finalized March 2025 spanning Bermuda), operating primary executive functionality installations housed occupying Dubai International Financial Centre (DIFC) quadrants, retaining original overarching operational headquarters stationed precisely atop 53 Degtyarivska Street, Kyiv.

Fundamental transaction structures intersected intertwining five principal constituent participants: Kyivstar Group Ltd. (PubCo, Bermuda), Cohen Circle Acquisition Corp. I (SPAC, Cayman entities), VEON Amsterdam B.V. (Divesting Seller), VEON Holdings B.V. (Kyivstar Parent architectures), cascading toward Varna Merger Sub Corp. (PubCo affiliated subordinate merger elements).

Preliminary Pre-Closing Architectural Reorganization: VEON instituted initial Dutch-jurisdiction statutory demerger (spin-off) mechanisms traversing VEON Holdings B.V. infrastructure, strictly mandating resultant spin-off entities encapsulate exclusively JSC Kyivstar traversing accompanying subordinate subsidiaries retaining exclusive linked asset-liability architectures. Collateral extraneous core operating VEON subsidiaries underwent relocation pivoting targeting extraneous decoupled formations. Spin-off procedures attained finalizing administrative recognition spanning Dutch Chamber of Commerce tribunals reaching January 2025.

Phase One — Foundational Asset Divestiture: VEON Amsterdam B.V. completely liquidated holistic fully diluted issued equity holdings commanding VEON Holdings B.V. directly bridging PubCo acquirers, demanding precise compensation architectures measuring 206,942,440 freshly minted PubCo Ordinary Shares complimented incorporating overriding $178.4 million Seller Promissory Loan Notes. Applicable mathematically formulated Seller equity calculation baselines: [(Settlement Equity Valuation Baseline - Assigned Seller Loan Principle) ÷ $10.35] - 303,098.

Phase Two — Inverted Triangular Merger Mechanics: Varna Merger Sub Corp. structurally collapsed amalgamating directly entering Cohen Circle entities (Establishing reverse triangular merger execution), defining Cohen Circle holding surviving continuous operational status becoming exclusive fully owned PubCo subsidiary branches. Entire comprehensive CCIR Class A combined Class B ordinary share composites triggered automated conversion cascades transitioning assuming PubCo Ordinary Share profiles, systematically minting combined 23,163,338 equity units; simultaneously all encompassing 7,666,638 overarching public warrant instruments executed 1:1 proportional conversion algorithms assuming distinctive Kyivstar Group Warrant designations.

| Shareholder Constituent Taxonomy | Equity Volume Assessed | Proportional Density |

|---|---|---|

| VEON Amsterdam B.V. (Originating Seller) | 206,942,440 | 89.6% |

| Legacy Originating CCIR Shareholders (Aggregating Class A+B) | 23,163,338 | 10.0% |

| Compensatory Allocated NRA Reward Shares | 757,745 | 0.3% |

| Absolute Summation PubCo Ordinary Shares | 230,863,523 | 100% |

| Circulating Active Outstanding Warrants | 7,666,638 | — |

Originating Founder Equity: Sponsoring entities (Cohen Circle Sponsor I, LLC alongside Cohen Circle Advisors I, LLC) historically procured 7,905,000 Class B Ordinary Shares generating nominal aggregate $25,000 consideration expenditures (equating roughly $0.003 dimensional unit pricing), configuring standard historical baseline SPAC promote architectures.

Sponsor Equity Extinguishment Mechanics: Executing in accordance traversing updated Sponsor Agreements codified July 10, 2025, Sponsors structurally capitulated voluntarily extinguishing forfeiting 2,609,647 Class B Ordinary Shares encompassing comprehensive 238,333 Private Warrant Instruments. Concluding settlement architectures left Sponsors retaining aggregate 6,010,353 standing PubCo Ordinary Shares (Integrating 5,295,353 shares cascading via transitioning remaining Class B allocations bundled identically accompanying 715,000 shares descending originating navigating Class A instruments packaged internally spanning Private Units), comprising roughly generalized 2.2% overall aggregate capitalization parameters (strictly excluding designated Vesting Securities). This radically compressed promote profile aggressively reflects prevailing normative institutional behavior governing intensive modern DeSPAC renegotiation environments.

Performance Hurdle Contingent Vehicles (Vesting Securities): Specific 1,323,838 share tranches received explicit "Vesting Security" classification designations, demanding precise hurdle satisfactions: (i) Tier One threshold implementations requiring achievement bounding two trailing sequential years post-consummation; (ii) Tier Two targets requiring overarching execution encapsulated within trailing five year bounds post-closing. Unfulfilled metrics trigger absolute systematic Vesting Security forfeiture termination.

Comprehensive Lock-Up Covenants: Originating Sponsor components holding 3,971,515 shares (Strictly exempting distinct Vesting configurations) remain shackled traversing rigorous transfer limitation strictures, enduring continuously spanning the earliest converging date encapsulating: (i) General 180 days trailing post-consummation; (ii) Spot pricing PubCo metrics striking equaling advancing traversing $13.50 limits spanning consecutive twenty trading intervals encapsulating comprehensive baseline thirty-interval bands; (iii) Or definitive pre-liquidation culmination triggers. Notably staggering, absolute 95% categorical VEON legacy seller shares suffer identically parallel identical encompassing lock-up restriction confinement.

Warrant Architectural Constructs: Singular originating IPO Unit assemblages fused singular Class A shares seamlessly integrating one-third proportion redeemable fractional warrants, compounding generating aggregate approx. 7,666,667 circulating public warrant instruments demanding explicit $11.50 per share execution strikeprices. Private Placement Warrants (registering 238,333 unit volume) experienced absolute total zero-consideration annihilation concurrently upon executed settlement closing. Notably crossing finishing parameters respective circulating warrants remained firmly suspended functioning fundamentally maintaining rigid out-of-the-money status classifications (Contrasted explicitly juxtaposed crossing baseline $10.35 foundational reference benchmarks).

Transactional Blueprint Highlights

Unprecedented NRA Mechanics Superseding Conventional PIPEs

This extraordinary transaction operated entirely omitting fundamental legacy traditional PIPE placement architectural dependencies. Alternatively replacing legacy methodologies, architects favored incorporating Non-Redemption Agreements (NRAs)—Establishing decisively dominant instrumental mechanisms commanding recent prevailing modern DeSPAC ecosystem deployments. Overarching NRA methodologies attained public broadcasting synchronized aligned matching overlapping Second BCA Amendments navigating July 10, 2025.

Foundational NRA Structural Mechanics: Validated qualified institutional contingents affirmatively committed extending guarantees (i) exercising explicit supportive affirmative proxy votes utilizing corresponding retained CCIR Class A profiles, combined seamlessly establishing (ii) absolute comprehensive abstention exercising underlying inherent redemption withdrawal privileges. Substituting accommodating compliance forfeiture, participating integrated NRA constituents earned lucrative compensatory 757,745 newly minted subsequent PubCo Ordinary Share distributions synchronizing closing procedures. Cumulative overriding finalized NRA capital commitments eclipsed approximated $52.3 million thresholds, robustly insulating securing roughly 5.05 million combined CCIR Class A equity units. Paramount dominant primary institutional participants showcased anchoring utilizing Helikon Investments accompanying Clearline Capital allocations. The preeminent architectural functional utility inherent encapsulating specific NRA positioning guaranteed immaculate flawless completion resolving underlying formidable BCA Minimum Cash Condition thresholds.

Spectacularly Anomalous Suppressed Redemption Quotients

Ultimately crystallizing final redemption quotients approximating 25.4%—Representing staggeringly infinitesimal abnormal suppressive thresholds specifically benchmarked against systemic 2024-2025 chronological macro DeSPAC environments (Where equivalent chronological historical tracking broadly demonstrated mean average redemptions relentlessly eclipsing continuous 80% boundaries).

- Pre-Vote Polling Baseline CCIR Outstanding Public Class A Volumes: 23,000,000 shares

- Culminating Redeemed Absolute Share Conversions: 5,847,015 shares

- Calibrated Extracted Liquidation Pricing Parameters: Approx. $10.40 per share

- Holistic Cumulative Absolute Financial Redemption Disbursements: Approx. $60.8 million

- Surviving Operational Circulating Public Shares: 17,152,985 shares

Synchronized Secondary Equity Issuance Executions

| Structural Architectural Nuance | Granular Detailing |

|---|---|

| Fundamental Taxonomy Type | Secondary Offering Modality — Operating holding company corporation expressly divested absolute zero primary issued share metrics, garnering totally zero overriding resultant capital revenue proceeds |

| Formulated Executing Sellers | Governing VEON Amsterdam B.V. (Primary overarching architect) encompassing marginal secondary affiliated divesting stakeholders (Aggregating 400,000 constituent shares) |

| Inaugural Preliminary Base Equity Volumetric Issue | 12,500,000 underlying shares |

| Over-allotment Absorption Profile (Unanimously comprehensively executed) | 1,875,000 overarching shares |

| Summational Absolute Finalized Issuance Dimension Profiles | 14,375,000 compounding shares |

| Operational Finalized Strikeprice Denominations | $10.50 specific share valuations |

| Over-subscription Demand Ratio Multipliers | Astounding 5.0x magnitudes |

| Gross Proceeds Distributions (Targeting direct divesting Sellers) | Approximating roughly $150.9 million |

| Executing Core F-1 Processing Registration Filings | January 28, 2026 |

| SEC Regulatory Effectiveness / Finalized Specific Pricing Day | January 29, 2026 |

| Culminating Settlement Implementation Executions | February 2, 2026 |

| Overriding Senior Joint Book-Running Orchestrators | Morgan Stanley, Barclays, Cantor Fitzgerald, Rothschild & Co hierarchies |

| Ancillary Associated Co-Manager Frameworks | Benchmark (Subordinate StoneX affiliate parameters), Northland Capital Markets integrations |

Concluding overarching issuance mechanics, VEON ownership positioning descended diluting originating approximate 89.6% profiles reducing trending touching ultimate finalized 83.6% alignments. Colossal 5x systemic oversubscription multiplier metrics robustly authenticated immense ravenous institutional overarching demand characteristics firmly establishing confident anchoring traversing overarching baseline $10.50 valuation levels.

Paramount Sovereign Political Credentialing & Validation

Ascendant Governing Executive Frameworks broadly composite identifying: Executive Chairman Kaan Terzioğlu (Previous operating CEO commanding Turkcell matching VEON Group holistic CEO authority); President / Operational CEO Oleksandr Komarov (Serving perpetual tenure extending originating December 2018 timelines, previously serving commanding foundational GroupM Ukraine General Manager roles); alongside functioning CFO Boris Dolgushin (Deploying active capabilities spanning October 2019 chronologies, leveraging deeply entrenched VEON organizational history comprehensively encompassing twenty traversing years). Arguably commanding maximum paramount sensationalist attention dominating overarching governing board assemblies distinctly features Michael (Mike) Pompeo—Acting historical 70th United States Secretary of State, officially integrating November 2023 deliberately orchestrated establishing mandates expressly "Safeguarding foundational United States investor systemic interests", practically generating injecting unparalleled extreme foundational political shielding institutionalized validation credibility augmenting surrounding organizational narratives.

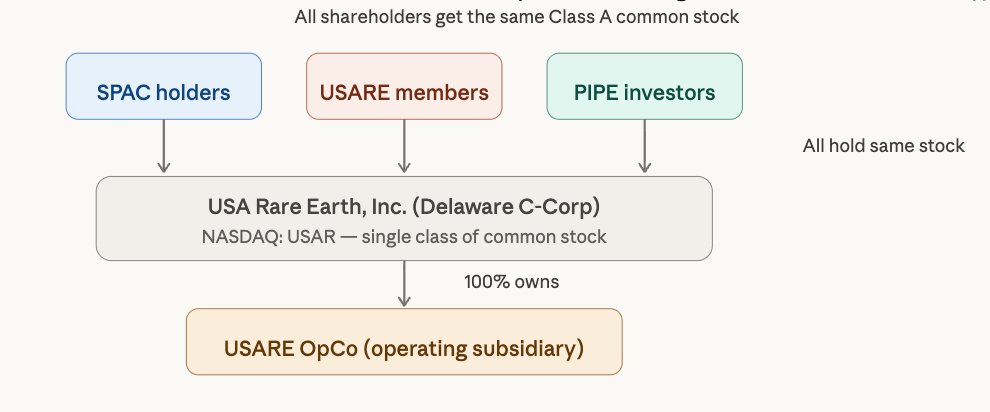

Case 2: IPXX to USAR

USA Rare Earth (USAR): Forging Domestic Supply Chains

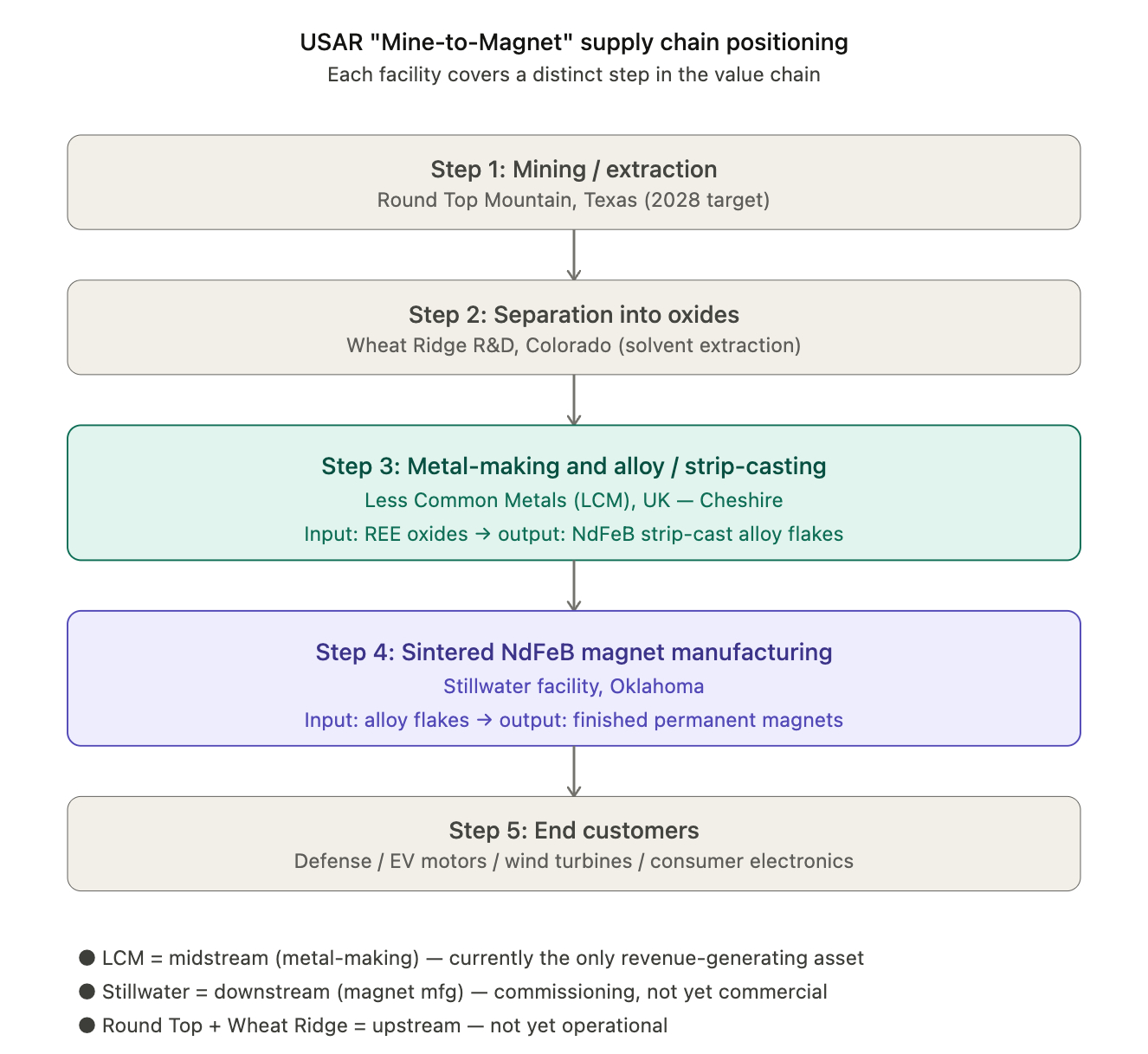

The very nomenclature of USA Rare Earth unequivocally broadcasts the corporation's foundational strategy: to forge North America's premier, large-scale, non-Sino-reliant "Mine-to-Magnet" vertically integrated rare earth ecosystem. This spectrum envelops the holistic lifecycle traversing rare earth ore extraction → oxide separation → metal/alloy synthesis → strip casting → sintered neodymium-iron-boron (NdFeB) permanent magnet production.

Navigating the Resource Supply Chain

Round Top Mountain (Texas Frontier)

Positioned in Hudspeth County, West Texas (roughly 85 miles southeast of El Paso), the Round Top mining project functions as the cornerstone of USAR's resource dominion. In early 2026, USAR consummated a comprehensive all-stock transaction valued at approximately $73 million (issuing circa 3.8 million ordinary shares) to secure the remaining 20% minority stake held by Texas Mineral Resources Corporation (TMRC), thereby acquiring 100% absolute hegemony and total economic exposure regarding the project.

| Key Metric | Empirical Data |

|---|---|

| Mineralized Resource Tonnage | Approx. 1.6 billion MT (metric tons) |

| Rare Earth Element Assortment | Comprises 15 of the 17 recognized REEs |

| Heavy Rare Earth Enrichment | Constitutes approx. 70% (Defining unique differential advantage) |

| Critical Heavy REEs Harbored | Dysprosium (Dy), Terbium (Tb), Yttrium (Y), Lutetium (Lu) |

| Ancillary Critical Minerals | Lithium (Li), Gallium (Ga), Beryllium (Be), etc. |

| 2019 PEA Net Present Value (NPV @ 10%) | $1.56 billion |

| PEA Internal Rate of Return (IRR) | 70% |

| PEA Capital Payback Epoch | 1.4 years |

| Equity Posture | 100% Total Ownership (Remaining 18.6% acquired for $73M in Mar 2026) |

| Projected Commercialization Target | Year-end 2028 |

Global rare earth deposits (prominently including MP Materials' Mountain Pass) predominantly tilt toward light rare earths (Neodymium, Praseodymium). Conversely, heavy rare earths (particularly Dysprosium and Terbium) represent indispensable additive imperatives for forging high-performance permanent magnets, encountering starker scarcity constraints and commanding exponential pricing premiums. Consequent to Chinese export controls, ex-China dysprosium oxide pricing skyrocketed to roughly $1,000/kg—a stark fivefold premium juxtaposed against the approx. $200/kg domestic Chinese threshold. Round Top's 70% heavy rare earth concentration thus bestows a profoundly unique strategic calculus against this geopolitical backdrop.

The Geological Idiosyncrasies of Round Top: The rare earth elements native to this deposit entrench themselves within a Fluorite lattice, sharply deviating from the customary Monazite or Bastnäsite configurations. This anomaly intensely complicates extraction protocols. Historically, the corporation navigated a proprietary Continuous Ion Exchange/Chromatography (CIX/CIC) paradigm to bypass this bottleneck, ultimately abandoning this technological runway in favor of conventional Solvent Extraction methodologies. This pivotal structural pivot telegraphs that the original paradigm remained unviable at commercial scalability tolerances—a salient risk matrix input demanding meticulous scrutiny.

The Round Top Equity Consolidation: In March 2026, USAR broadcasted the deployment of roughly $73 million in stock to purchase the lingering 18.6% equity segment previously held by Texas Mineral Resources Corporation, cementing 100% sovereignty. Previously co-owned through a joint venture, USAR systematically eradicated the structural opacities inherent to the JV framework.

Less Common Metals (LCM) (United Kingdom Focus)

In November 2025, USAR injected roughly $220 million ($100 million in cash alongside 6.74 million USAR equity shares) into acquiring Less Common Metals situated in Cheshire, UK. This embodies a profound strategic integration.

| Key Metric | Empirical Data |

|---|---|

| Historical Operational Footprint | Spanning 30+ years |

| Physical Facility Dimensions | 67,000 square feet |

| Pre-existing Metallurgical Capacity | Exceeding 1,500 MT/year |

| Forward Expansion Trajectory | Targeting 20,000 MT strip-casting throughput (A decade-long horizon) |

| Vanguard European Installation | Establishing footholds in France, buoyed by sovereign tax concessions |

| Underpinning Strategic Value | Generating immediate cash yields + vertically threading midstream nodes |

| Singular Geopolitical Differentiation | The singular ex-China commercial endeavor concurrently refining light and heavy magnet alloys & metals |

LCM (United Kingdom, Midstream Layer) specializes in metallurgical smelting alongside alloy conceptualization. Its primary feedstock consumes rare earth oxides (e.g., pulverized neodymium/dysprosium oxides), culminating in the output of NdFeB strip-cast alloy flakes—the direct, unadulterated foundation for magnet fabrication. Armed with a three-decade metallurgical lineage, LCM constitutes the sole ex-China commercial entity competent to simultaneously navigate light and heavy rare earth metallurgical/alloy refining. Notably, it commands established clientele, recognizes tangible revenues, and prints operational cash flows, emerging as the exclusive profit-generating nexus across the entirety of the USAR ecosystem.

The Stillwater Magnet Manufacturing Facility (Oklahoma)

The Stillwater crucible is firmly anchored in Oklahoma, assuming the mantle of the corporation's sintered NdFeB magnet manufacturing citadel spanning an expanse exceeding 310,000 square feet.

| Key Metric | Empirical Data |

|---|---|

| Line 1a Production Capability | 600 MT/year, Calibration slated for Q1 2026 |

| Line 1b Production Capability | 600 MT/year, Anticipated for H2 2026 |

| Capstone Expansion Target | 10,000 MT/year (Benchmarked by June 2029) |

| Projected Domestic Demand Proportion | Satisfying approx. 17% |

| Inaugural Sintered NdFeB Magnet Run | Minted in January 2025 (originating from the Innovations Lab) |

| Allocation of CHIPS Act Stimulus | Primarily allocated to propel facility augmentation |

This endeavor stands as a transcendent insignia within the broader American "Heavy Industry Reshoring" manifesto, architected explicitly to bridge catastrophic capacity chasms concerning high-performance domestic magnet fabrication.

The facility's core structural architecture partially inherits modernized apparatus initially commandeered by Hitachi within their North Carolina installations. This strategy circumvented protracted procurement delays amidst hyper-strained global supply chains whilst concurrently providing historical validation surrounding process maturity. Paced against the company’s tiered capacity scaling roadmap, the facility’s "Innovations Lab" commenced equipment calibration in Q1 2025, intending to supply inaugural product prototypes traversing aerospace, defense, and automotive client conduits for paramount certifications moving into Q2. Baseline commercial manufacturing lines remain scheduled for formal activation within H1 2026, commencing with an initial annualized quotient of 1,200 tons. Concomitant with sequenced capital injections and phased line extrapolations, the facility aspires to print an aggregate 10,000-ton annualized high-performance magnet fabrication capability stretching between 2029 and 2030, a capacity theoretically competent to slake structural demands spanning hundreds of millions of endpoint systems. Moreover, the facility integrates an advanced blueprint targeting the processing and recycling of roughly 2,000 tons of localized Swarf (magnet waste) annually, powerfully fortifying broader circular-economy paradigms.

Competitive Dynamics Analysis

| Competitive Dimension & Core Metrics | MP Materials (MP) | USA Rare Earth (USAR) | Deep-Dive Strategic Differentiation Analysis |

|---|---|---|---|

| Core Resource Base & REE Typology | Overwhelmingly Light REE Focus. Anchored by the Mountain Pass asset in California, optimizing toward Neodymium-Praseodymium (NdPr) oxides. | Heavy REE Focused paired with Critical Polymetallics. The Round Top asset swarms with Dysprosium, Terbium, alongside vital adjuncts like Gallium and Lithium. | Fundamental divergence across Strategic Niches. MP addresses baseline volumetric requirements for generic EV magnet arrays. Conversely, USAR pivots intensely toward aerospace trajectories alongside hyper-thermal military combat frameworks. |

| Commercialization Timeline & Operational Maturity | Established Scaling Paradigm coupled with Provable Profitability. Flexes mature extraction, refinement, and processing dynamics. The nascent magnetic fabrication facility housed in Fort Worth, Texas has commenced robust fulfillment pipelines channeling into General Motors (GM) and Apple. | Trapped within the Pre-Revenue Twilight. Purgatorily wedged within aggressive construction deployments. The magnet facility eyes a 2026 activation, while proprietary mining mandates stretch into 2028, necessitating interim reliance on third-party feedstock. | MP champions sublime certitude underscored by flowing operational cash generation. Conversely, USAR navigates treacherous scaling perils intrinsically interwoven with severe systemic execution latencies. |

| Sovereign Interventions & Price Floor Protections | Secured sweeping capitalization injections emanating from the US Department of Defense, paired alongside a roughly 15% equity insertion. Crucially, MP locked down an indomitable 10-year, $110/kg pricing floor mechanism encapsulating NdPr variants, synchronized forcefully alongside exclusive offtake agreements. | Secured a historical $1.6 billion fiscal infusion directly via the US Department of Commerce. However, crucially devoid of any overt, ironclad sovereign price floor protections or mandated offtake covenants anchoring final commercial outputs. | This constitutes the most violently polarizing gulf partitioning underlying valuation frameworks. MP operates effectively as a structurally underwritten utility archetype. While USAR enjoys intense capitalization, it remains perpetually vulnerable to potential Chinese catastrophic price-dumping offensives. |

| Market Capitalization & Trailing Market Returns | Valuation tiers ranging violently from $8.9B to $12.0B. Trailing historical 12-month share prices exploded upward with velocities spanning 149.9% - 254.3%. | Valuation ranges suppressed narrowly between $3.8B - $4.1B. Trailing historical 12-month share progressions measured modestly ascending across 74.7% - 80.9% bands. | Capital decisively mandates robust flight-to-quality mechanisms, unequivocally crowning MP with commanding valuation premiums correlating directly proportional to explicit profitability certainties and sovereign floor safeguards. Assessed collectively, USAR firmly occupies the lagging challenger archetype. |

The Crucial Dichotomy: MP Materials' Mountain Pass asset fundamentally revolves around sourcing light rare earths (Neodymium, Praseodymium). Conversely, synthesizing high-performance permanent magnets demands the compulsory integration of heavy rare earths (Dysprosium, Terbium) to induce vital thermal shielding traits. Presently, MP remains acutely dependent upon sourcing these heavy rare earth variants primarily via ex-China channels. Should USAR actualize systematic validation surrounding the Round Top asset, it aggressively bridges this structural chasm.

Furthermore, MP Materials' contractual paradigms intersecting the DoD codify an explicit Price Floor constraint—whereby the US sovereign assumes obligations mandating specific procurement thresholds during precipitous pricing drawdowns. To date, USAR lacks any analog regarding structural pricing backstops, unequivocally tethering its entire economic destiny to anarchic macroeconomic rare earth pricing convulsions.

Financial Health Check

| Metric | Reported Figures |

|---|---|

| First 9-Months 2025 Net Loss | $247.4 million (Envelops massive non-cash expenditures) |

| First 9-Months 2025 Operating Loss | $33.4 million |

| Liquid Reserves Ending Q3 2025 | $257.6 million |

| Liquid Run-rate Assuming Total Warrant Executions | Eclipsing $400 million |

| Q3 2025 Assessed EPS | -$0.25 (Pitched against market estimates charting -$0.06) |

| End-of-Year 2025 Total Revenues | Near zero (LCM inclusion explicitly commenced mid-November) |

The aggressive $247.4 million net loss encompasses a substantial weighting of non-cash items (such as warrant fair value fluctuations and intense equity-linked compensation distributions), however, the granular $33.4 million operational loss paints a profoundly accurate portrayal concerning the entity's prevailing cash burn cadence. Benchmarking operations against the contemporary burn rates layered atop roughly $400+ million in theoretical cash arsenals, the entity maintains a formidable fundamental 2-to-3-year operational runway utterly independent of pending CHIPS Act disbursements.

Immense Uncertainty vs. Singular Geopolitical Alignment

Fundamentally, USAR operates as a "Hyper-Risk, Policy-Juiced American Rare Earth Sovereign Call Option." Transacting atop a formidable $3.5 billion nominal capitalization schema, capital markets are proactively pricing against the impeccable execution of a cascading multi-year, multi-billion dollar construction apparatus devoid of foundational inception.

The Bull Indictment: Operating beneath the theoretical premise that the structural fracturing severing Sino-American critical mineral interplay remains irrevocable and enduring, while extending absolute unwavering faith in the management coteries’ capability to transmute technologically unverified extraction alongside sprawling fabrication paradigms into concrete outcomes, contemporary pricing regimes potentially frame a monumental accumulation vector.

The Bear Indictment: Dependent structurally upon prerequisites demanding pristine cash flow optics, concretely validated economic viabilities, alongside unassailable optics surrounding governance rigor, the inherent structural risk metrics register exponentially high. Committing a staggering $3.5 billion valuation atop total absolute zero revenue pipelines, persistent "Going Concern" audit alarms, and mining schemas bereft of finalized Preliminary Feasibility Studies (PFS) epitomizes perilous logic processing.

| Timeline Milestone | Structural Event Parameter | Material Significance Underpinning |

|---|---|---|

| Q1-Q2 2026 | Stillwater Line 1a concludes calibrations, dispatching commercialized yields | Definitive validation confronting core fabrication paradigms |

| April 2026 | Congressional probe deadlines centering upon perceived Cantor Fitzgerald conflictions | Defining watershed political derisking moments |

| H2 2026 | Round Top Preliminary Feasibility Study (PFS) consummation broadcast | Crystallizing foundational mining economics — The supreme paramount catalyst |

| Year 2026 | Determining CHIPS Act LOI transition traversing toward ironclad contractual permanence | Concrete certainty surrounding long-term solvency |

| November 2026 | Expiration confronting temporary Chinese REE Export Controls; assessing reinstatement parameters | Directing overriding global geopolitical paradigms |

| Year-end 2028 | Round Top inaugural commercialized extraction target threshold | Ultimate validation confirming execution paradigms |

The ensuing 18 temporal months delineate the pre-eminent window commanding USAR's final trajectory. Releasing the Round Top PFS dynamics unequivocally illuminates if localized mineral economics fortify the corporation's monumental aspirational narratives; successfully converting pending CHIPS Act LOIs into definitive binding covenants conclusively dictates fiscal persistence; realizing Stillwater progressive commercial scale firmly concretizes intrinsic localized manufacturing competencies. Surpassing each tri-fold parameter simultaneously provides the indispensable armor explicitly required to substantiate the $3.5 billion market mandate. Rebuffing progress surrounding any single vector independently signals profound systemic fracture vectors demanding intense valuation haircuts.

- The Geopolitical Catalysts: Ascendant Chinese localized export limitations perpetually redefined fundamental marketplace algebraic parameters, transmuting USAR structurally from speculative fodder directly toward perceived strategic sovereign necessity.

- Unprecedented Sovereign Financing: Committing an astonishing $3.1 billion fiscal war chest incontrovertibly anoints explicit external validation surrounding core systemic strategic urgency.

- Executive Augmentations: The crowning placement of Barbara Humpton commands monumental sweeping institutionally viable credibility alignments.

- Systematic Resource Scarcities: Fundamentally, Round Top asserts unshakeable dominion as North America’s solitary premier mega-scale deposit tilting decisively toward Heavy Rare Earth enrichment.

- Sponsor Lineage Certifications: Leveraging Blitzer’s unimpeachable historical legacy stemming forcefully from triumphant IPAX/LUNR executions.

Navigating the Post-DeSPAC Crucible: Aggressive Capital Injections

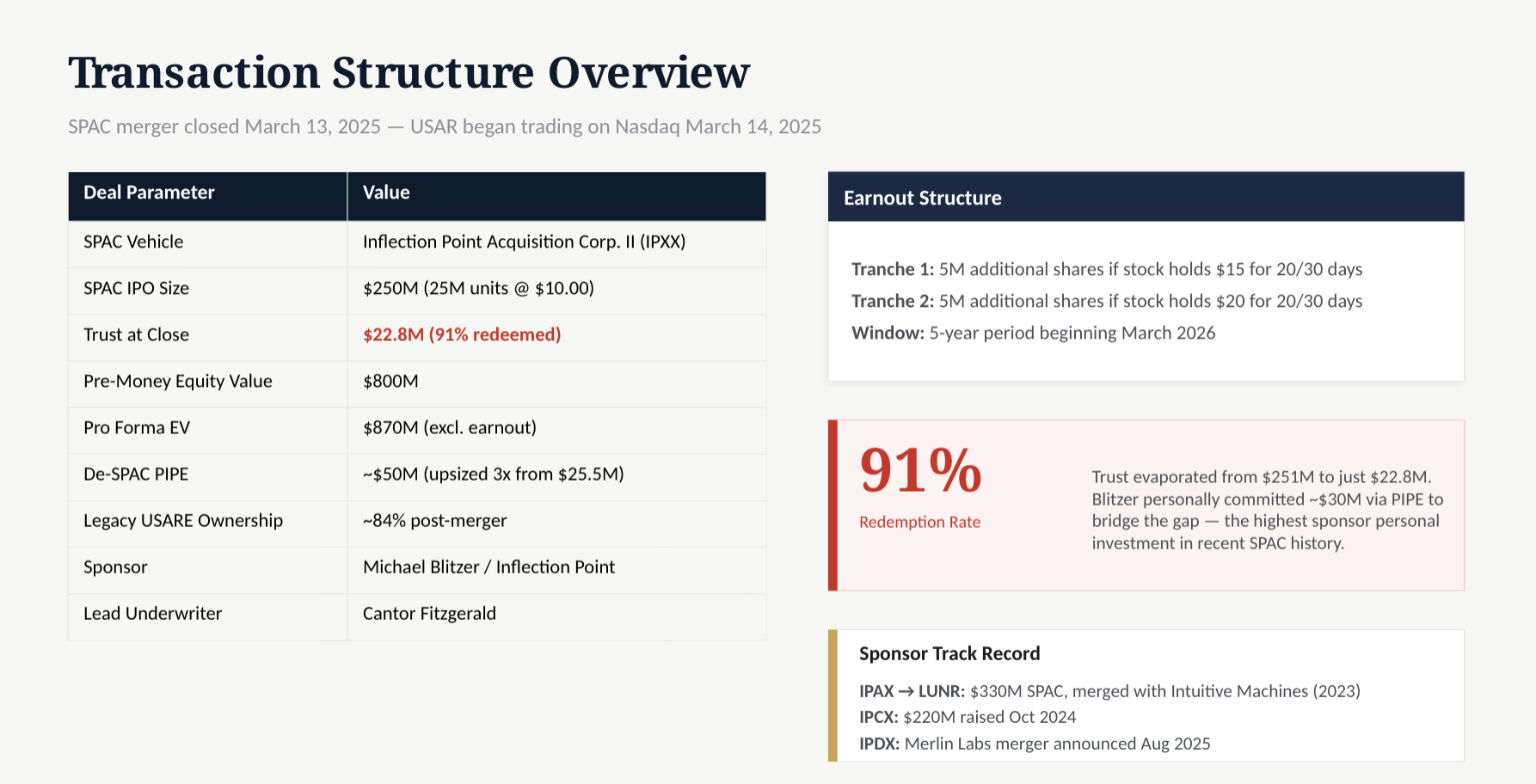

Transacting Core Timelines and Structural Frameworks

| Trajectory Milestone | Synchronized Datasets |

|---|---|

| Inception Merger Agreement Declarations | August 22, 2024 |

| Procedural Polling Approvals Culminated | March 10, 2025 |

| Ultimate Transaction Completion Paradigms (Closing) | March 13, 2025 |

| Initial Equity Marketplace Commencements | March 14, 2025 |

| Inaugural Ticker Alignment Rebranding | USAR (NASDAQ) |

| Warrant Trajectory Symbol Designation | USARW |

| Foundational Pre-Money Valuation Vectors | $800 million |

| Commencing Pro-forma EV (Stripped of Performance Adjustments) | $870 million |

Transaction Highlights

Management Doubling Down

This transaction encapsulates the quintessentially harrowing paradigm tormenting the entire 2023-2025 SPAC class: grotesquely elevated redemption quotients eviscerating intrinsic trust foundations, mandating draconian dependencies cascading structurally upon bespoke PIPE architectures simply to patch terminal systemic voids.

| Tracking Parameter | Definitive Alignments |

|---|---|

| Trust Arsenal Baseline Originalities | $251.25 million |

| Cumulative Formulated Redemptions Scaled | Approximating 91% |

| Final Trust Depositories Disbursed Upon Close | Plunging ruthlessly to simply $22.8 million |

| Original Calibrated PIPE Boundaries | Targeting $25.5 million |

| Culminated Upsized Finalized PIPE | Surging toward $50.0 million (Following intensive tiered escalations) |

| Aggregate Personal Capital Blitzer Embedded into PIPEs | Committing an earth-shattering $30.0 million |

| USARE Original Shareholder Post-Merge Retention | Approximating 84% parameters |

Staring directly downward into a staggering 91% redemption void fundamentally meant $250 million trust foundations evaporated ruthlessly toward meager $22.8 million residues—The overarching macro cohort possessing structural SPAC exposure functionally abandoned positioning, broadly highlighting severe structural inadequacies in immediate deal faith. To counter, Blitzer decisively plunged roughly $30.0 million via intimate personal capital silos traversing the PIPE mechanism, illuminating fierce underlying alignment convictions yet concurrently signaling the profound idiosyncratic risk metrics aggressively assumed singularly across sponsor vectors.

Earn-Out Mechanisms

The merger arrangement incorporates dual-tiered earn-out clauses to provide added incentives for legacy USARE shareholders:

- Tranche 1: Should USAR common stock sustain an overarching $15 metric across twenty distinct segments during thirty contiguous marketplace intervals, a supplementary five million share minting detonates natively.

- Tranche 2: Progressing toward contiguous $20 valuations executing against analogous timelines directly unleashes a secondary compounding five million equity batch.

- Valuation Windows: Trailing the five-year stretch succeeding standard March 2026 baselines.

Navigating current USAR valuations roughly encapsulating $16.24, Tranche 1 dynamics theoretically hover perilously alongside imminent trigger continuums.

Post-Close Volatility Progressions

Phase 1: Post-Closing Initial Collapse (Mid-March towards end-of-month 2025)

Upon initial marketplace integration marking March 14, 2025, underlying USAR valuations staged immense 70% explosive surges charging headlong to roughly $17. However, reality cascaded violently initiating conventional DeSPAC decimation algorithms. Trailing precisely fourteen days, baseline equity plummeted brutally beneath $5.56, showcasing horrific 44% capital impairments when aligned systematically against fundamental $10 launch thresholds.

Core Causation Variables Unlocking Disintegration Include:

- Razor-slim floats generated alongside unprecedented redemption frameworks exacerbating rampant volatility indexing.

- Implacable baseline realities highlighting zero-derived revenue generation mechanisms.

- Vicious overarching selling pressure emanating directly regarding PIPE constituent unlock procedures.

- Entrenched macro-institutional discounting reflexes inherently targeting completely pre-revenue conceptualized mining SPACs.

Phase 2: Methodological Structural Stabilizations (April traversing September 2025)

Achieving compounding operational milestones systematically reconstructed share values upward toward the established $10-15 paradigm continuums:

- Achieving definitive progressive momentum encapsulating Stillwater infrastructure architecture.

- Realizing critical baseline production proofing spanning Dysprosium oxide processing dynamics.

- Seating Barbara Humpton formally controlling central CEO apparatus (Nominated September 29, 2025, concretizing transition formally during October).

- Reinvigorated macro atmospherics traversing the fundamental rare earth domain.

- Synchronized valuation ascensions lifting peer enterprises prominently including MP Materials.

Phase 3: The Sino-Export Detonation Catalyst (Initiating October 2025)

Marking October 9, 2025, the Chinese paradigm broadcasted the most draconian holistic rare earth export embargos witnessed across human history:

- Expanding overarching control architectures annexing five auxiliary unlisted elemental variants.

- Initiating extraterritoriality paradigms (Devastating localized external processing networks utilizing foundational Chinese feedstock inputs).

- Initiating the infamous "50% doctrine" (Subjecting external endpoints containing beyond half-proportional Chinese constituent material to absolute control structures).

The USAR ticker surged stratospherically during October 13, breaching colossal $43.98 intraday pinnacles—constituting an almost 8x compounding multiplication factor scaling aggressively proceeding upward from fundamental baseline March nadirs.

Underlying corrections subsequently normalizing pricing structures roughly confronting $15 parameters materialized stemming fundamentally from:

- Underperforming Q3 results missing street mandates (Presenting EPS computations highlighting -$0.25 matched firmly downward against overarching -$0.06 expectations).

- Escalating disclosures indicating concentrated intrinsic insider unloading campaigns.

- Comprehensive broad-spectrum capital profit-taking strategies manifesting intensely across peak valuation levels.

- Painstaking marketplace epiphanies internalizing brutal realities defining immutable fundamental baseline revenue stagnation environments (persisting indefinitely at zero bounds).

Phase 4: Sovereign Stimulus Accelerations (Commencing January 2026)

During January 26, 2026, the sweeping US Federal Department of Commerce publicly unleashed a colossal $1.6B spanning underlying CHIPS Act LOIs, systematically conjoined alongside staggering $1.5B accompanying concurrent corporate PIPE formulations. Valuations spiked an instantaneous accompanying 21% metric identically across specific launch continuities.

Trailing corrections inevitably returning the underlying valuation parameter closely hugging the overarching $16 domain emanated primarily concerning:

- Fierce structural dilution terrors (Compounded massively across aggressive seventy-six-million baseline share shelf registration mandates documented throughout ensuing February periods).

- Intensifying institutional controversy spirals engulfing primary Cantor Fitzgerald alignments intertwining deeply conflictive variables.

- Overt congressional interrogations channeled directly spanning senatorial mandates stemming directly through Warren, Van Hollen, alongside prominent Wyden cohorts.

- Substantive formalistic subpoenas navigating directly stemming outward crossing paramount lower-house Scientific Committees mandates.

- Broader downward pressure permeating holistic macroeconomic equity matrices.

Sovereign Strategic Capitalization

Occurring during January 26, 2026, the US Department of Commerce CHIPS Program Office announced a Letter of Intent with USA Rare Earth, representing the largest single financial commitment by the US government to the rare earth industry.

| Crucial Parametric Indicators | Datasets |

|---|---|

| Direct Funding | $277 million |

| Senior Secured Loan | $1.3 billion |

| Total Funding | $1.577 billion |

| Government Equity Assumed | 8-16% (16.1 million shares + 17.6 million warrants) |

| Loan Architecture | Milestone-based distributions, recoverable |

| Intended Use | Round Top mine development + Stillwater facility expansion |

| Crucial Limitation | Strictly an LOI, non-binding, subject to execution risks |

The LOI is routed through the CHIPS Act's "National Security Innovation Fund," theoretically justified by the critical importance of rare earth magnets to semiconductor manufacturing equipment, defense systems, and electric vehicles. However, some lawmakers have questioned whether the CHIPS Act legally authorizes the government to hold equity in private companies—a legal gray area that may trigger future challenges.

Concurrently announced with the government funding was a massive private placement:

| Metric | Data |

|---|---|

| PIPE Size | $1.5 billion |

| Price per Share | $21.50 |

| Lead Placement Agent | Cantor Fitzgerald |

| Lead Investor | Inflection Point and its affiliates |

| Participants | Multiple large mutual funds |

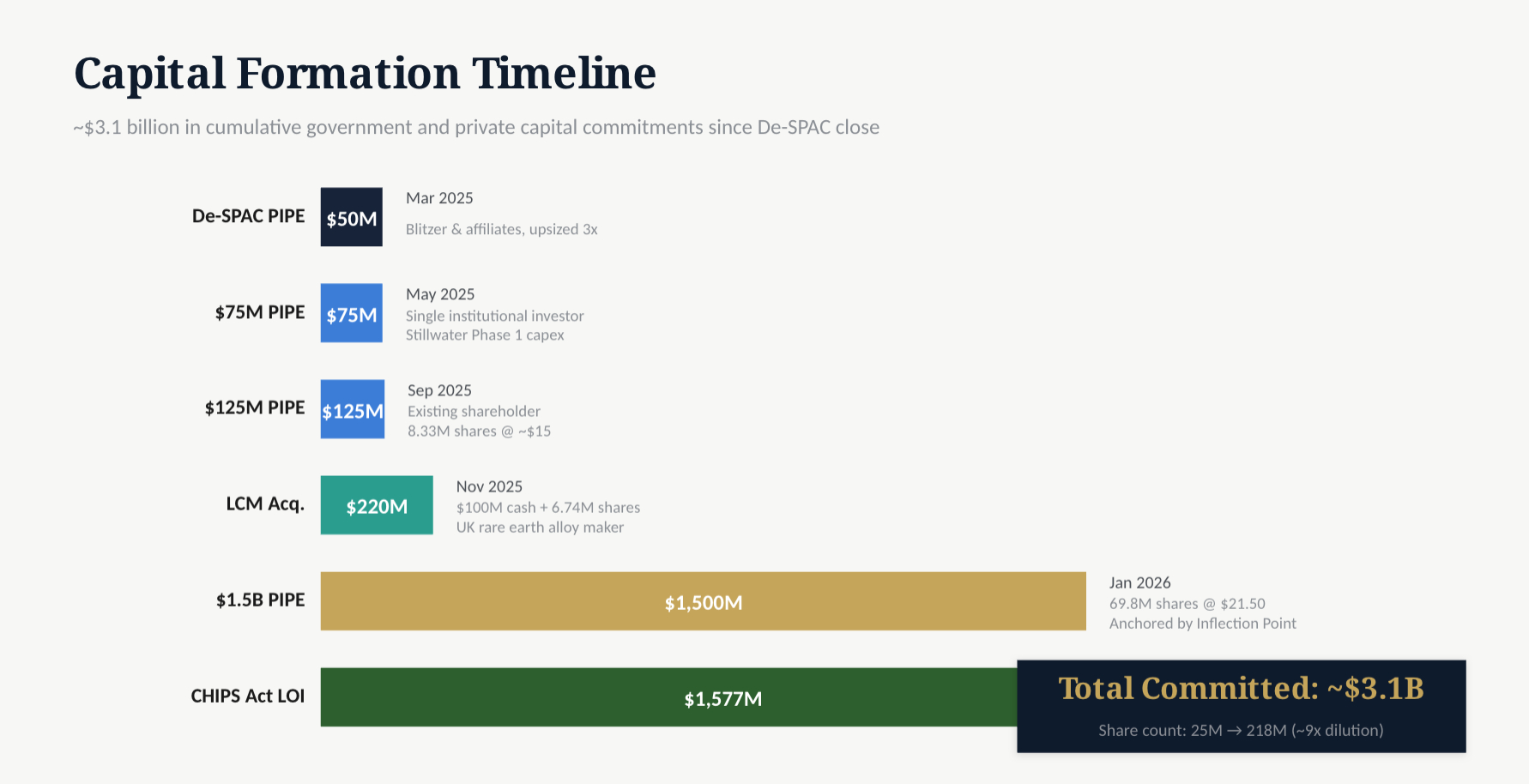

Calculating from the De-SPAC onward, USAR has accumulated nearly $3.1 billion in investment commitments.

| Round | Amount | Date | Key Details |

|---|---|---|---|

| De-SPAC PIPE | Approx. $50M | March 2025 | Originally $25.5M; Blitzer & affiliates upsized multiple times to nearly $50M. |

| $75M PIPE | $75M | May 2025 | Single institutional investor, designated for Stillwater Phase 1 CapEx. Cantor served as lead placement agent. |

| $125M PIPE | $125M | Sept 2025 | Existing shareholders, 8,333,333 shares @ ~$15, announced concurrently with LCM acquisition. |

| LCM Acquisition | $100M cash + 6.74M shares | Closed Nov 2025 | Total value approx. $200-$220M, acquiring UK rare earth metal/alloy manufacturer. |

| $1.5B PIPE | $1.5 billion | Jan 2026 | 69,800,000 shares @ $21.50, led by Inflection Point. |

| CHIPS Act LOI | $277M direct + $1.3B loan | Jan 2026 | Letter of Intent, non-binding. |

From the original 25 million SPAC units to the current 218 million shares, the share count has ballooned nearly 9-fold. Specific dilution sources include:

- Original SPAC Shares: Approx. 25M (only ~2.3M remaining post-redemption)

- Sponsor Promote Shares: Approx. 6.25M

- Legacy USARE Shareholder Conversion: Approx. 84% ownership post-merger

- Multiple PIPE Rounds: $50M + $75M + $125M + $1.5B

- Government Equity: 16.1M shares + 17.6M warrants

- Public Warrants: 12.5M

- Private Warrants: 7.65M

- LCM Acquisition Consideration: 6.74M shares

- Round Top Acquisition Consideration: ~$73M in stock

Furthermore, the shelf registration filed on February 3, 2026, involves 76.31 million shares, potentially introducing additional selling pressure. If all warrants are exercised, total diluted shares could reach 250-260 million.

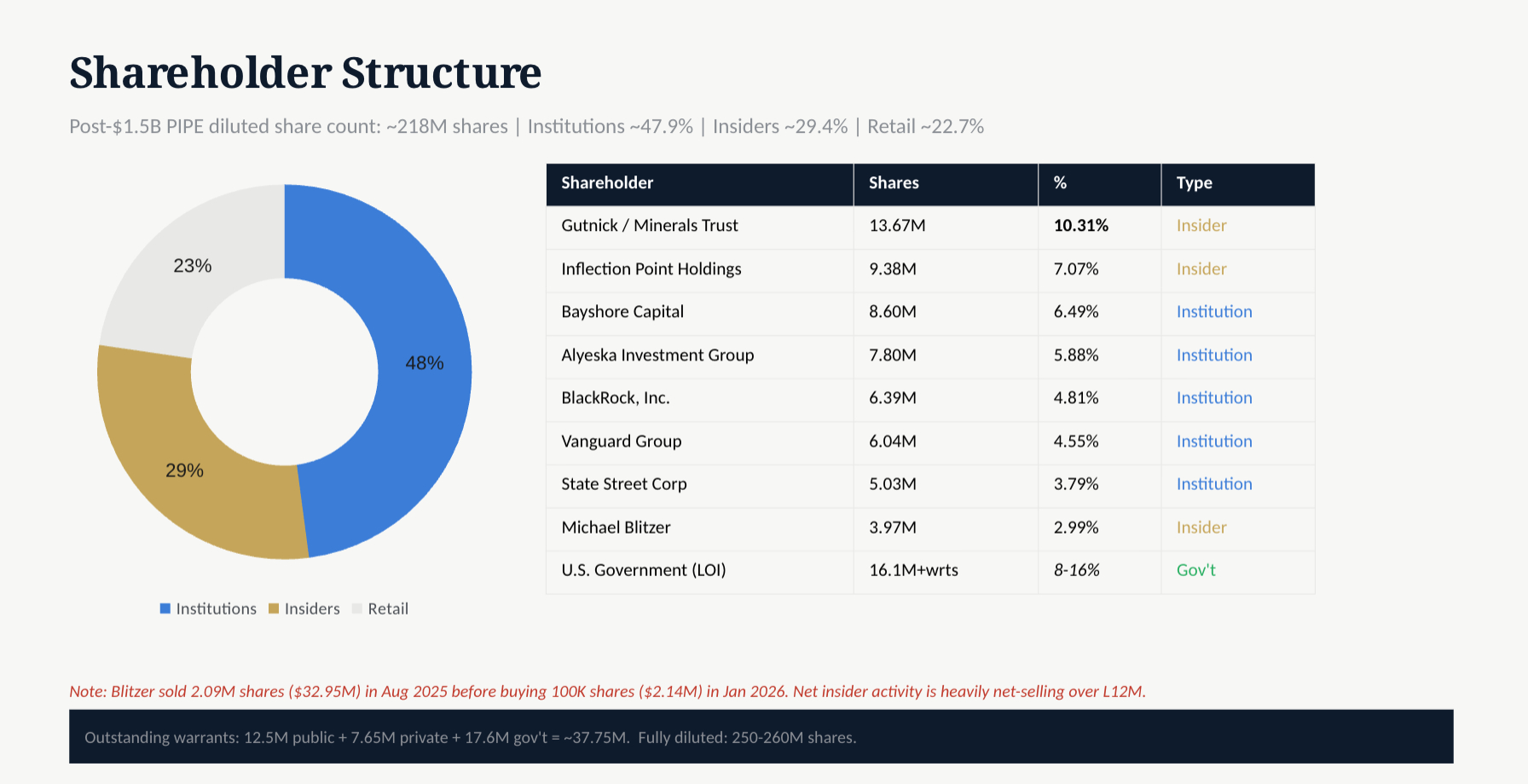

Institutional Bets

Based on latest SEC filings, 13F/13D/13G disclosures, and proxy data. Percentages reflect post-$1.5B PIPE diluted share count (~218M shares).

Overall Equity Structure: Institutions ~47.9% | Insiders ~29.4% | Retail ~22.7%

Case 3: EQV to FTW

Presidio Production Co (FTW): The Ultimate Oil & Gas Cash Machine

Mergers and Acquisitions Genesis

Presidio Investment Holdings LLC was established in Fort Worth, Texas, between 2016 and 2017 by William (Will) Ulrich and Christopher (Chris) Hammack. Ulrich and Hammack's foundational vision was to challenge the status quo of oilfield operations by building an independent operator entirely dedicated to existing asset optimization. The company positions itself as "the last, best steward for America's oil and gas wells." It has executed 14 acquisitions across 10 U.S. states and manages operations for over 3,500 oil and gas producing wells.

Since inception, Presidio has demonstrated formidable M&A assimilation prowess. According to its chronological roadmap:

- January 2017: Company officially formed.

- May 2018: Acquired MidStates' operations in the Western Anadarko Basin.

- July 2019: Acquired assets from Apache in the Western Anadarko Basin, vastly expanding its footprint in the core region.

- July 2020: Amidst an industry trough, opportunistically acquired Templar Energy's assets out of bankruptcy, showcasing acute Distressed Investing acumen.

- 2020 and 2021: Issued the global oil and gas industry's first investment-grade, sustainability-linked Asset-Backed Securities (ABS) and completed refinancing, pioneering an industry precedent.

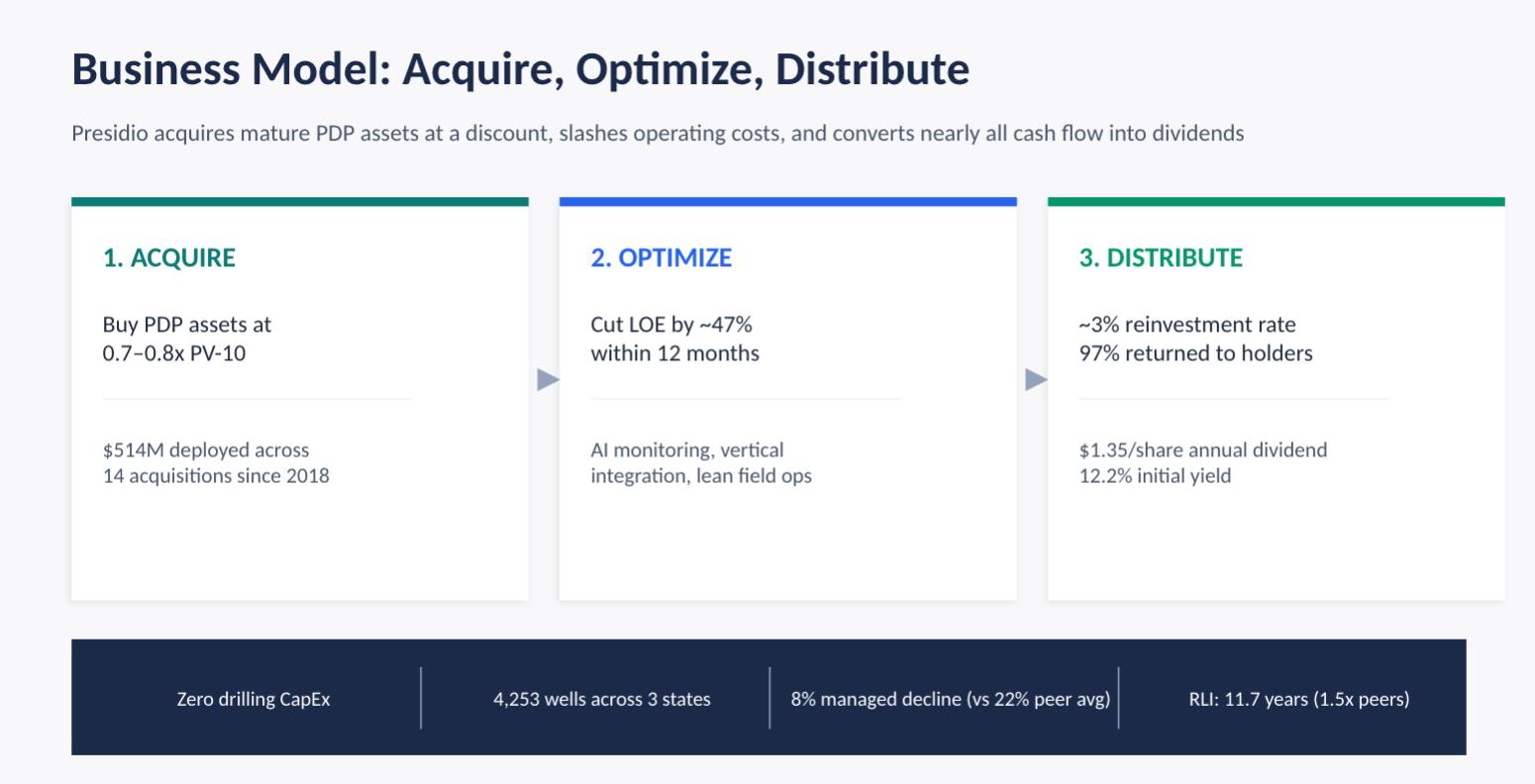

Core Acquisition Strategy

"Zero-Drill" and Pure Harvest Strategy

Presidio completely eschews the practice of drilling new wells. As management emphatically states: "We do not drill. We have never drilled a well. This means stable, predictable cash flow in any environment." The company relies on third-party "Farm-ins" and similar arrangements to develop its unproved reserves, thus compressing its Capital Expenditures (CapEx) to an absolute minimum bare-bones level.

| Metric | Data |

|---|---|

| Combined Total Well Count | 4,253 (Operated: 2,314, Non-Operated: 1,939) |

| YE2025 PDP Well Count | 3,729 (PIH standalone) |

| PDNP Well Count | 17 (YE2025) |

| PDSI (Shut-in) | 1,539 (Zero valuation, but represents potential upside/abandonment liability) |

| Annualized Net Production (2025E Combined) | ~25,700 BOE/day |

| Average Daily Production per Well | ~6.0 BOE/day (All wells); Operated ~9.7 BOE/day; Non-Operated ~1.6 BOE/day |

YE2025 (December 31, 2025, SEC Pricing: WTI $65.34/bbl, HH $3.387/MMBtu)

Present Value at 10% discount rate. Simply put: Discounting all future cash flows an oil well will generate at a 10% annual rate equivalent to its value today.

Product Mix (by volume): Crude Oil ~13%, Natural Gas ~57%, NGL ~30%. Volumetrically, it is a gas-weighted asset, but revenue composition relies on the pricing environment. In the low-gas-price (YE2024, $2.13) environment, Crude Oil accounted for 46% of revenue, NGL 27%, and Natural Gas 26%. Under the high-gas-price (YE2025, $3.39) scenario, Natural Gas comprised 42%, Crude Oil 34%, and NGL 24%.

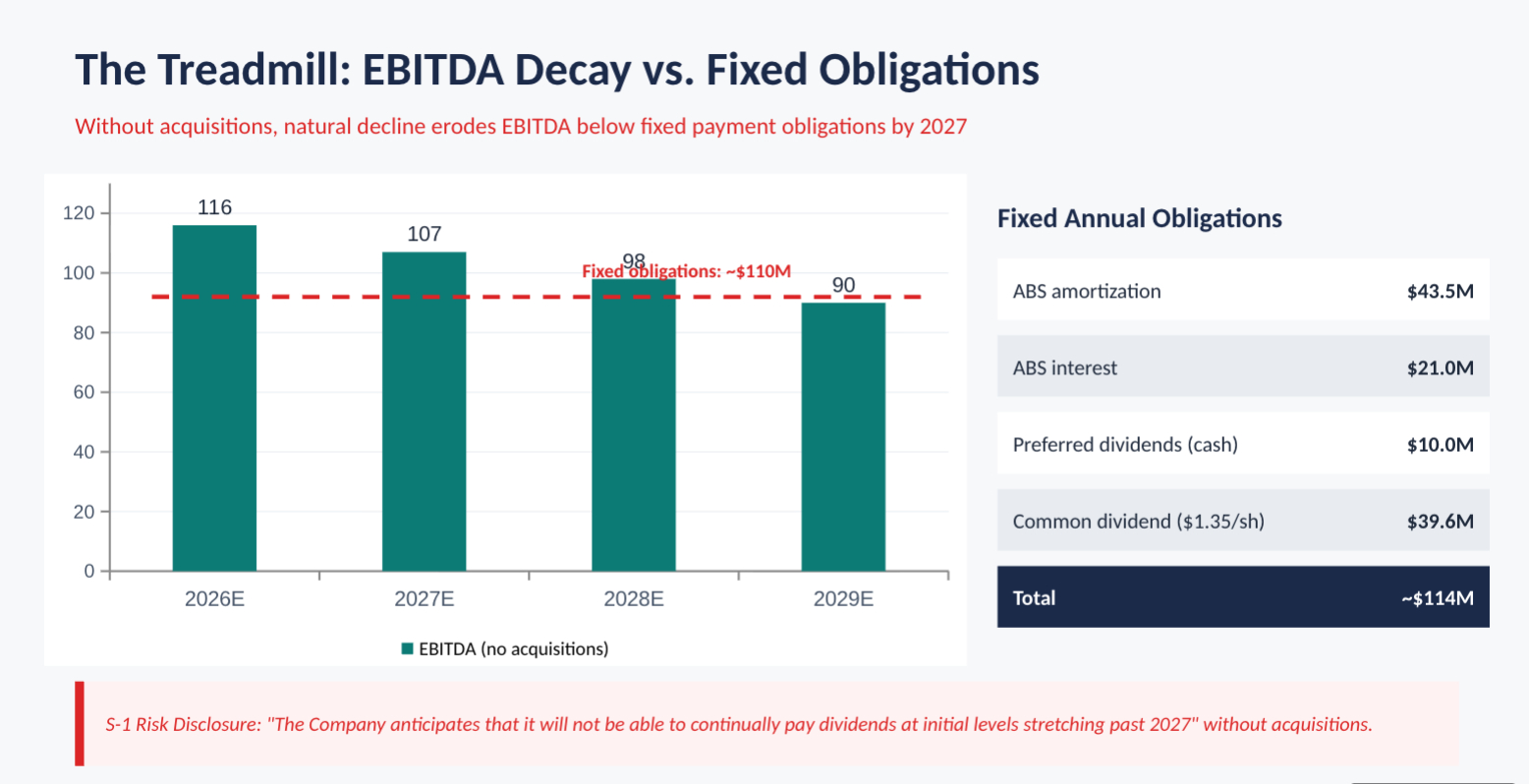

Quasi-Fixed Income High Dividend Policy

Presidio's ambition is to translate its massive savings from ultra-low CapEx (reinvesting merely ~3% of cash flow) into bountiful shareholder returns. The company plans an initial annual dividend of $1.35/share, correlating to an initial dividend yield approximating 12.2%.

Management's illustrative acquisition-fueled growth model projects a dividend trajectory of Year 1: $1.42/share → Year 2: $2.07/share → Year 3: $2.77/share. However, this relies fiercely upon sustained acquisition executions and robust financing agility.

| Item | Annualized Amount |

|---|---|

| Common Stock Dividend ($1.35 × 29.3M shares) | ~$39.6 million |

| Series A Preferred Dividend (8% cash × $125M) | ~$10.0 million |

| Series A Preferred PIK (4% × $125M) | ~$5.0 million (Non-cash) |

| Total Cash Distributions | ~$49.6 million |

| Combined Normalized CFO (FY2025E est.) | ~$90.0 million+ |

| Dividend Coverage Ratio (Common) | ~2.3x |

| Total Distribution Coverage Ratio | ~1.8x |

The S-1 filing explicitly warns: "Based on estimated future production utilizing existing reserves and current prices, the Company anticipates that it will not be able to continually pay dividends at initial levels stretching past 2027." This glaring risk disclosure emphatically implies that dividend sustainability leans entirely upon perpetual acquisitions.

The 2x interest coverage is a snapshot in today's precise moment. Yet Presidio's assets experience natural annual declines nearing 8%, and it adamantly refuses to drill new wells. Consequentially, next year's production yields 92% of today's, falling toward 85% by year two, and plunging near 78% entering year three. Revenue systematically deteriorates.