The global data center industry is in the midst of an unprecedented "supercycle." The 2024 total market is estimated at $350–390 billion, and powered by the explosive demand for AI compute, is projected to exceed $650 billion by 2030 at a CAGR of 9–11%. The headline numbers are even more striking: in Q3 2025 alone, global hyperscale capex reached $142 billion — a roughly 180% year-over-year increase (Synergy Research); Dell'Oro Group reports that full-year 2025 data center capex grew 57% YoY, with 2026 projected to cross $1 trillion. Severe supply-demand imbalance is the defining feature of the current market — the global weighted average vacancy rate has fallen to a record-low 6.6% (CBRE Q1 2025), with North American core markets at just 1.4% and Singapore below 2%. Power access has replaced land and capital as the primary bottleneck constraining industry growth.

Chapter I: Global Data Center Market Overview

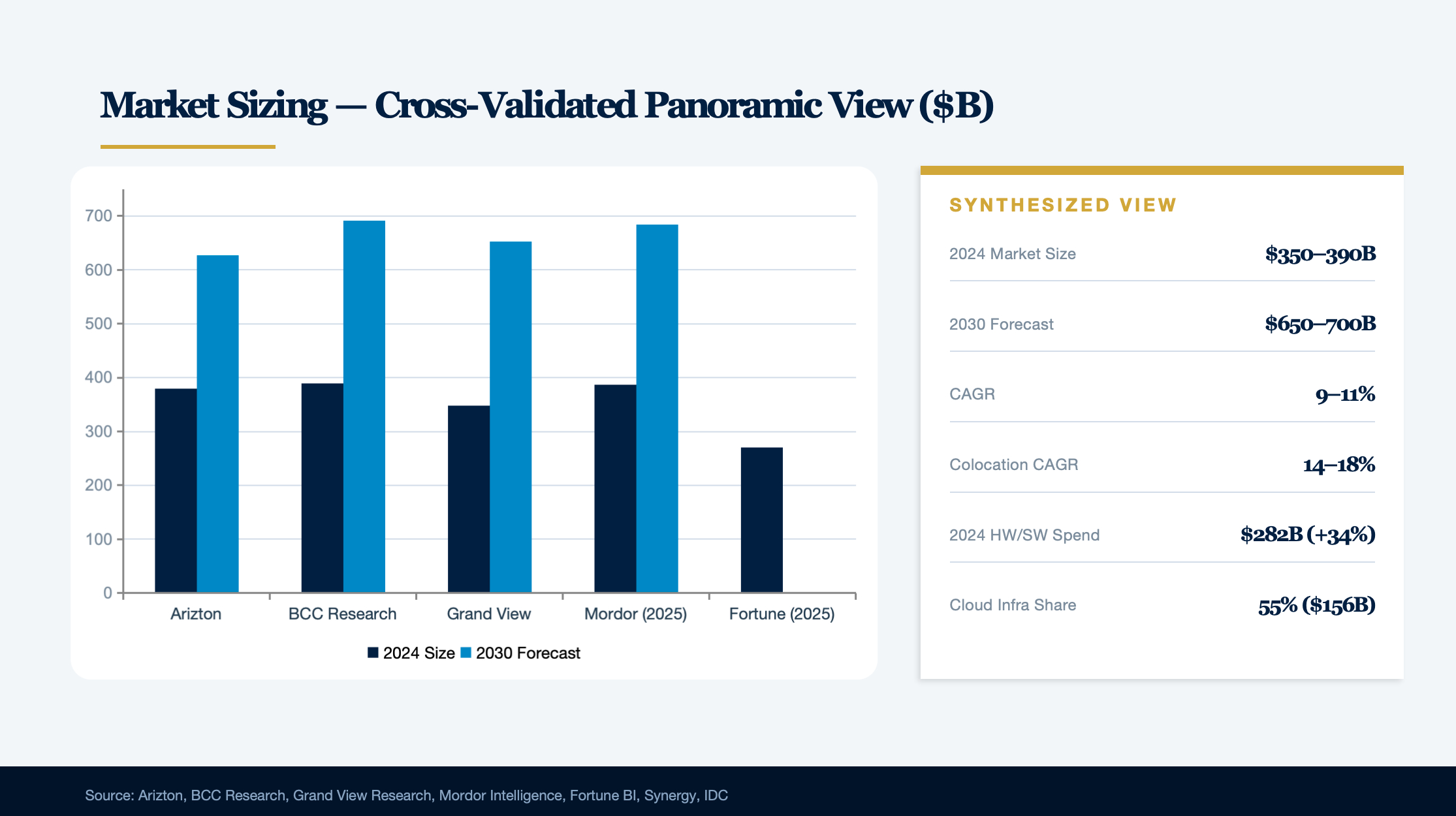

1. Total Market Size: A Cross-Validated Panoramic View

Market Revenue and Growth

Due to methodological differences (whether IT hardware, software, and construction investment are included), market-sizing figures vary across research firms, but the trend is consistent. The following is a cross-reference of 2024–2030 data from major institutions

| Institution | 2024 Size | 2030 Forecast | CAGR | Publication Date |

|---|---|---|---|---|

| Arizton | $379.3B | $627.4B | 8.75% | 2025 |

| BCC Research | $389.0B | $691.6B | 10.6% | December 2025 |

| Grand View Research | $347.6B | $652.0B | 11.2% | 2025 |

| Mordor Intelligence | $386.7B (2025) | $684.4B (2031) | 9.98% | January 2026 |

| Fortune Business Insights | $269.8B (2025) | — | 11.1% | 2025 |

Synthesized view: On a full-scope basis including infrastructure investment, the 2024 market size of $350–390 billion is the reasonable range, growing to $650–700 billion by 2030 at a 9–11% CAGR.

Within sub-segments, the colocation market is experiencing the strongest growth. Grand View Research estimates the 2024 global colocation market at $69.4 billion, with a CAGR as high as 16.0% (reaching $165.5 billion by 2030). Mordor Intelligence presents a more aggressive view — $105.9 billion in 2025 at an 18.63% CAGR. MarketsandMarkets takes the middle ground at a 14.4% CAGR.

On the hardware and software layer, Synergy Research Group's January 2025 data shows 2024 global data center hardware and software spending reached $282 billion, a 34% YoY jump, with public cloud infrastructure spending of $156 billion accounting for 55% of the total. IDC's same-period tally of infrastructure investment was $231.5 billion, up 35.7% YoY.

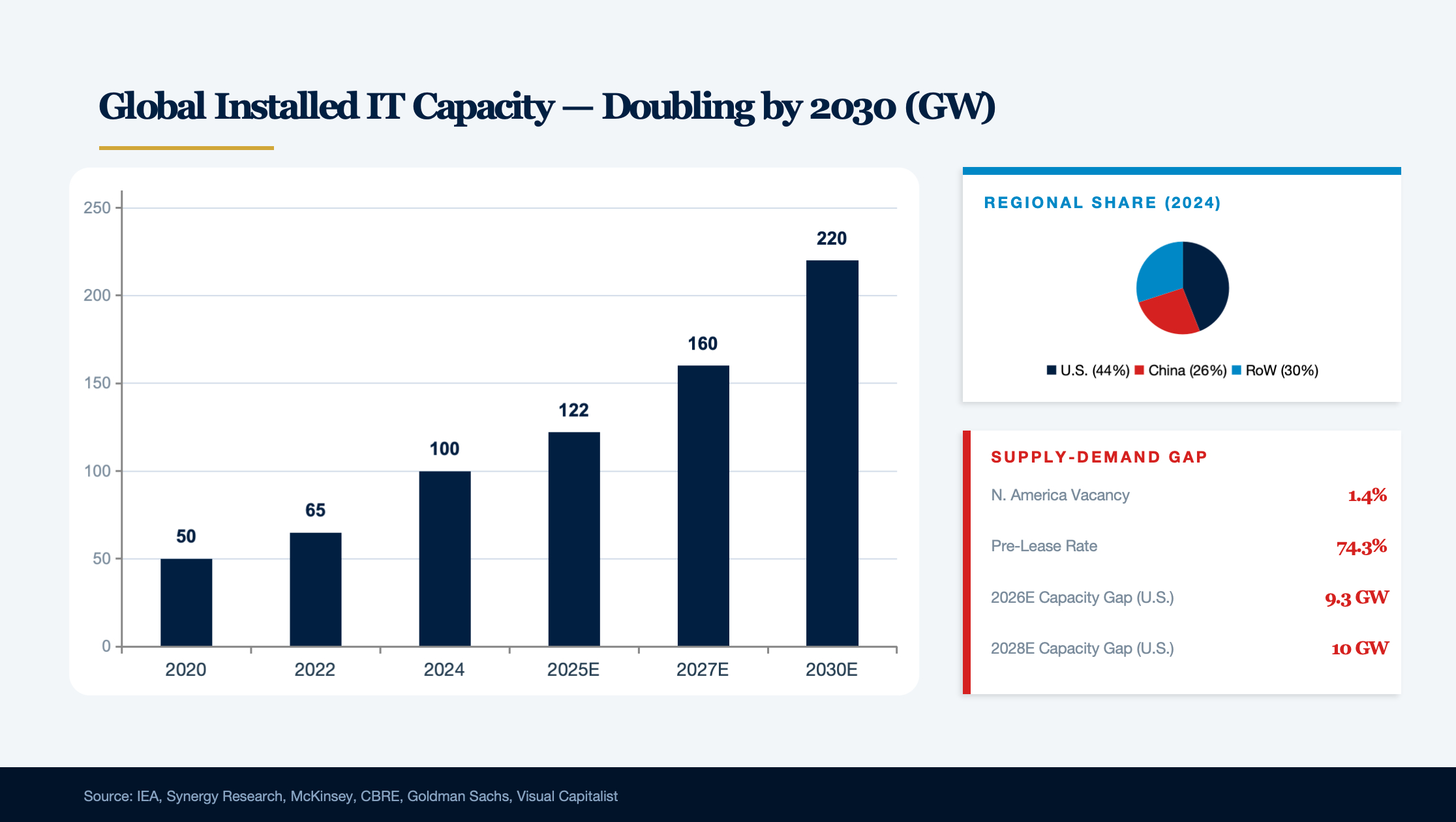

Global Installed Capacity Is Doubling

Total installed IT power capacity is climbing rapidly. Aggregating multiple data sources:

- IEA: 2024 global installed capacity approaching 100 GW

- Synergy Research: Q1 2025 reaching 122.2 GW

- Knight Frank: 2024 live IT capacity of 45,676 MW, projected to reach 66,504 MW by 2026 (a 45% increase)

- Mordor Intelligence: approximately 119 GW in 2025, projected at 240 GW by 2030, CAGR 15.08%

- McKinsey: global demand projected at ~220 GW by 2030

Note the methodological differences between IEA and Synergy — IEA's 100 GW is closer to facility-level total power consumption, while industry trackers typically focus on IT load capacity. Cushman & Wakefield tracks 97 global markets, with end-2024 third-party operated capacity exceeding 40 GW. By regional breakdown, U.S. installed capacity stands at 53.7 GW (44% of global), China at approximately 32 GW (26%), with the two countries combined representing 70% of the global total (IEA 2024 data).

Supply-Demand Gap at Critical Levels

The severity of the supply-demand imbalance is unprecedented. North American core market vacancy is just 1.4% (CBRE H2 2025), with 74.3% of under-construction capacity already pre-leased. JLL reports that North American vacancy has held at approximately 1% for two consecutive years, with 60% of 35 GW under construction fully leased. Goldman Sachs projects global occupancy will rise from approximately 85% in 2023 to a peak of over 95% by end-2026. Visual Capitalist, citing industry data, notes that the U.S. data center capacity gap is projected to reach 9.3 GW in 2026 and 10 GW in 2028. Key bottlenecks include: power access and grid interconnection delays (2–5 years in many locations), transformer delivery delays (24–40 weeks), tighter permitting, and tight cooling equipment supply chains.

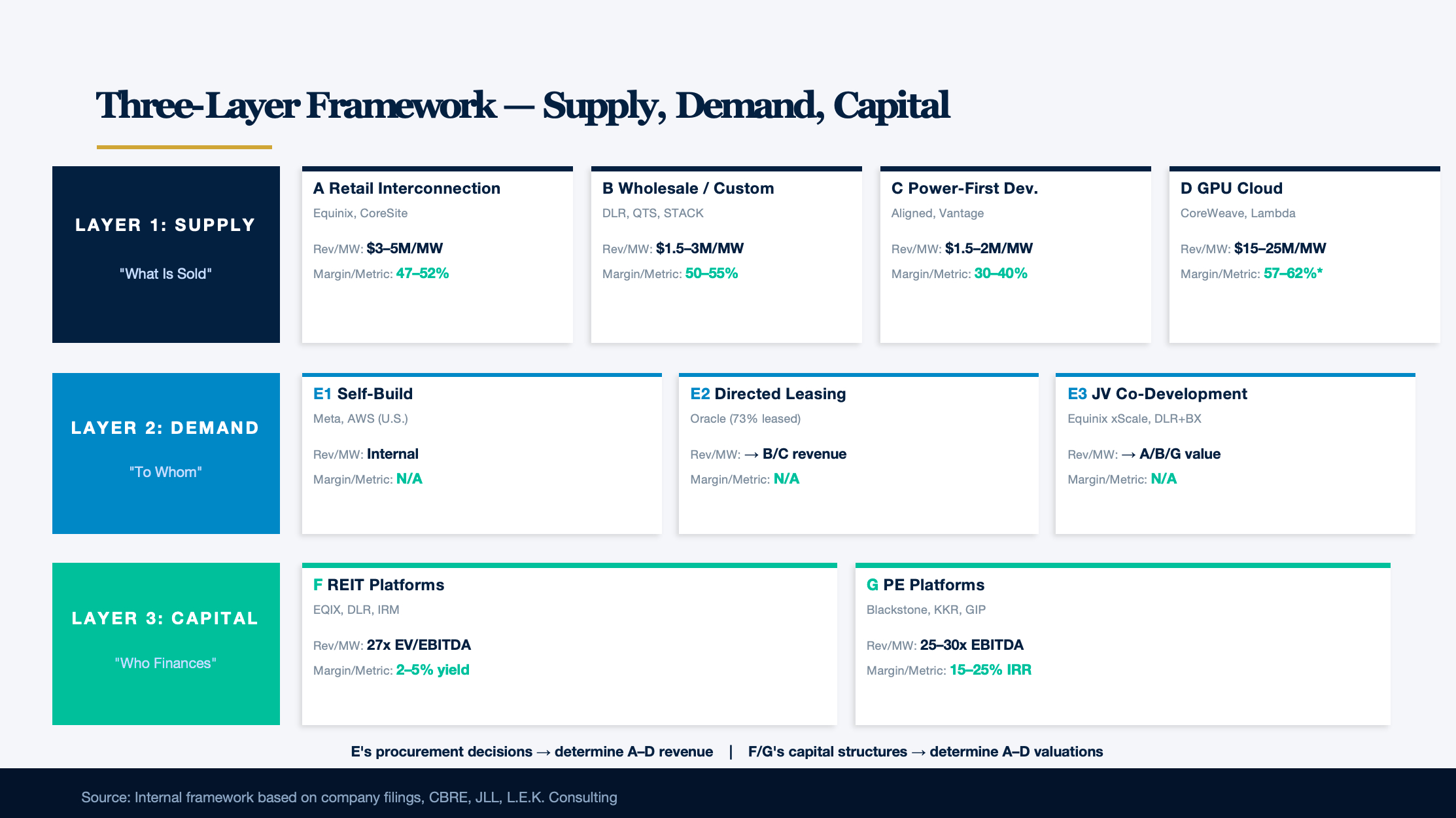

2. Global Competitive Landscape of Leading Operators

Map of the World's Top 20 Operators

Industry concentration continues to rise, with hyperscale operators and private capital dominating the landscape. The following summarizes key metrics for major operators in 2024–2025:

| Rank | Operator | Total Capacity | Data Centers | 2025 Revenue | Geographic Coverage |

|---|---|---|---|---|---|

| 1 | QTS (Blackstone) | >3 GW | 70+ | Undisclosed | North America, UK |

| 2 | Equinix | ~2.1 GW (U.S.) | 251 | $9.22B | 70 metros across 32 countries |

| 3 | Vantage | ~2.6 GW | 24+ (NA) | Undisclosed | North America, EMEA, APAC |

| 4 | Digital Realty | 2,431 MW | 312 | $6.11B | Six continents |

| 5 | Aligned + ODATA | >2.5 GW | 40+ | Undisclosed | North America, LatAm |

| 6 | STT GDC | 2.3 GW design capacity | 100+ | Undisclosed | 12 countries (APAC, Europe) |

| 7 | NTT Global DC | 2,000+ MW | 160+ | ~$1.8B | 20+ countries |

| 8 | CyrusOne (KKR/GIP) | ~1,000 MW | 55+ | Undisclosed | U.S., Europe |

| 9 | CoreWeave | 850 MW (active) | 43 | ~$5.2B (2025E) | U.S., Europe |

| 10 | GDS Holdings | 510,511 sqm in service | 102 | ¥11.29–11.59B (guidance) | China, SE Asia |

Other important operators include: STACK Infrastructure (23+ global markets, with major projects including a 220 MW Malaysia campus and 200 MW Virginia facility); EdgeConneX (350 MW in Japan, AI data center partnership with Lambda); Iron Mountain (18 U.S. data centers, 233 MW, with rapid data center revenue growth); CloudHQ (7 U.S. data centers, 260 MW, with the Ashburn, VA campus reaching 1.7 GW at full build-out); Switch (5 major campuses, 500+ MW potential capacity); VNET Group (452 MW under construction, Microsoft Azure's China partner); Colt DCS (£2.5 billion London expansion plan); Africa Data Centres (Africa's largest independent operator); and ODATA (Latin America's leading hyperscale operator, with a $3.3 billion project in Querétaro).

Chapter II: Global Data Center Trends Driven by AI Compute Demand

AI is reshaping every dimension of the global data center industry at unprecedented speed and scale — from chip to rack, from grid to capital structure. The 2024 global AI server market crossed $125 billion (IDC basis), and combined 2025 capex from the five largest hyperscalers is approaching $400 billion, with roughly 75% flowing to AI infrastructure. The IEA forecasts global data center electricity consumption will double from 415 TWh in 2024 to 945 TWh by 2030, with most of the increment driven by AI. Concurrently, rack-level power density has surged from the traditional 5–10 kW to over 120 kW; GW-scale campuses are moving from blueprint to reality; and non-traditional power solutions such as nuclear and on-site gas generation are being deployed at pace. The depth, breadth, and speed of this transformation are rewriting the rules of the infrastructure industry.

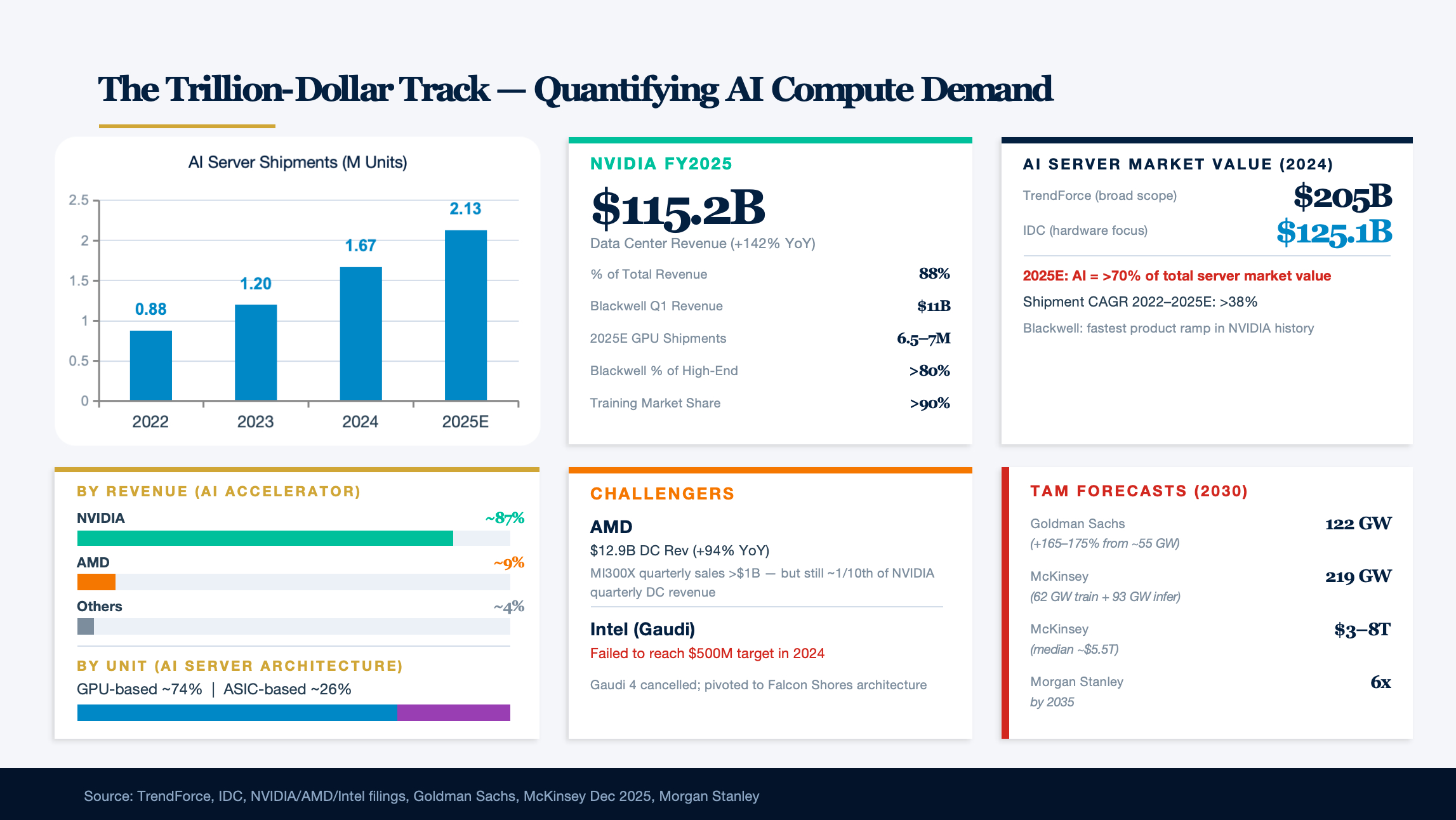

1. The Trillion-Dollar Track: Quantifying AI Compute Demand

Global AI server shipments grew from approximately 880,000 units in 2022 to 1.67 million units in 2024 (TrendForce), a CAGR exceeding 38%. By market value, TrendForce pegs the 2024 AI server industry at approximately $205 billion, while IDC's narrower hardware-focused count is $125.1 billion — both showing explosive growth. TrendForce projects 2025 AI server shipments will reach 2.13 million units, representing over 70% of total server market value.

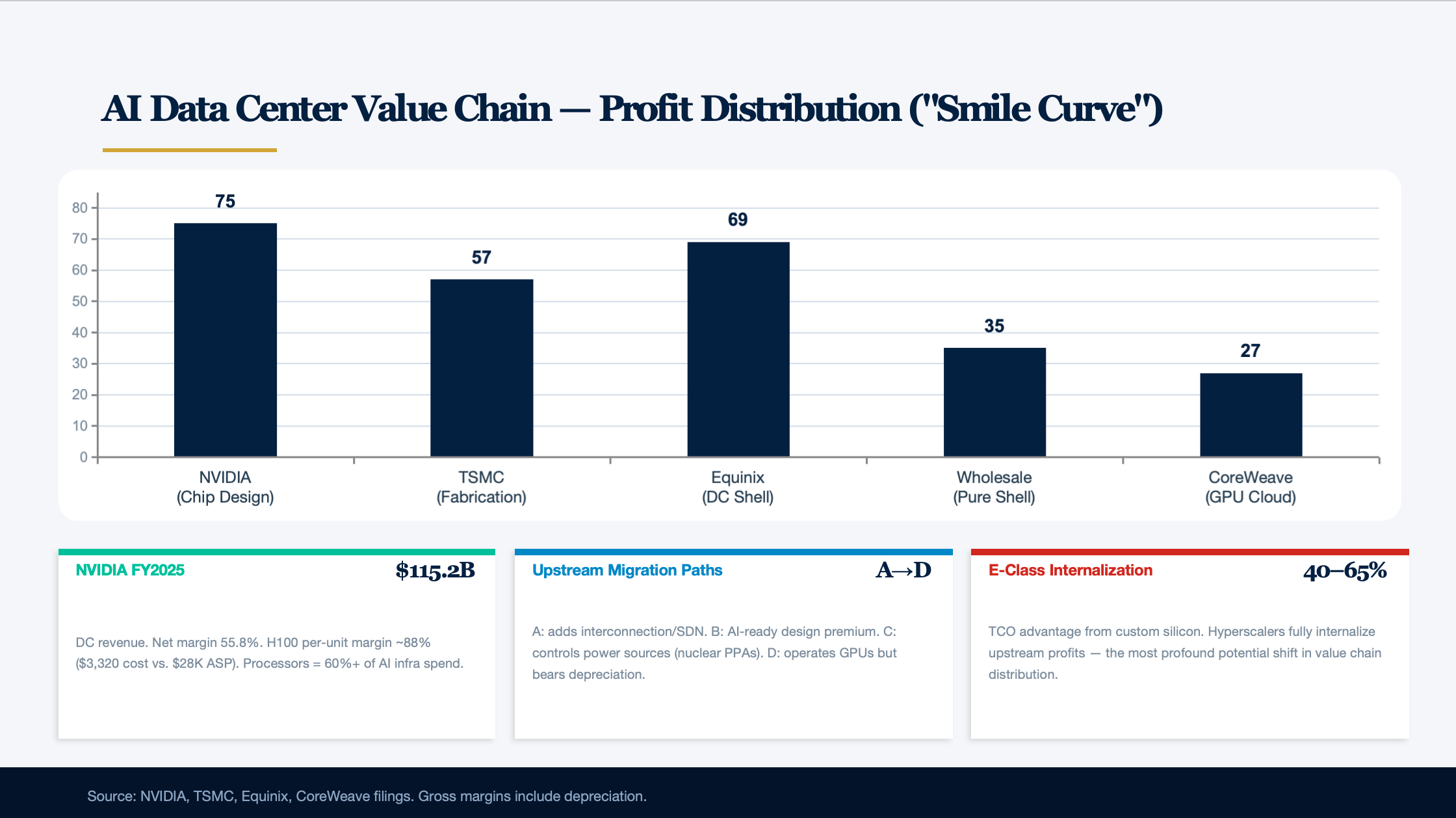

NVIDIA holds absolute dominance in this arms race. Its FY2025 (ended January 2025) data center revenue reached $115.2 billion, up 142% YoY and accounting for 88% of total company revenue. Blackwell-architecture GPUs contributed $11 billion in revenue in their first full shipment quarter — the fastest ramp of any product line in NVIDIA's history. By revenue, NVIDIA commands approximately 87% of the AI accelerator market and over 90% in training. In 2025, NVIDIA is expected to ship 6.5–7 million GPUs, with Blackwell accounting for over 80% of high-end GPU shipments.

AMD, as the only competitor with meaningful traction, recorded approximately $12.9 billion in 2024 data center revenue (+94% YoY), with MI300X quarterly sales crossing $1 billion — but this still represents only one-tenth of NVIDIA's quarterly data center revenue. Intel's Gaudi line suffered a major setback: 2024 failed to reach the $500 million revenue target, Gaudi 4 was cancelled, and the roadmap pivoted to the Falcon Shores architecture. Proprietary ASICs such as Google TPU and AWS Trainium are gaining ground, with ASIC AI servers rising to approximately 26% share in 2024 — though they have not yet disrupted NVIDIA's dominance in the near term.

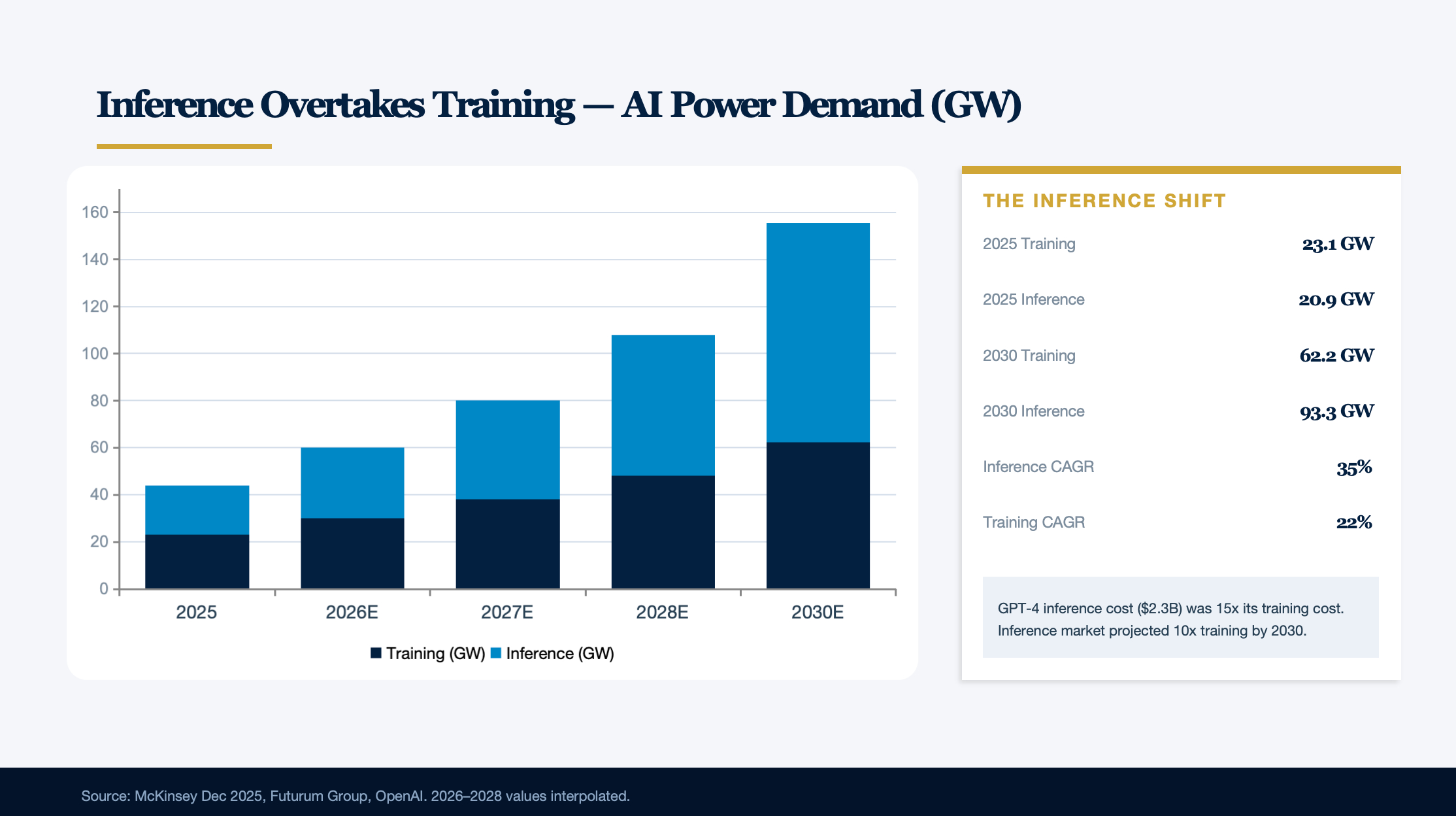

Forecasts for the global AI data center TAM are converging in direction but diverge significantly in methodology. Goldman Sachs projects global data center power demand will grow from approximately 55 GW today to 122 GW by 2030, an increase of 165–175%. McKinsey's December 2025 forecast is more aggressive: 2030 global data center power demand will reach 219 GW, consisting of 62.2 GW for AI training and 93.3 GW for AI inference. By investment scale, McKinsey estimates cumulative AI data center investment requirements of $3–8 trillion, with a median of approximately $5.5 trillion. Morgan Stanley projects global data center capacity will need to grow 6x by 2035.

Inference Is Overtaking Training as the Dominant Workload

The internal structure of AI compute demand is undergoing a profound shift. McKinsey data shows that in 2025, AI training power demand is approximately 23.1 GW and inference is 20.9 GW — roughly balanced. By 2030, however, inference will surge to 93.3 GW (CAGR 35%), substantially exceeding training at 62.2 GW (CAGR 22%). The Futurum Group projects inference revenue will surpass training by 2026; for reference, GPT-4's 2024 inference expenses of approximately $2.3 billion were already 15x its training cost. The inference market is projected to be 10x the size of the training market by 2030. This structural shift means data centers must simultaneously serve two fundamentally different workload profiles — training requires sustained high power and mega-scale clusters, while inference demands low latency and flexible scaling.

On per-query AI energy consumption, the early "ChatGPT uses 10x the energy of a Google search" narrative now requires correction. EPRI's initial estimate placed ChatGPT at approximately 2.9 Wh per query, but updated data from Epoch AI and Sam Altman in 2025 shows GPT-4o standard queries consume only approximately 0.3 Wh — comparable to the per-query figure Google published for its search service back in 2009. That said, complex queries (long text, file attachments) can consume 2–40 Wh, and reasoning-chain models (such as o1) require several multiples of the compute of standard queries. More importantly, Google Search itself has integrated AI Overview, driving actual energy consumption upward.

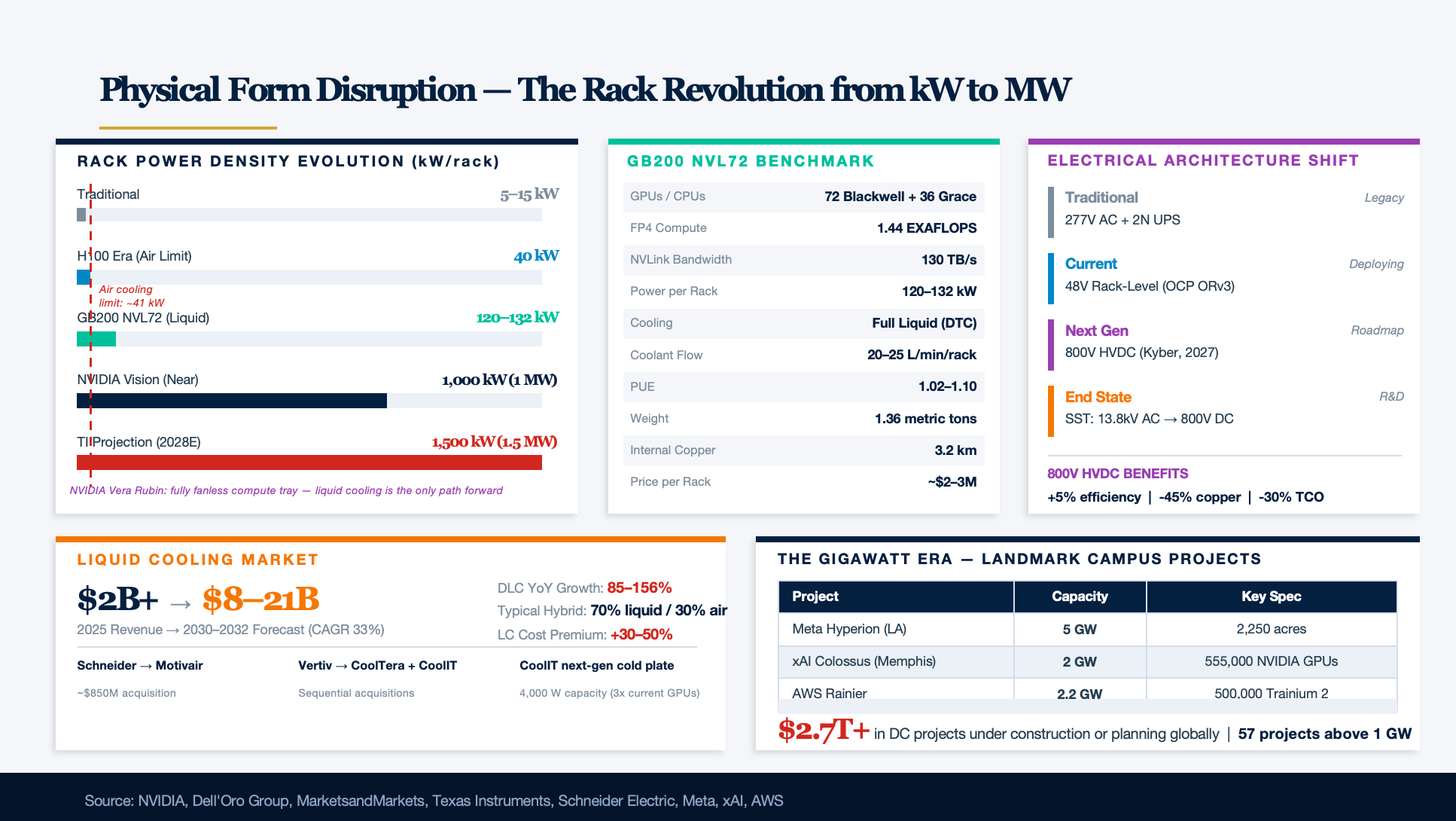

2. Physical Form Disruption: The Rack Revolution from Kilowatts to Megawatts

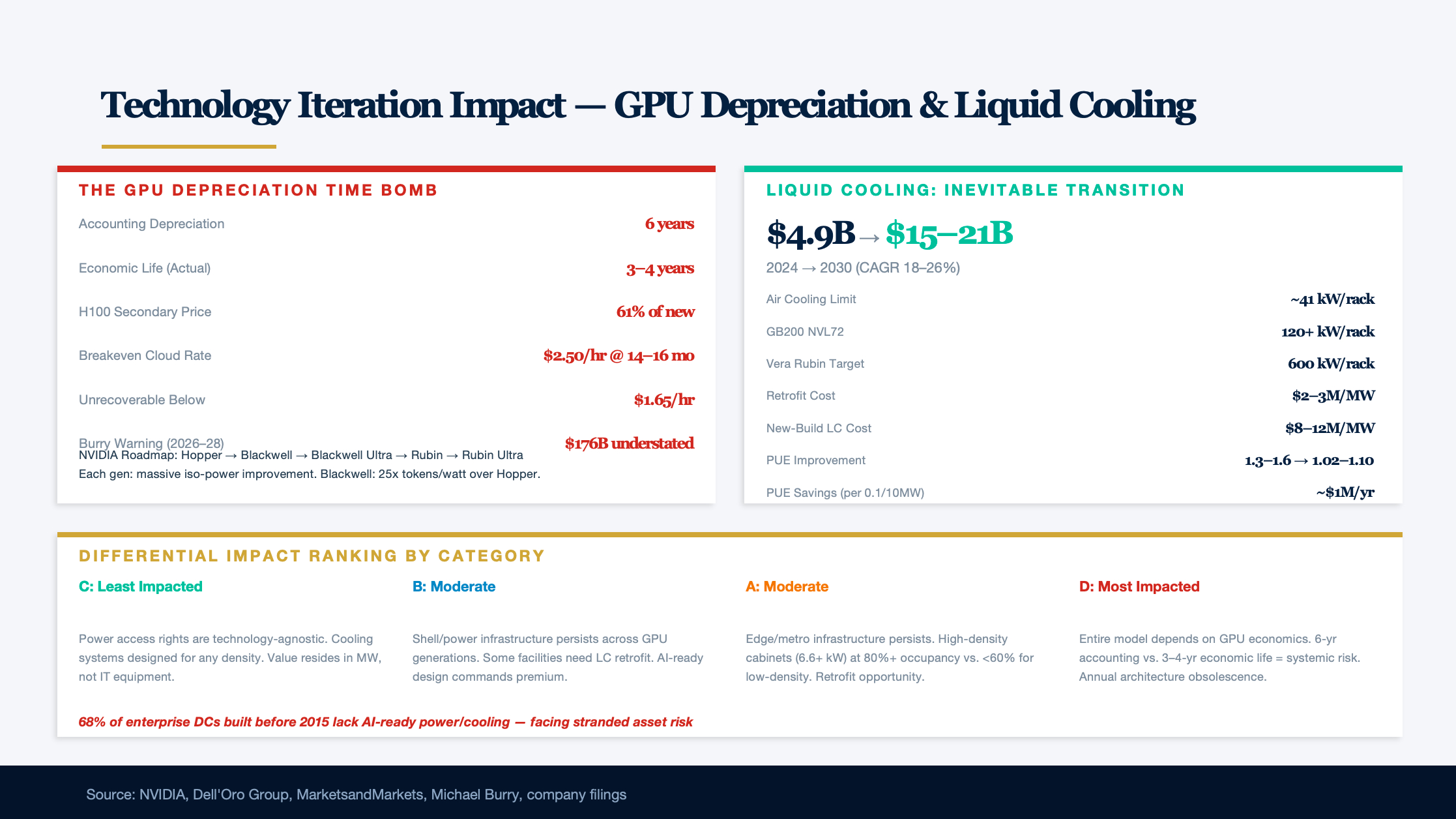

AI's impact on data center physical infrastructure first manifests in the leap in power density. Traditional data center rack power density runs 5–15 kW; H100-era AI training racks reach 40 kW (the air-cooled limit); and NVIDIA Blackwell GB200 NVL72 pushes this figure to 120–132 kW/rack — making liquid cooling a hard prerequisite.

GB200 NVL72 represents the current benchmark for AI infrastructure: 72 Blackwell GPUs paired with 36 Grace CPUs across 36 superchips, forming a single NVLink domain delivering 130 TB/s of interconnect bandwidth and 1.44 EXAFLOPS of FP4 compute. A single rack weighs approximately 1.36 metric tons, contains over 3.2 km of internal copper cabling, and sells for approximately $2–3 million. The system requires full liquid cooling (direct-to-chip cold plate), with coolant flow of approximately 20–25 L/min/rack and inlet temperatures of 25–45°C, driving PUE down to 1.02–1.10.

But this is not the endpoint. NVIDIA has shown the vision of 1 MW-class racks, and in May 2025 released an 800V high-voltage DC (HVDC) power distribution architecture, planned for volume deployment with the Kyber rack system in 2027. The architecture delivers up to 5% end-to-end efficiency improvement, 45% less copper use, and up to 30% lower TCO. Texas Instruments projects that by 2028, a single IT rack will require 1.5 MW of power — 10x current levels.

Liquid Cooling Moves from Optional to Mandatory

The liquid cooling market is experiencing explosive growth. Dell'Oro Group data shows the direct liquid cooling (DLC) market grew 85–156% YoY in 2025, with full-year revenue on track to exceed $2 billion, and projected to surpass $8 billion by 2030. MarketsandMarkets projects the liquid cooling market will grow from $2.84 billion in 2025 to $21.14 billion by 2032, a CAGR of 33.2%.

Key suppliers are aggressively expanding capacity and pursuing acquisitions: Schneider Electric acquired a majority stake in liquid cooling specialist Motivair for approximately $850 million; Vertiv successively acquired CoolTera and CoolIT's joint venture technology; CoolIT unveiled a next-generation cold plate prototype capable of handling approximately 4,000 W — sufficient to cool chips 3x the power of current NVIDIA GPUs. DLC has become the de facto standard for large AI clusters — NVIDIA's next-generation Vera Rubin compute tray has completely eliminated fans, achieving a fully liquid-cooled configuration. Current typical deployments are hybrid 70% liquid / 30% air, with liquid cooling system construction costs 30–50% above traditional air-cooled designs.

The electrical architecture is also undergoing a generational shift. From the traditional 277V AC distribution plus 2N UPS model, the industry is transitioning to 48V rack-level power (OCP ORv3 standard), with the ultimate target being 800V HVDC. NVIDIA's 800V roadmap has gained support from over 20 semiconductor and power equipment companies including ADI, Infineon, Eaton, Schneider, and Vertiv. The end-state solution is solid-state transformers (SSTs) that directly convert 13.8 kV AC to 800V DC, eliminating multi-stage conversion — but commercial deployment is still years away.

Data center campuses have crossed from the "megawatt era" into the "gigawatt era." Meta's Hyperion project in Louisiana targets capacity of up to 5 GW on 2,250 acres; xAI's Memphis Colossus campus has 2 GW operating and under expansion, deploying 555,000 NVIDIA GPUs; AWS's Project Rainier plans 2.2 GW with 500,000 Trainium 2 chips. Globally, data center projects under construction or in planning are valued at over $2.7 trillion, including 57 projects above 1 GW in capacity.

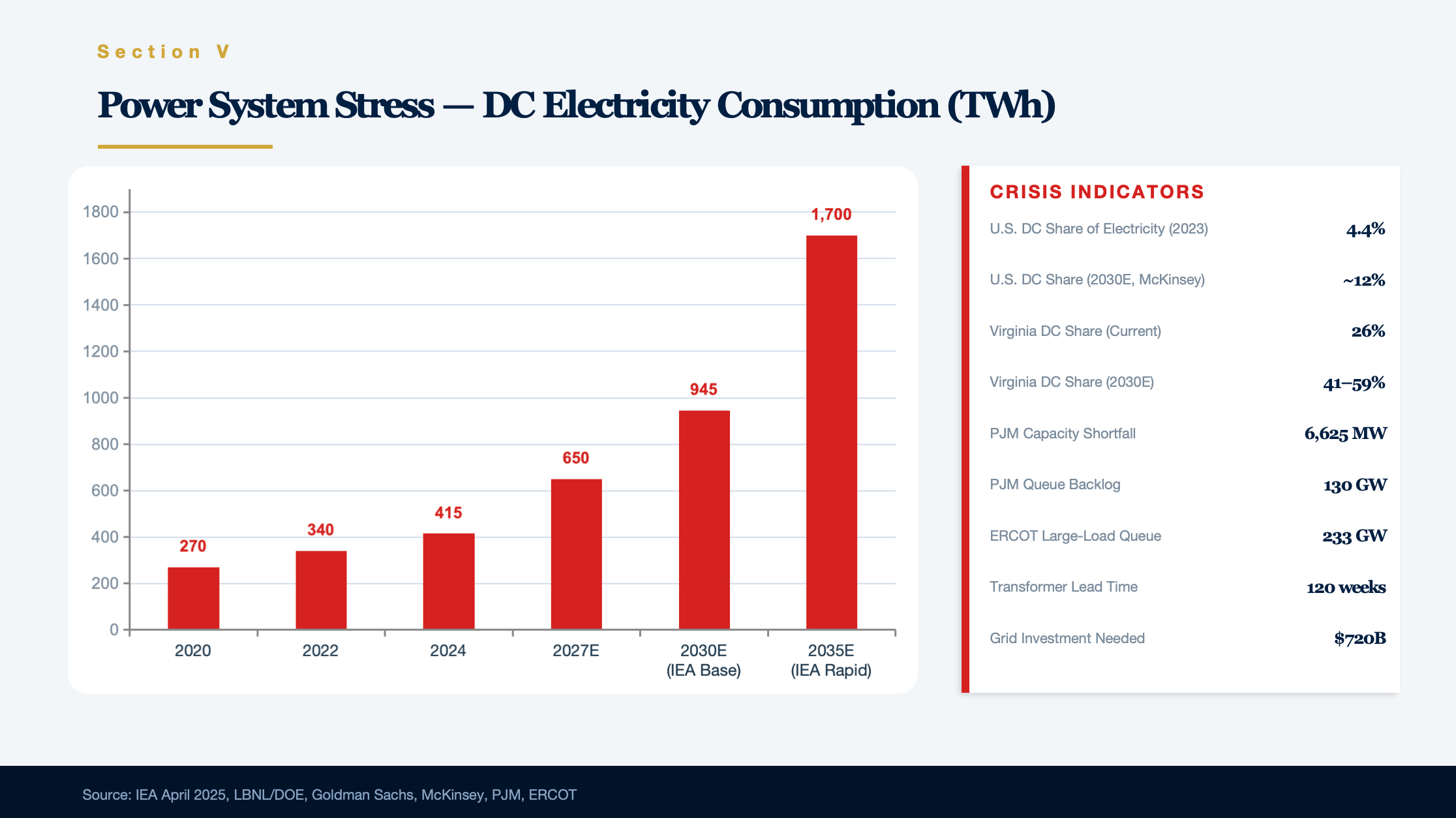

3. Power System Stress Test: From Bottleneck to Crisis

AI data centers' impact on the global power system is shifting from forecast to reality. The IEA's April 2025 Energy and AI report shows global data center electricity consumption grew from approximately 270 TWh in 2020 to 415 TWh in 2024, representing approximately 1.5% of global electricity consumption. Under the baseline scenario, 2030 consumption will reach 945 TWh (~3% of global total), and under the rapid-growth scenario, 2035 could exceed 1,700 TWh. Goldman Sachs' forecast focuses on the power dimension: global data center power demand grows from approximately 55 GW today to 84–92 GW by 2027 and 122 GW by 2030, requiring approximately $720 billion in global grid investment.

The United States is where the pressure is most concentrated. The LBNL/DOE December 2024 report shows 2023 U.S. data center consumption reached 176 TWh, or 4.4% of total U.S. electricity. IEA forecasts 2030 consumption will reach 426 TWh; McKinsey's estimate is higher, projecting U.S. data center share will reach approximately 12%. Virginia's situation is particularly extreme — data centers already account for 26% of state electricity, and EPRI projects this could reach 41–59% by 2030.

PJM Grid Posts Its First Capacity Shortfall; Reliability on the Edge

The PJM Interconnection grid, covering 65 million people across 13 Eastern U.S. states, is under tremendous pressure. Its interconnection queue holds approximately 130 GW of capacity awaiting connection — equivalent to 73% of existing system capacity. More alarmingly, the December 2025 capacity auction posted its first-ever 6,625 MW capacity shortfall, failing to meet reliability targets, with capacity prices surging to a record $333.44/MW-day. PJM peak load is projected to grow 32 GW from 2025–2030, with 30 GW coming from data centers. The organization's scenario analysis shows new data center capacity additions are running at 2x the pace of new generation additions annually, with the cumulative deficit widening and reliability standards potentially being breached from summer 2027.

The Texas ERCOT grid faces similar pressures. As of end-2025, its large-load interconnection queue had surged to over 233 GW, up approximately 300% year-over-year. Data-center-related proposals alone total 156 GW (through 2030), while only approximately 3 GW of large loads were actually approved between June 2024 and June 2025. Interconnection wait times are a system-wide issue — extending from under 2 years in 2000–2007 to approximately 5 years on average today. At end-2023, the national interconnection queue totaled approximately 2.6 TW — more than double existing U.S. installed capacity.

Supply chain bottlenecks for critical power equipment have become a hard constraint on data center construction. Large power transformer delivery times have extended from approximately 50 weeks in 2021 to an average of 120 weeks in 2024, with some transmission-class transformers requiring 3–6 years. Prices have risen 150% since 2020 — 4–6x pre-2022 levels. The U.S. imports 80% of transformer MVA capacity, with severely inadequate domestic production. High-voltage circuit breakers have delivery times of approximately 151 weeks (nearly 3 years), switchgear is in severe shortage, and gas turbines require 5–7 years. The core bottlenecks are shortages of grain-oriented electrical steel (GOES) and copper, and insufficient manufacturing capacity.

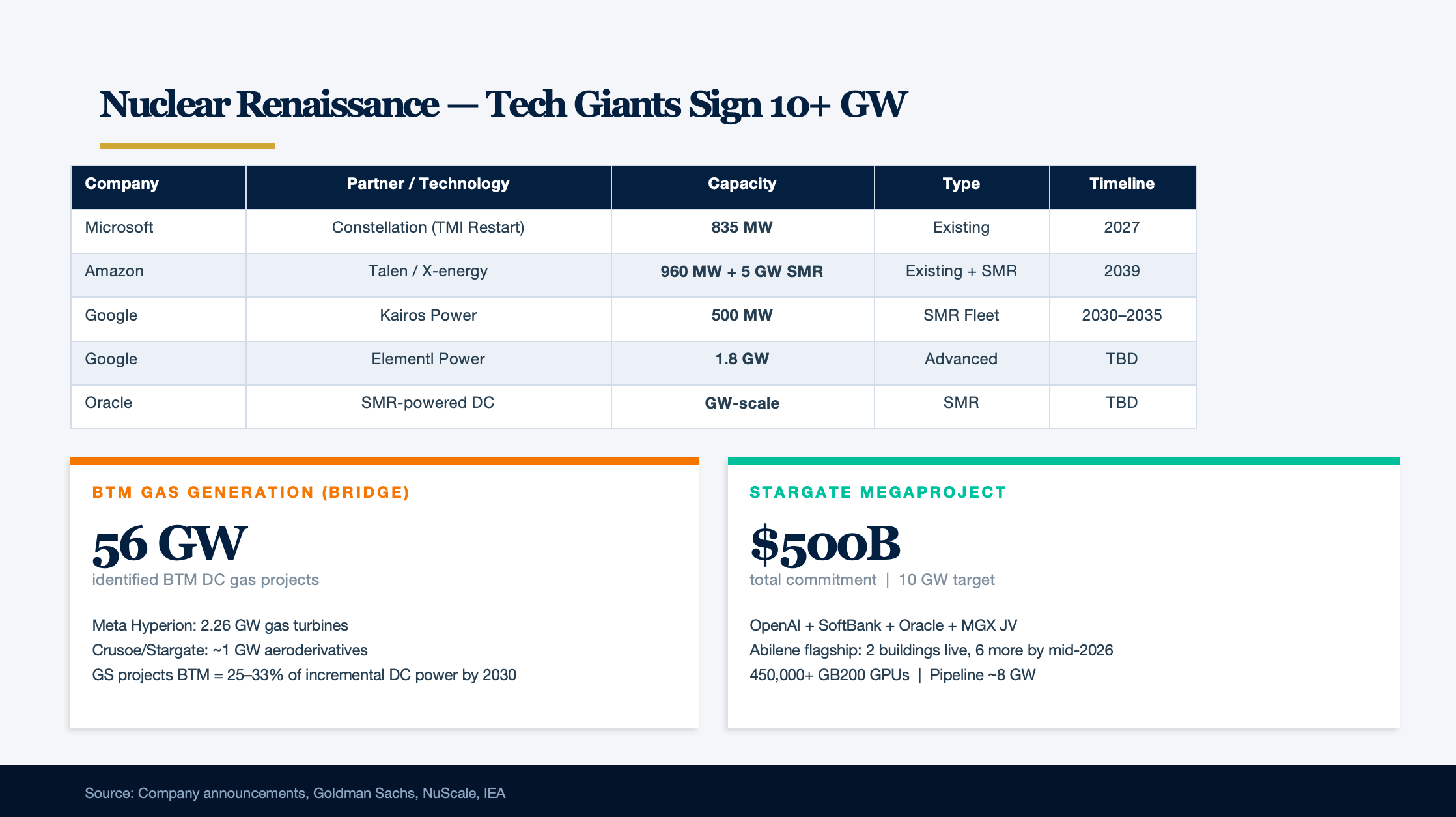

Nuclear Renaissance: Tech Giants Sign for 10+ GW of New Capacity

Facing power bottlenecks, tech giants are embracing nuclear energy with unprecedented intensity. Microsoft signed a 20-year agreement with Constellation Energy, investing $1.6 billion to restart the 835 MW Three Mile Island plant, targeting resumption in 2027. Amazon, through investments in X-energy and a 17-year PPA with Talen Energy, has locked in significant nuclear capacity including 960 MW from the Susquehanna plant, with a goal of deploying 5 GW of SMRs by 2039. Google signed the U.S.'s first corporate SMR fleet contract with Kairos Power for 500 MW to be delivered 2030–2035, and is partnering with Elementl Power to develop 1.8 GW of advanced nuclear. Oracle plans to build a GW-scale data center powered by three SMRs. NuScale's 462 MW US 460 design received Standard Design Approval from the NRC in May 2025, becoming the only NRC-certified SMR technology. Major tech companies have now collectively signed for over 10 GW of new nuclear capacity.

But nuclear timelines are long, making on-site natural gas generation a short-term bridge. Identified behind-the-meter data center gas generation projects total 56 GW. Meta's Hyperion project includes 2.26 GW of H-class gas turbines; Crusoe has deployed approximately 1 GW of aeroderivative turbines for Stargate in Abilene; global natural gas generation under construction exceeds 1,000 GW, including over 250 GW of new U.S. additions. Goldman Sachs projects BTM generation will meet 25–33% of incremental data center demand by 2030, with fuel cell capacity reaching 8–20 GW. Fuel cell suppliers such as Bloom Energy, with deployment cycles of under a year and higher efficiency, are becoming important complements to gas turbines.

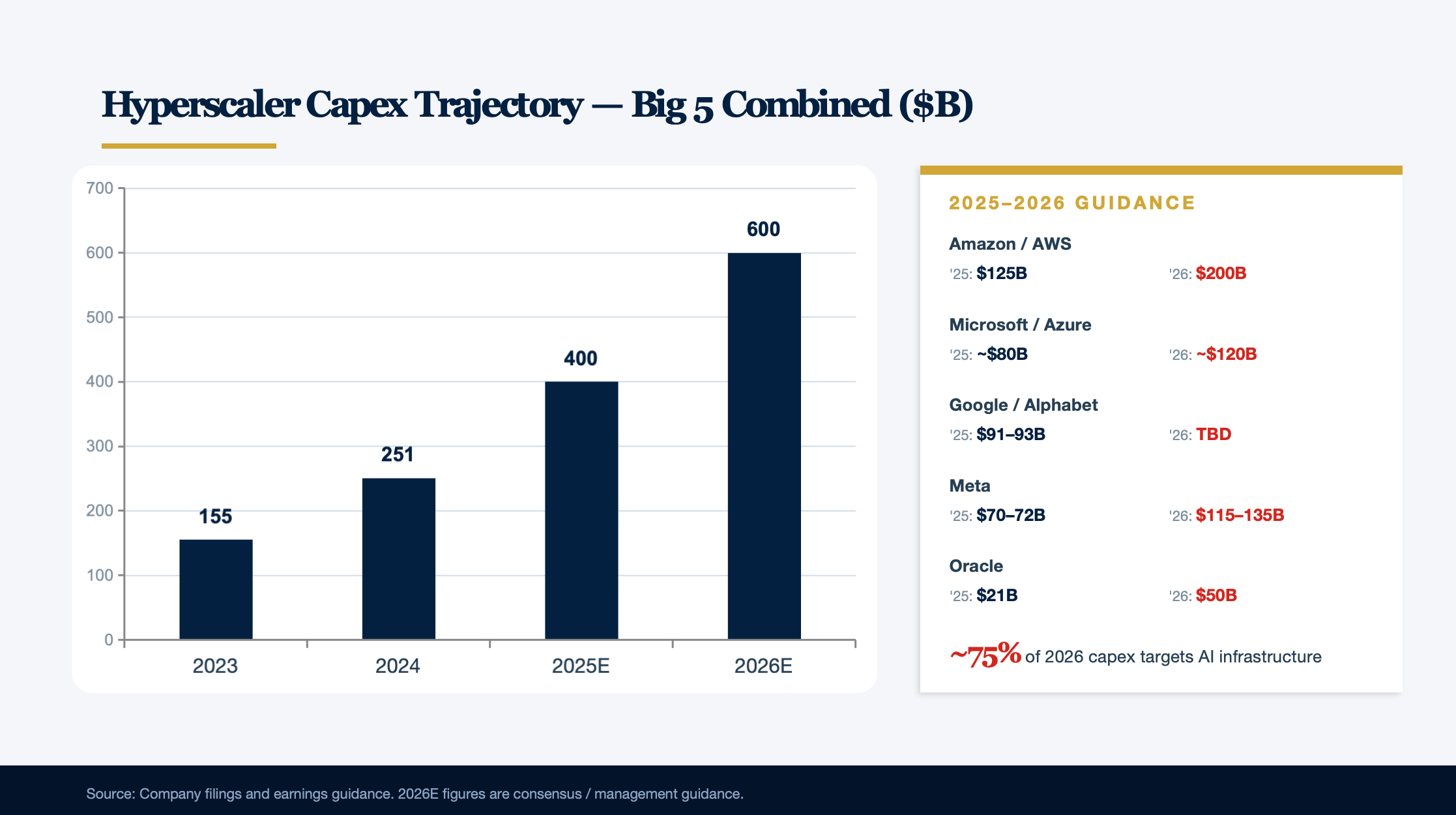

4. The Hyperscaler Arms Race: A $400 Billion Annual Bet

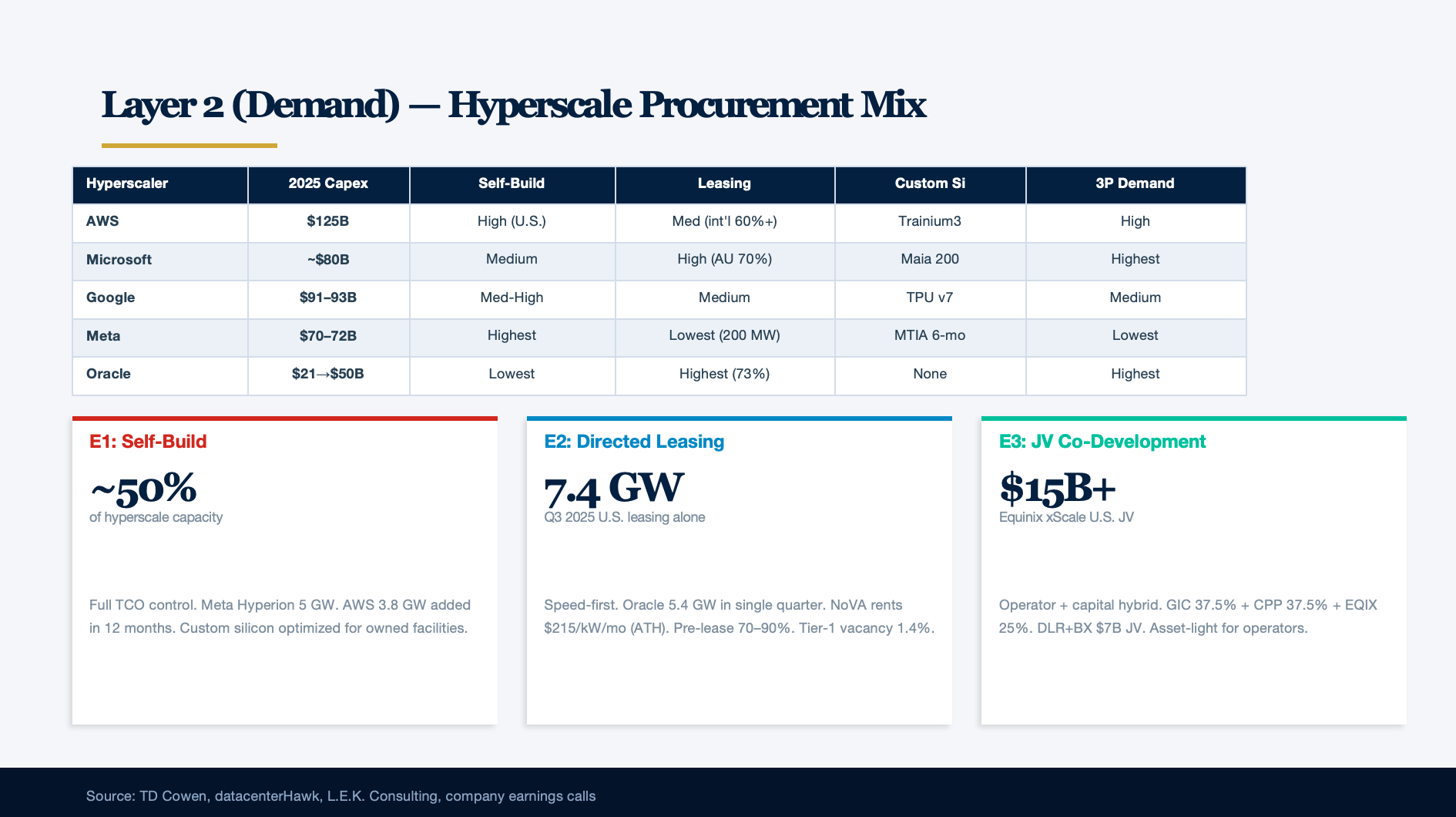

The five hyperscaler AI infrastructure race has reached white-hot intensity. In 2024, Amazon, Microsoft, Google, and Meta combined capex was approximately $251 billion, up 62% YoY. The 2025 figure is projected to approach $400 billion, and 2026 could exceed $600 billion.

Amazon/AWS leads with the most aggressive posture. 2024 capex was approximately $77 billion; 2025 guidance is approximately $125 billion; and Andy Jassy has confirmed 2026 will reach $200 billion — the vast majority directed toward AI infrastructure. AWS has deployed 1.4 million of its own Trainium 2 chips, all sold out; Trainium 3 will roll out in 2026 with ~40% performance improvement; Trainium 4 is expected in 2027 with FP4 performance 6x that of Trainium 3. Combined annualized revenue from the Trainium and Graviton lines has exceeded $10 billion.

Microsoft/Azure FY2025 (ended June 2025) capex was approximately $80 billion, with FY2026 projected at approximately $120 billion. Its in-house Azure Maia 100 chip, built on TSMC's 5nm process, delivers 1,600 TFLOPS of MXInt8 compute. The second-generation Maia is already in mass deployment, with 40% improvement in performance-per-watt.

Google/Alphabet actual 2024 spending was approximately $52 billion; 2025 guidance has been raised three times to $91–93 billion. TPU v7 (Ironwood) was launched in April 2025, with peak compute of 4,614 TFLOPS and 9,216-chip cluster configurations. An agreement with Anthropic for the use of up to 1 million TPUs is valued in the tens of billions.

Meta was approximately $39 billion in 2024, raised to $70–72 billion in 2025, with 2026 guidance of $115–135 billion (nearly double). Meta has announced a 4-generation MTIA chip roadmap aimed at reducing dependency on NVIDIA. It has purchased over 1.3 million GPUs, with multiple GW-scale campuses under construction globally.

Oracle has emerged as the dark horse "coming from behind." FY2026 capex has been raised from $35 billion to $50 billion, with capex as a share of revenue reaching 57% — the highest among the five hyperscalers. RPO (remaining performance obligations) has surged from $80 billion in FY2024 Q3 to the latest figure of $553 billion.

AI-Native Insurgents and the Stargate Megaproject

CoreWeave is the most closely watched AI-native data center company. It raised approximately $1.5 billion in its March 2025 IPO. 2024 revenue of $1.9 billion (+737% YoY), with a contract backlog of $66.8 billion. Active power is approximately 850 MW, total contracted capacity exceeds 3.1 GW, and it has announced an all-stock ~$9 billion acquisition of Core Scientific to secure 1.3 GW of power resources, targeting 5+ GW by 2030. NVIDIA is a core partner, having signed a $6.3 billion capacity agreement.

Crusoe Energy, with its vertically integrated model (energy → data center → cloud), has risen rapidly, with a latest valuation exceeding $10 billion and a power pipeline exceeding 45 GW. Lambda Labs is valued at approximately $4 billion and is deploying Blackwell B200s, with 25,000+ NVIDIA GPUs. Applied Digital has contracted for 600 MW and approximately $16 billion in expected lease revenue.

The Stargate project is the most grandiose undertaking in this race. A joint venture among OpenAI, SoftBank, Oracle, and MGX, announced at the White House in January 2025, with total investment commitments of $500 billion and a 10 GW capacity target. As of early 2026, the Abilene flagship site has 2 buildings operational and 6 more expected to complete by mid-2026, deploying over 450,000 GB200 GPUs. Through a series of bilateral agreements, the total project pipeline approaches 8 GW. However, the joint venture entity's governance and execution mechanism remain disputed — actual construction is largely being advanced through bilateral Oracle-OpenAI and SoftBank-OpenAI agreements.

5. Undercurrents Beneath the Boom: Uncertainties and Risks

Jevons Paradox Is Operating Strongly — But Not Without Ceilings

AI chip efficiency gains are stunning — B200 inference efficiency is 8–15x that of H100, though power draw has risen from 700 W to 1000 W. Epoch AI data shows AI inference costs have dropped approximately 92% since early 2023 — but demand is growing faster. Microsoft CEO Satya Nadella, Meta CEO Mark Zuckerberg, and Anthropic founder Dario Amodei have all stated explicitly that efficiency gains will not reduce spending but will instead accelerate investment. DeepSeek V3's training cost on the surface was only approximately $5.6 million (versus over $100 million for GPT-4), but this stunning efficiency did not dampen hyperscaler spending intent — Meta raised its 2025 AI spending guidance to $60–65 billion within days of DeepSeek's release.

That said, some researchers have noted the limits of Jevons' applicability. LED lighting efficiency improvements did not lead to runaway energy consumption, and the AI market may face application-layer saturation. Short-term (2025–2027) demand growth almost certainly overwhelms efficiency gains, but the long-term trajectory depends on whether AI application end-value can continue to expand.

GPU Utilization and Overbuild Risk

Average GPU utilization is only 60–70%, with 30–40% of capacity sitting idle. In training deployments, GPUs wait for data 30–50% of the time, and data preprocessing consumes up to 65% of training cycles. 70% utilization implies effective costs are 43% above nameplate. MIG, dynamic batching, GPU pooling, and similar techniques can push utilization to 90–95%, but significant optimization headroom remains in actual deployments.

Sequoia Capital's "$600 billion question" highlighted the massive gap between AI infrastructure investment and actual revenue — only "low single-digit to low double-digit percentages" of enterprises have achieved sustainable ROI from generative AI. The late-1990s fiber optic bubble offers a historical warning: over $500 billion in investment, 85% of fiber unused for years, but ultimately birthing Netflix and Facebook. KKR argues that the current cycle differs critically from the fiber bubble — long-term contracts provide support, and the hard constraint of power makes unconstrained overbuild impossible.

The Model Efficiency Revolution Is Reshaping Demand Structure

The shift from dense Transformers to sparse MoE is the most profound technical variable. Since early 2025, over 60% of frontier models have adopted MoE architectures — DeepSeek-V3 achieves performance comparable to dense models using 671B total parameters but only 37B activated. Quantization has become standardized as "16-bit training, 4-bit deployment"; FP32 → INT4 quantization shrinks model size 8x. Microsoft's Phi-4-reasoning (14B parameters) achieves reasoning task performance approaching full DeepSeek-R1 (671B parameters) — meaning compute and memory requirements for equivalent performance are declining rapidly.

The small-model + edge-inference trend suggests a possible hybrid architecture: 90–95% of queries handled by on-device small models, with only 5–10% requiring cloud-based large models. Over 2 billion smartphones can now run local SLMs. If this trend accelerates, it could materially alter the demand growth trajectory for cloud-based AI compute.

6. Summary

This AI-driven data center transformation carries three high-conviction characteristics: power will replace land as the scarcest resource (120-week transformer lead times, PJM's 6.6 GW capacity shortfall); liquid cooling and HVDC distribution will become standard for new builds within 3–5 years (DLC penetration is moving from single digits to majority); and inference will overtake training as the dominant workload between 2026–2028 (changing data center geographic distribution and design paradigms).

The greatest uncertainty lies in whether demand growth can keep pace with investment growth. The top five hyperscalers' combined 2026 capex of $600 billion means they are channeling 94% of operating cash flow into AI build-out — an unprecedented collective bet. MoE architectures and inference optimization are driving unit compute costs down by factors of tens per year, and Jevons' paradox is strongly active in the short term — but whether AI application-layer end revenue can match the pace of infrastructure investment remains the key variable determining whether this supercycle is "rational build-out" or "a new fiber bubble." The physical constraint of power may be the most effective "circuit breaker" preventing overbuild — even with unlimited capital, transformer delivery cycles and grid interconnection capacity set a hard speed limit on this race.

Chapter III: The New Global Data Center Map in the AI Era

| Market | Operating Capacity | Under Construction | Pipeline | Vacancy | Rent ($/kW/mo) | Power Rate (¢/kWh) |

|---|---|---|---|---|---|---|

| Northern Virginia | 5.6 GW | 2,078 MW | 5.9 GW | 0.5% | $175–225 | 8–10 |

| Dallas–Fort Worth | 1.5 GW | ~606 MW | 3.9 GW | <1% | $200+ | 6–8 |

| Phoenix | 2.4 GW | 1,300 MW | 4.2 GW | 3% | $190 | 7–9 |

| Chicago | 1.9 GW | 1,180 MW | 3+ GW | 1.9% | $155–165 | 6.9 |

| Silicon Valley | ~625 MW | 168 MW | Limited | 5.5% | $155–250 | 12.6–26 |

| Atlanta | 1,000 MW | 2,150 MW | Massive | 0.72% | Relatively stable | 9.94 |

| Montreal | 600+ MW pipeline | Multiple | Large | Tight | — | 2.8–4.2 |

Part I: North America — The Global Compute Engine at Full Stretch

Northern Virginia Still Reigns Supreme, but the Cost of Growth Is Rising

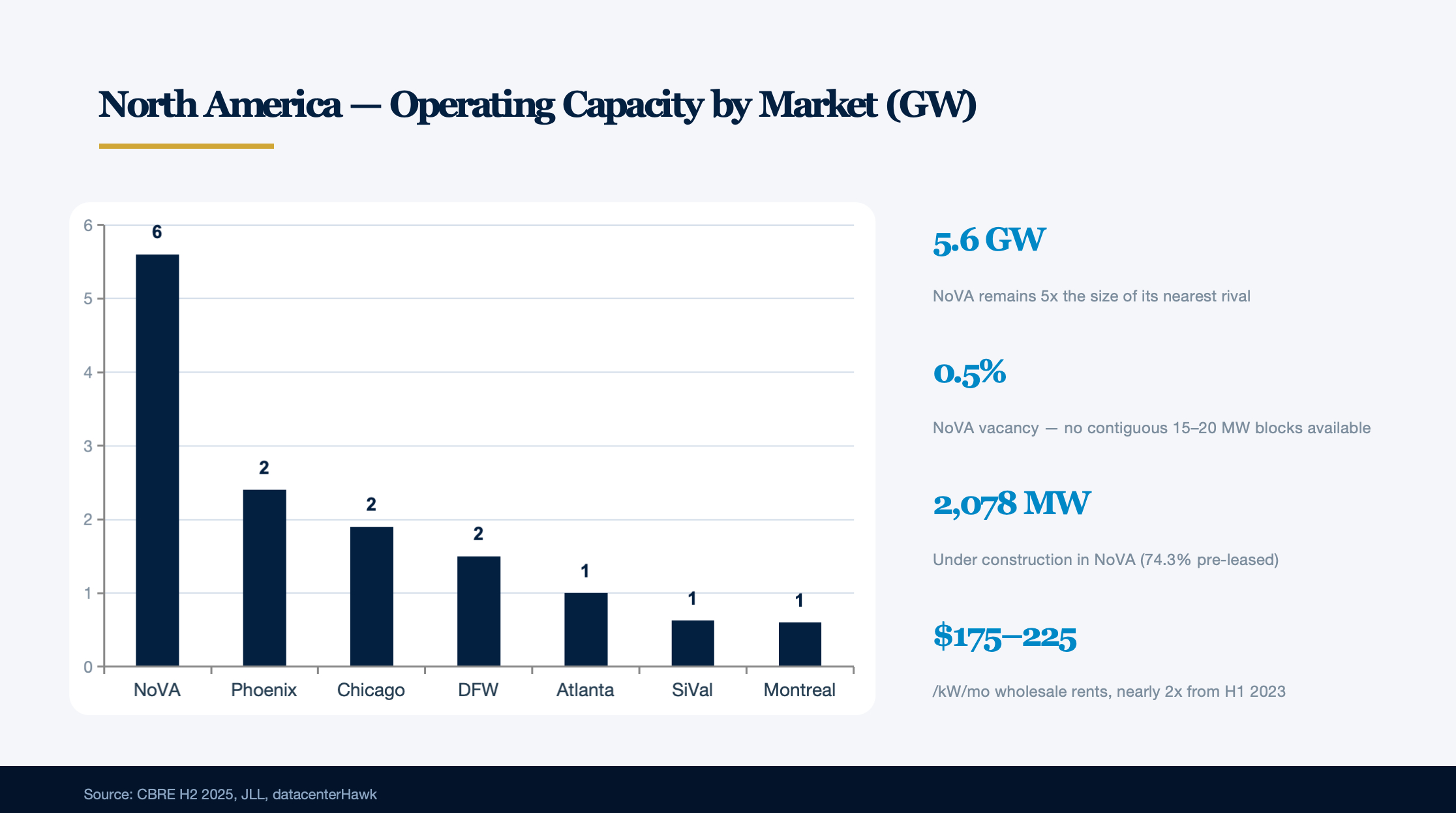

Northern Virginia (NoVA) remains the world's largest data center market at 5.6 GW of total capacity — five times the size of its nearest rival. Net absorption in 2025 reached 1,102 MW, leading all major markets. Yet this "Data Center Capital" faces unprecedented pressure.

Supply-demand at breaking point. CBRE data shows colocation vacancy fell to just 0.5% in H2 2025, with no contiguous blocks of 15–20 MW available anywhere in the market. Under-construction capacity stands at 2,078 MW (up 80% YoY), but 74.3% is already pre-leased, with signed power agreements extending through 2026–2028. Wholesale rents have soared to $175–$225/kW/month, nearly doubling from the $90–$110 range seen in H1 2023. Data center land prices have breached $8 million per acre, compared with $200K–$300K for other land in the same area.

Dominion Energy grid queue hits record levels. As of October 2025, data center-related power applications total 47.1 GW — more than double Dominion's historical peak load of 23 GW. Filings submitted in February 2025 show pending applications with no confirmed interconnection date reaching approximately 70 GW. Individual campus applications have scaled from a typical 30 MW to 300 MW or even multi-GW levels. Dominion projects an 85% load increase over 15 years, requiring 3.4 GW of offshore wind, 12 GW of solar, and 4.5 GW of storage. Data centers already account for 21–24% of Virginia's total electricity sales.

Loudoun County ends by-right approvals. On March 18, 2025, Loudoun County voted 7:2 to amend its zoning rules, shifting data center construction from administrative approval to a Special Exception (SPEX) process — requiring public hearings before the Planning Commission and Board of Supervisors. The change is expected to add 12–24 months to approval timelines. Nonetheless, data centers still contribute roughly half the county's property tax revenue, with FY2025 collections of approximately $895 million, generating $26 in tax revenue for every $1 of public services consumed.

The southern corridor accelerates. Vantage is developing a $2 billion, 929,000 sq ft campus in Stafford County. STACK Infrastructure has planned a 1 GW Stafford Technology Campus spanning 500 acres with 19 buildings and 300 MW of battery storage. CleanArc has broken ground on a 900 MW campus in Caroline County, while PowerHouse is constructing an 800 MW facility in Spotsylvania County. The I-95 corridor is extending southward from NoVA toward Richmond as a new data center belt.

Phoenix, Chicago, DFW, Silicon Valley, and Atlanta Each Carve Distinct Positions

Phoenix boasts a 4.2 GW pipeline — second nationally only to NoVA's 5.9 GW — with 1.3 GW under construction, the most of any market outside NoVA. Vacancy stands at 3% and rents at approximately $190/kW/month. Yet water constraints are intensifying: the Bureau of Reclamation cut Arizona's Colorado River allocation to 512,000 acre-feet/year in August 2024, amid the region's driest period in 1,200 years. Data centers consume 500,000 to 5 million gallons of water daily. The industry is accelerating adoption of waterless cooling. The largest planned development is the Vermaland campus in Pinal County: 3,300 acres, up to 3 GW, and a $33 billion investment.

Chicago operates 1.9 GW with 1.18 GW under construction and a record-low vacancy of 1.9%. ComEd's grid faces immense pressure: 75+ large load applications total over 28 GW (exceeding ComEd's historical peak of 24 GW), including 7 projects requesting 1 GW each. Power delivery is delayed to 2032 or later. Illinois industrial electricity at approximately 6.9¢/kWh remains competitive among major markets.

DFW has grown to 1.5 GW of total capacity. JLL projects the market will double by end of 2026. Net absorption in 2025 reached 470.8 MW (up 424 MW YoY), while vacancy dropped below 1%.

Vantage Frontier is the market's marquee development — announced in August 2025, located in Shackelford County, roughly 125 miles west of Fort Worth. Total investment exceeds $25 billion, with 1.4 GW of capacity across 1,200 acres, 10 data centers, and 3.7 million sq ft, supporting 250+ kW ultra-high-density racks with liquid cooling. The first building is expected to deliver in H2 2026, linked to the Oracle/OpenAI Stargate project. Other major DFW projects include Crusoe and Blue Owl's $15 billion / 1.2 GW AI campus in Abilene, and Compass Red Oak's 350 MW development.

ERCOT grid — advantages and challenges. Oncor interconnection timelines of approximately 18 months are far faster than NoVA's 36 months or Silicon Valley's 5+ years. However, ERCOT interconnection applications have surged from 41 GW in early 2024 to 226 GW by November 2025, with roughly 73% attributable to data centers. Texas Senate Bill 6 requires new large loads to meet performance obligations during emergencies, with developers paying a $100K initial study fee.

Silicon Valley / San Jose is the highest-rent data center market in the U.S. ($155–$250/kW/month), with power delivery expected to take 5+ years — the longest of any major market. PG&E has virtually no additional megawatt-scale capacity available in Santa Clara or San Jose. Land prices approach $4.4 million/acre, forcing developers into 3–4-story vertical builds. But its interconnection density remains irreplaceable — Equinix's Great Oaks campus is a critical cloud connectivity hub hosting AWS Direct Connect, Azure ExpressRoute, and Google Cloud Interconnect.

Atlanta was 2024's biggest breakout market — net absorption of 705.8 MW was 39 times the 2023 figure, surpassing NoVA for the first time. Total inventory grew 222% to 1,000.4 MW, with over 2,150 MW under construction. Georgia Power received regulatory approval for approximately 10 GW of new generation capacity ($16.3 billion investment), with 80% earmarked for data centers. AWS is investing $11 billion in Georgia, and QTS is planning a 615-acre campus in Fayetteville. Georgia offers a 100% sales tax exemption on server equipment investments exceeding $15 million. However, political winds are shifting — Clayton County has imposed a construction moratorium, and state legislators considered curtailing data center tax incentives in March 2026.

Secondary Markets Explode: Ohio, Mississippi, Indiana, Reno

Ohio is rising on the back of AEP's power infrastructure and its central geographic position. AEP Ohio's queue includes 50+ customers requesting over 30,000 MW. The largest project is SoftBank's Pike County $33 billion development (10 GW data center + 10 GW power plant). Amazon has invested over $11.3 billion in Ohio. AEP plans $72 billion in grid upgrades from 2026–2030.

Mississippi has attracted approximately $29 billion in investment — including AWS's $10 billion Madison County campus (1,713 acres, 16 buildings), Compass's $10 billion Meridian campus, and xAI's 1.2 GW Southaven project. The state offers 10-year/100% corporate income tax exemptions, sales tax incentives, and 30-year rolling abatements.

Indiana has secured over $31 billion in Amazon investment alone, including the $11 billion Project Rainier in New Carlisle (2.4 GW, 1,100 new jobs). Meta is investing $10 billion in a 1 GW campus in Lebanon. Indiana offers 35-year sales tax exemptions with a starting threshold of just $10 million — among the lowest in the nation.

Reno hosts Switch's Citadel campus (2,000 acres, 7.2M sq ft, 650 MW) alongside major projects from Apple, Google, and Vantage. Notably, Reno's construction cost of $15M/MW is the highest in the country, driven primarily by labor scarcity requiring workers to be imported from other regions.

Canada: Hydroelectric Advantage Powers Montreal's Rise

Canada's total IT capacity now exceeds 10 GW (including operational, under construction, committed, and early-stage). Three hubs — Toronto, Montreal, and Alberta — account for 93% of national IT load.

Montreal has emerged as an AI data center hotspot, leveraging Québec's hydroelectric advantage with industrial power rates locked at CAD 0.036–0.054/kWh (~$0.028–$0.042/kWh) — the lowest in North America. Operating costs run 40% below the Canadian national average. Over 600 MW of announced pipeline capacity is in the 2025 queue, with campus designs targeting 70 kW/rack densities for AI workloads.

Toronto holds 370+ MW of power capacity, representing approximately 40% of Canada's total. Alberta's Wonder Valley project (O'Leary Ventures, 5.6 GW) is the largest single development ever announced in Canada.

U.S. Policy Landscape: A Tug-of-War Between Incentives and Resistance

Tax incentive competition. At least 36–42 states have some form of data center tax incentive legislation. 37 states have enacted sales tax exemptions, with 16 states collectively granting nearly $6 billion in abatements over the past five years. Virginia's exemptions have ballooned from an initial $1.5M/year to $1.6 billion/year — a JLARC evaluation rated the program as delivering only "moderate economic benefit" and noted it "does not pay for itself." Texas is expected to exceed $1 billion in subsidies in 2025. A counter-trend is emerging: Virginia, Minnesota, Texas, and Georgia are all reconsidering or attaching conditions to their programs.

Community opposition at record levels. The Data Center Watch project tracked 142 grassroots groups (across 24 states) opposing data centers, growing to 188 groups (40 states) by Q2 2025. A cumulative $18 billion in projects have been directly blocked, and $46 billion delayed — a combined $64 billion. In Q2 2025 alone, $98 billion across 20 projects in 11 states were stalled. Project cancellations surged from 2 in 2023 to 25 in 2025. Core grievances include daily water consumption of 5 million gallons, permanent facilities creating only 15–100 jobs, noise levels reaching 100 decibels, and residential electricity rates rising 11.5% in 2025. Senator Bernie Sanders called for a national construction moratorium in December 2025.

The ADVANCE Act and nuclear energy. Signed in July 2024, the ADVANCE Act streamlines NRC licensing and sets a 25-month review deadline for new reactors at existing nuclear plant sites. A May 2025 executive order targets quadrupling nuclear capacity from 100 GW to 400 GW by 2050. Key nuclear-data center deals include: Talen Energy/Amazon's $18 billion / 1,920 MW / 17-year PPA (Susquehanna); Microsoft/Constellation's $1.6 billion / 835 MW / 20-year PPA (Three Mile Island restart, targeting 2028); and Meta's agreement with TerraPower for 8 Natrium reactors (2.6 GW nuclear + 1.2 GW storage). Google signed the first corporate SMR fleet deal with Kairos Power for 500 MW by 2035, with the first unit online by 2030. However, no SMRs are currently operational in the U.S. — the earliest commercial deployments are expected in the late 2020s or early 2030s.

North American AI-Driven Supply-Demand Dynamics: A Historic Inflection Point

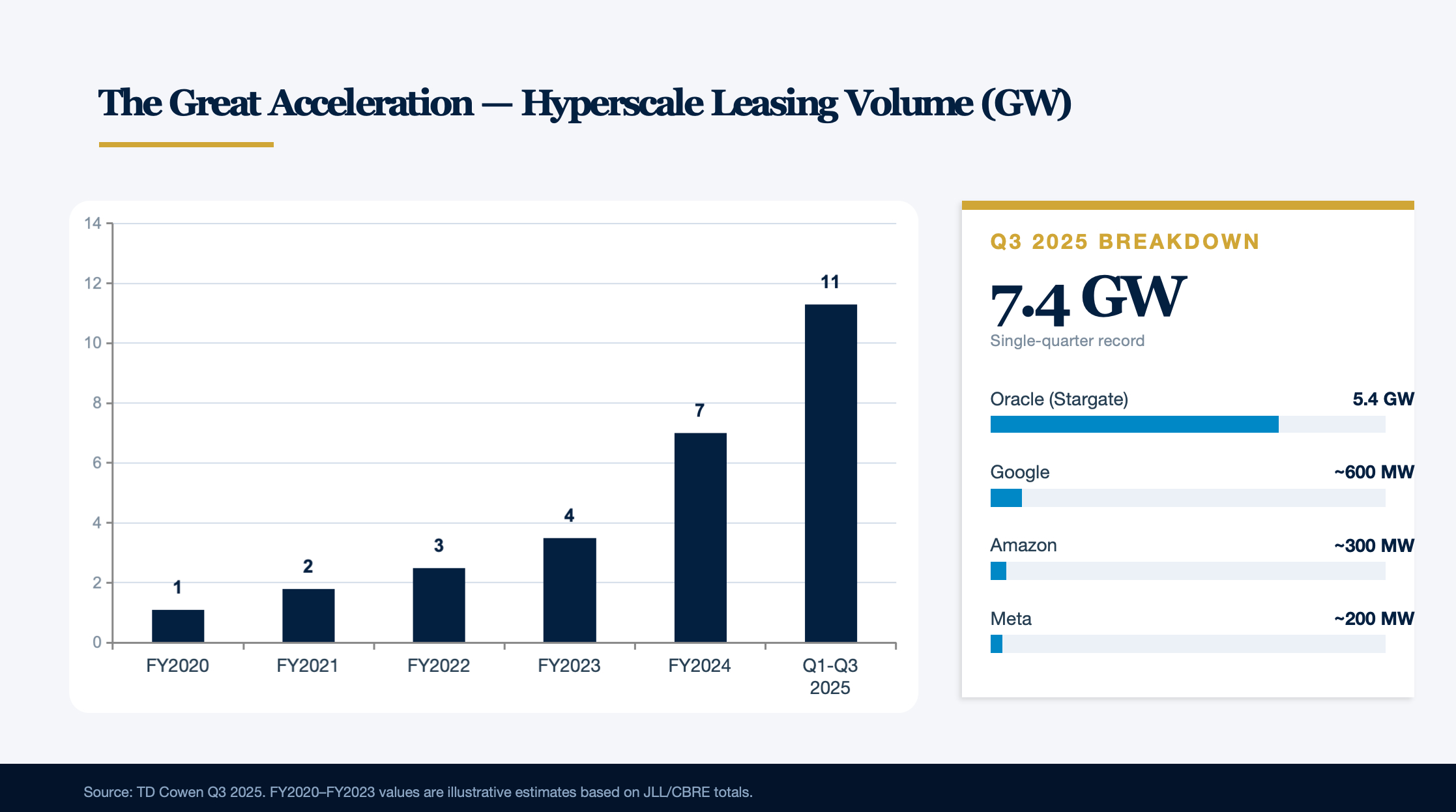

Net absorption surges. Full-year 2025 net absorption across major markets reached 2,497.6 MW (CBRE); datacenterHawk's broader tracking scope shows 15+ GW. The 2024 full-year figure of approximately 4.4 GW (JLL) represented a fourfold increase from 2020. Under-construction pre-lease rates stand at 74.3% (CBRE), with pre-lease timelines extending 3–4 years out.

The "Great Acceleration" in hyperscale leasing. TD Cowen confirmed that Q3 2025 single-quarter leasing volume reached 7.4 GW — exceeding the full-year 2024 total of 7 GW. Oracle accounted for 5.4 GW (supporting Stargate), Google ~600 MW, Amazon ~300 MW, and Meta ~200 MW. The first three quarters of 2025 aggregated to 11.3 GW. TD Cowen called this "the most significant demand inflection since the data center industry's inception."

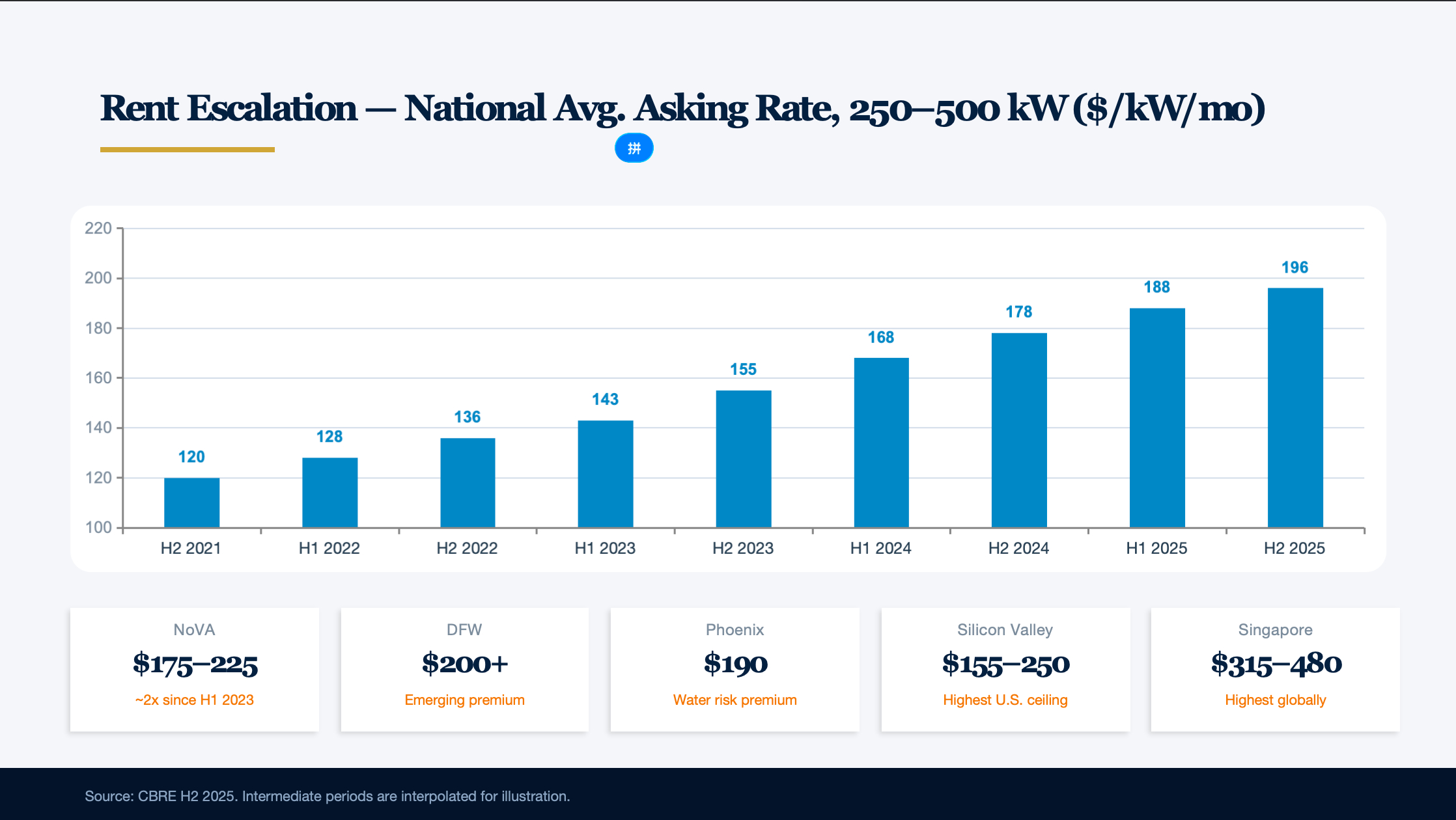

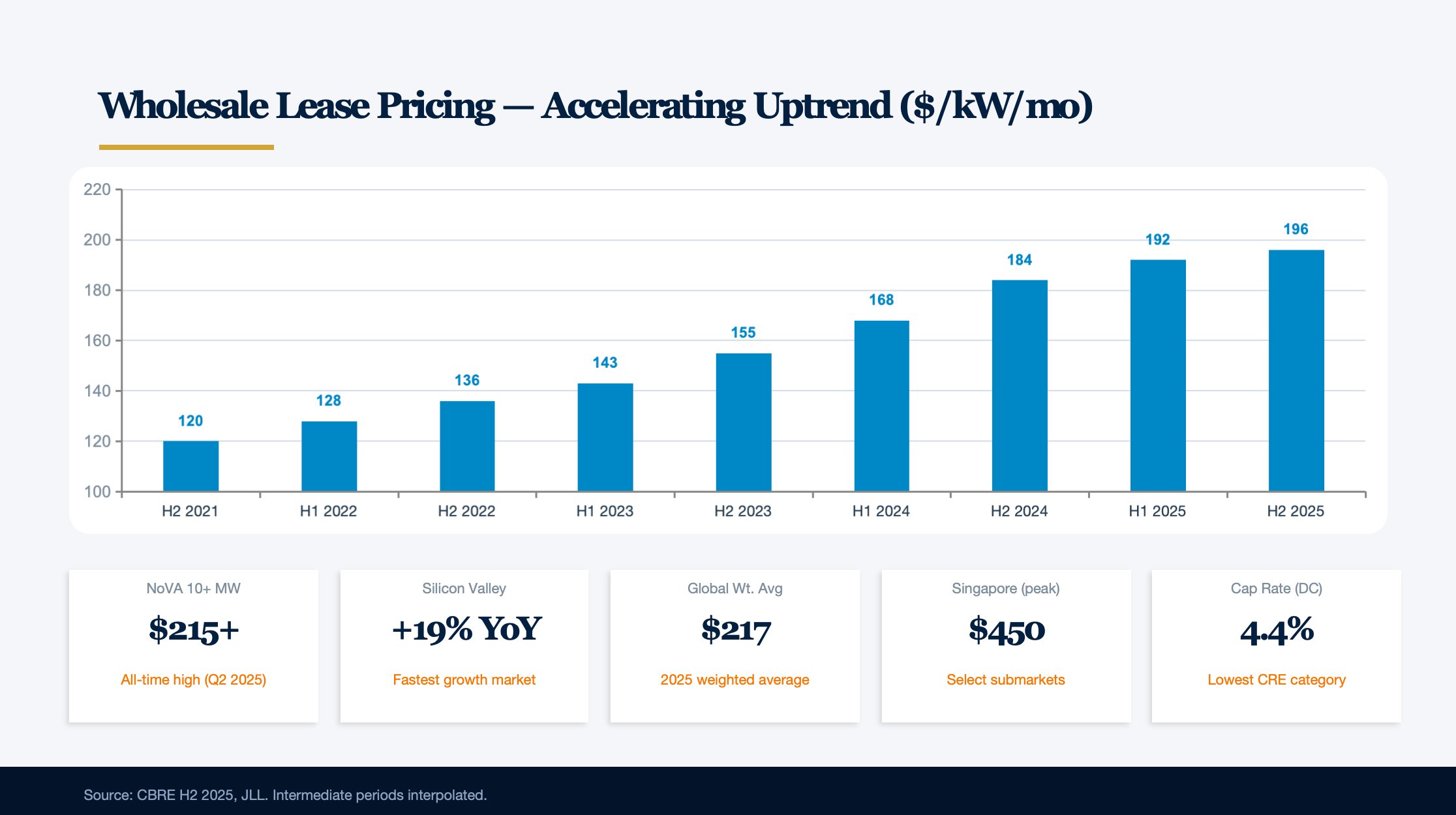

Rents continue to climb. The national average asking rate for 250–500 kW demand rose from approximately $120/kW/month in H2 2021 to $195.94/kW/month in H2 2025 (CBRE) — a 63%+ increase over four years and the fourth consecutive year of growth. Large-block 10–30 MW demand saw even steeper 19% increases. NoVA wholesale rents broke through $215/kW/month in Q2 2025 — a new all-time high. CBRE expects rents to remain above $200/kW/month in 2026.

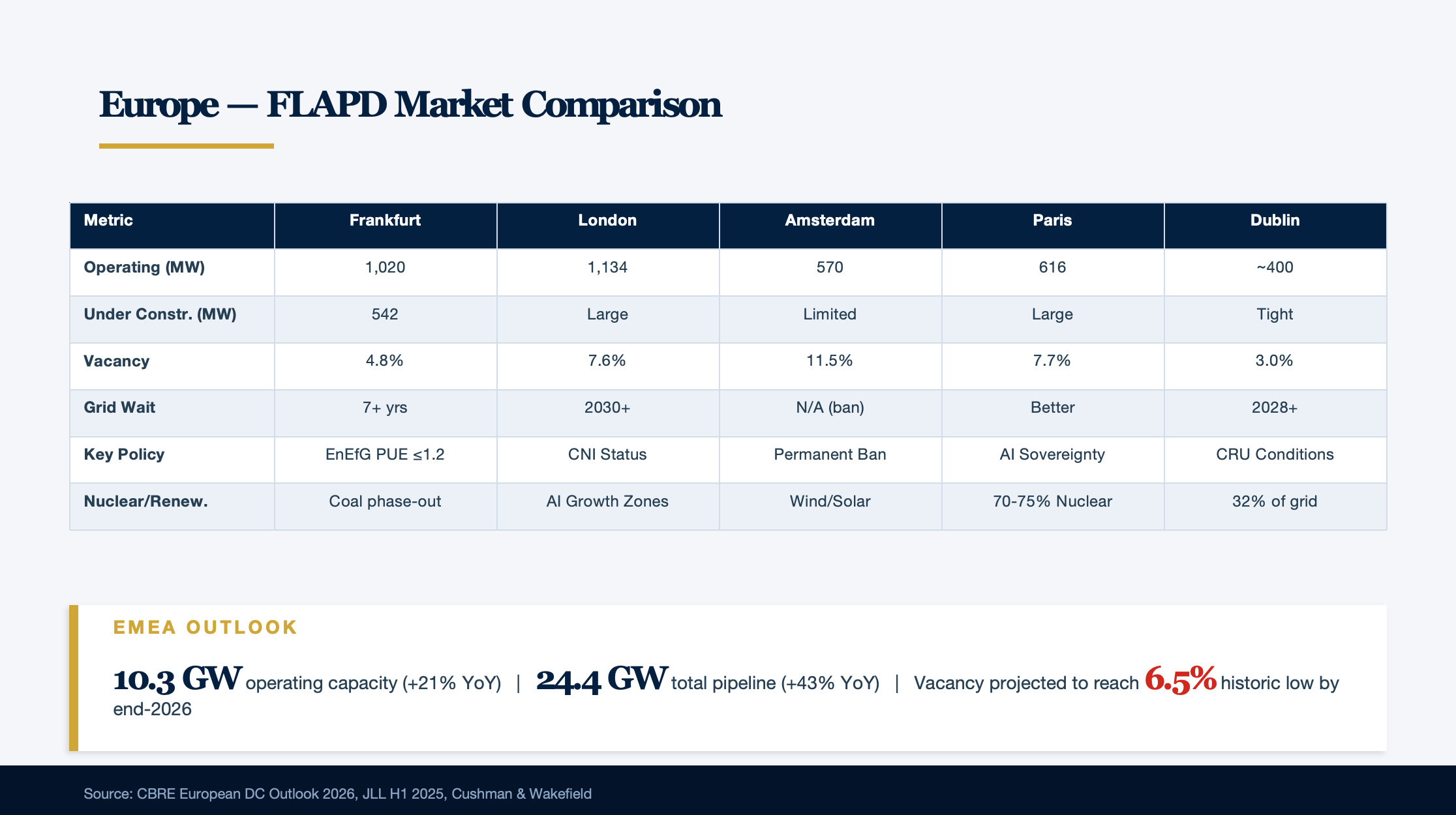

Part II: Europe — Regulatory-Driven Green Transformation and Expansion

EMEA operating capacity stands at 10.3 GW (Cushman & Wakefield H1 2025, up 21% YoY), with 2.6 GW under construction, 11.5 GW in planning, and a 24.4 GW total pipeline (up 43% YoY). New capacity additions of approximately 850 MW in 2025 and a projected 710 MW in 2026 are expected to fall short of 848 MW in projected demand, driving vacancy still lower.

Vacancy is projected to fall to approximately 6.5% by end of 2026 — a historic low (CBRE European Data Centres Outlook 2026), down dramatically from 20.6% in 2019.

European construction costs exceed U.S. levels. Turner & Townsend's 2025 index shows Zurich at $14.2/W, Paris and Amsterdam at $10.8/W, Madrid and Dublin at $10.0/W, versus Atlanta at $9.9/W, Phoenix at $9.8/W, and Charlotte at $9.5/W. Drivers include: stricter sustainability regulation (EED compliance costs), limited contractor pools, higher labor costs (UK MEP wages up 12% YoY in 2025), transformer delivery times extending from 26 to 42 weeks, post-Brexit skills shortages, and more complex planning environments. 60% of industry respondents expect construction costs to increase by 5–15% in 2026.

The FLAPD Five: Divergent Paths Among Core Markets

Frankfurt reached 1,020 MW of operating capacity (CBRE Q2 2025), becoming the second European city after London to breach 1 GW. Vacancy is 4.8%, projected to fall to 3.4% by year-end. Approximately 542 MW is under construction. Frankfurt faces unique regulatory pressure — Germany's Energy Efficiency Act (EnEfG), effective September 2023, imposes strict requirements: new data centers must achieve PUE ≤ 1.2 by July 2026; 100% renewable energy supply by January 2027; and waste heat utilization ≥ 20% by July 2028. Grid interconnection wait times exceed 7 years, with some developers shifting 30–40 km west to find power. However, the 2025 CDU/SPD coalition agreement signals potential relaxation of PUE and waste heat requirements. Hyperscaler investment in Germany is substantial: Microsoft €3.2 billion, AWS €8.8 billion (through 2026), Google €5.5 billion (through 2029).

London maintains its position as the largest EMEA market with 1,134 MW of operating capacity, but faces severe growth bottlenecks. West London's grid is fully allocated through 2029, with new projects waiting until 2030 or later. National Grid ESO has suspended new 132 kV connection offers in Greater London; self-built substations require an additional £150 million per 100 MW. Data centers already consume 18% of West London's electricity. Alternative zones are emerging rapidly — East London (Dagenham, Havering), Crawley, and northern regions. Vacancy has fallen to a historic low of 7.6% (JLL H1 2025), with large-block (5 MW+) vacancy at just 5.9%. The UK government announced a £14 billion AI data center program in January 2025, designating data centers as Critical National Infrastructure and establishing AI Growth Zones (minimum 500 MW each).

Amsterdam has the most restrictive policy environment among the FLAPD markets. Operating capacity stands at 570 MW, having been overtaken by Paris to drop to Europe's third-largest. Policy evolution: July 2019 sudden moratorium → 2022 lift with PUE ≤ 1.2 conditions → November 2022 national ban on hyperscale (>10 hectares and >70 MW) → April 2025 Amsterdam announces a permanent ban on new data center construction and expansion, with reassessment in 2030. This is not a "2035 ban" — there is no specific 2035-targeted legislation. The actual situation is an ongoing national hyperscale ban plus Amsterdam's comprehensive new-build prohibition. Netherlands data center count declined from 189 in 2019 to 187 in 2023, with colocation operators falling from 111 to 95. Vacancy at 11.5% is the highest among the FLAPD markets, but demand is being artificially suppressed by policy — international wholesale demand has largely redirected to other European markets.

Paris is achieving leapfrog growth through France's AI sovereignty strategy. Operating capacity reached 616 MW (CBRE Q2 2025), overtaking Amsterdam to become Europe's third-largest market in 2024. Vacancy plunged from 16.1% to 7.7% within a year — the steepest decline of any market. Early-stage pipeline exceeds 1.8 GW. France's AI action plan has announced €109 billion in investment, headlined by a 1.4 GW Paris AI Supercampus — a joint €8.5 billion venture between MGX (Abu Dhabi), Bpifrance, NVIDIA, and Mistral AI, breaking ground in H2 2026 with operations by 2028, billed as "Europe's largest AI campus." Brookfield has committed €20 billion to French AI infrastructure. France's core competitive advantage lies in nuclear power — approximately 70–75% of electricity comes from nuclear, providing stable, low-carbon, price-predictable baseload power.

Dublin has a vacancy rate of just 3% (JLL H1 2025), with large-block (5 MW+) vacancy even lower at 1.3% — pre-lease rates of 94.8% are the highest in EMEA. Data centers already consume 21% of Ireland's total electricity, projected to reach 32% by 2026. EirGrid has imposed a de facto grid connection moratorium on the Dublin region since 2021, expected to continue through 2028. In December 2025, the CRU issued a landmark final decision requiring large energy users (>10 MVA, Tier B) to: (1) provide dispatchable on-site/near-site generation matching 100% of maximum import capacity; (2) connect generation independently to the grid and participate in the SEM; (3) match 80% of annual consumption with additional renewable energy within Ireland (existing REFIT/RESS contracts ineligible); and (4) achieve renewable energy compliance within 6 years of energization. This effectively ends the 4-year moratorium, but on highly demanding terms.

Emerging European Markets: The "Second Tier" Takes Shape

The Nordics offer a unique combination of climate and renewable energy advantages — collectively sourcing 90%+ of electricity from renewables, with prices 40–50% below Western European core markets. Finland leads in growth (CAGR 9.10%), with a pipeline exceeding 5 GW. TikTok is investing €1 billion in Finland; XTX Markets is building a 250 MW supercompute campus in Kajaani for over €1 billion. In Sweden, Brookfield announced a $10 billion AI data center investment in Strängnäs (initial 300 MW, expandable to 750 MW) — the largest planned AI infrastructure cluster in Europe. Norway has attracted the OpenAI Stargate Norway project (Narvik, 230 MW renewable-powered AI campus), while CoreWeave has committed $2.2 billion to three Nordic data centers. Iceland, with 100% renewable energy (geothermal + hydro) and year-round free cooling, is emerging as ideal for energy-intensive AI workloads.

Southern Europe is experiencing an unprecedented investment boom. Portugal's Start Campus SINES is Europe's largest single colocation site — 1.2 GW total capacity, €8.5 billion total investment. The first facility SIN01 (26 MW) went live in April 2025; subsequent buildings (SIN02–06) scale up to 240 MW each, targeting rack densities of up to 700 kW/rack, PUE of 1.1, and zero WUE (seawater cooling). Microsoft has announced a $10 billion investment at Start Campus. Spain's market is valued at $6.89 billion (2025), with IT load CAGR of 23.92%. Italy/Milan has been elevated to "Powerhouse" market status by Cushman & Wakefield, with projected total capacity reaching 1.2 GW. Greece/Athens has planned capacity of 250+ MW — 6 times existing capacity — and has been upgraded to "Developing" market status.

Poland/Warsaw is Central and Eastern Europe's bridgehead — installed capacity of 660 MW (2025), projected to reach 1,000 MW by 2030. Hyperscale and enterprise AI commitments exceed $6 billion. Grid interconnection takes approximately 18 months, with an annual ICT talent gap of 50,000 professionals.

Part III: Asia-Pacific — An AI Investment Tsunami Sweeps the Region

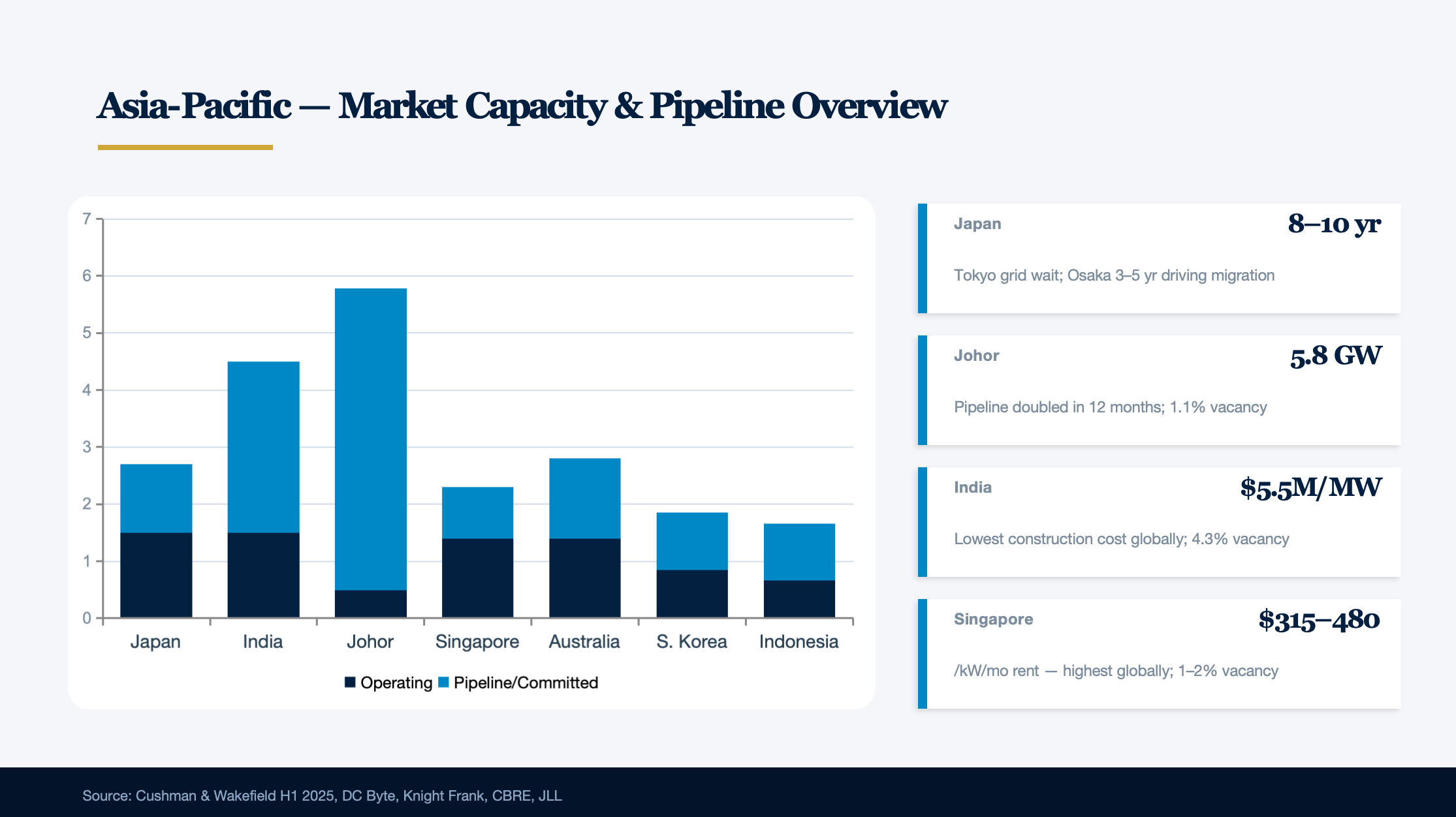

Asia-Pacific is experiencing the most dramatic data center expansion wave globally. Japan's construction pipeline exceeds 1.2 GW, Johor has 5.8 GW of committed capacity, and India's operational capacity has surpassed 1.5 GW — these three figures encapsulate a core reality: AI-driven compute demand is rewriting the Asia-Pacific data center map, creating a once-in-a-decade window for M&A investors.

Japan — Structural Opportunity Behind the Power Bottleneck

Three Markets Diverge; Osaka and Hokkaido Rise

Japan's data center market is valued at approximately $12.76 billion in 2025 (Arizton), with operational IT load capacity of approximately 1.5 GW (Cushman & Wakefield H1 2025), projected to reach $38.9 billion by 2031 (CAGR 20.42%). Tokyo still commands 40.7% market share, but Osaka is the fastest-growing region at 13.28% CAGR.

| Metric | Tokyo | Osaka | Hokkaido |

|---|---|---|---|

| Operating capacity (est.) | ~800–1,000 MW | ~300–400 MW | ~50 MW |

| Under construction / pipeline | 1.3 GW+ | 440 MW+ | 300 MW+ (SoftBank) |

| Wholesale rent ($/kW/mo) | $190–355 | Slightly below Tokyo | Lower (undisclosed) |

| Industrial power rate (¥/kWh) | ~¥18–20 | ~¥17–19 | Lower (renewable PPA) |

| Grid connection wait | 8–10 years (>10 MW) | 3–5 years | Relatively short |

| Natural disaster risk | High (earthquake + liquefaction) | Moderate (typhoon/storm surge) | Low-moderate (heavy snow) |

Tokyo's primary bottleneck is TEPCO power queues exceeding 36 months (154 kV connection waits can stretch to 7 years), while Osaka's 3–5-year timeline is driving significant developer migration to the Kansai region. OCCTO projects that electricity consumption from data centers and semiconductor factories will surge from 3.6 TWh in FY2025 to 51.4 TWh by FY2034 — roughly a 14-fold increase.

Emerging markets: Kyushu/Fukuoka is rising rapidly, with APL+GCI planning a 250 MW campus (first phase 120 MW, operational 2027). Hokkaido's SoftBank Tomakomai project spans 700,000 sqm with long-term potential of 1 GW, powered entirely by local renewables.

Japan Operator Landscape: NTT Leads; New Entrants Charge In

NTT is Japan's and one of the world's largest data center operators, with approximately 1,500 MW of global capacity, planning to double to 4 GW across 34 projects and targeting 5 GW+ within five years. Its most strategically significant move was the NTT DC REIT listing on the SGX on July 14, 2025, raising $773 million — Singapore's largest REIT IPO in over a decade, at 4.6x oversubscription and a projected annualized distribution yield of 7.5%.

SoftBank is the most aggressive AI data center player: the Sakai factory (initial 150 MW, expandable to 400 MW+, ¥100 billion investment, JV with OpenAI) and the Tomakomai project (initial 50 MW, long-term 1 GW). SoftBank also acquired DigitalBridge for $4 billion, gaining a global digital infrastructure management platform.

AirTrunk (Blackstone-owned) has invested over $8 billion in Japan across four campuses totaling approximately 530 MW. TOK1 secured a ¥191.6 billion ($1.24 billion) green loan — the largest data center financing in Japanese history. Princeton Digital Group is investing $1 billion in a 96 MW campus in Saitama, with rack density of 140 kW/rack.

Policy Tailwinds and FEFTA Scrutiny Coexist

The Japanese government offers multi-layered policy support. METI's Clean Energy Investment Subsidies provide up to 50% capex subsidies (from FY2026, over 5 years), with data centers explicitly included. The government has committed to investing at least ¥10 trillion ($66 billion) in AI by 2030.

Nuclear restart is a key variable. As of April 2026, Japan has 15 reactors operating, with total installed capacity of approximately 33 GW. TEPCO's Kashiwazaki-Kariwa Unit 6 restarted in February 2026 (1,356 MW) — TEPCO's first nuclear restart since Fukushima.

FEFTA foreign investment review requires prior notification and approval for acquisitions touching telecommunications and cybersecurity (triggered at 1% for listed companies). FY2024 filings hit a record 2,903. However, 2026 legislative amendments aim to narrow IT-sector review to critical cybersecurity operations only, potentially reducing the burden on pure real estate data center transactions.

M&A opportunity assessment: Yen depreciation (2024–2025 range: 145–160), relatively reasonable asset valuations, and increasing asset-sale willingness from domestic companies (NEC has already divested data centers; Fujitsu and Hitachi may follow) create a favorable entry window for foreign investors. Osaka Bay Area brownfield conversions of former factory sites (with existing power capacity) offer a low-cost entry path. Tokyo central-area data center development land commands premiums of up to 770% (for power-secured parcels).

Southeast Asia — The Johor Frenzy and Singapore Scarcity

Singapore: The Tightest Supply and Highest Rents Globally

Singapore's data center market is characterized by extreme undersupply: operating capacity of approximately 1.4 GW, vacancy of just 1–2% (CBRE Q1 2025), available capacity dipping as low as 4 MW, and wholesale rents of $315–$480/kW/month — the highest in the world. This scarcity stems from a de facto construction moratorium imposed in 2019.

DC-CFA2 was released in December 2025, opening at least 200 MW of new capacity. Selection criteria are significantly more stringent than the first round: PUE ≤ 1.25, renewable energy share ≥ 50% (from qualified green pathways; conventional RECs ineligible), and mandatory Green Mark for Data Centres 2024 Platinum certification.

The Jurong Island 700 MW Low-Carbon Data Center Park, announced in October 2025, is a joint EDB-JTC development. At 700 MW, it represents 50% of Singapore's existing capacity — a transformative expansion.

Of particular note, KKR and Singtel are acquiring the remaining 82% of STT GDC for approximately S$6.6 billion, at an implied enterprise value of approximately S$13.8 billion, expected to close in H2 2026 — one of the largest data center M&A transactions in Southeast Asia.

Johor: Asia-Pacific's Most Aggressive Data Center Expansion

Johor is experiencing the most concentrated investment surge in data center construction history. Per DC Byte (July 2025), Johor has 487 MW operational, 324 MW under construction, 1.4 GW committed, and 3.4 GW in early-stage planning. Knight Frank H1 2025 reports total pipeline supply of approximately 5.8 GW (doubling within 12 months), with vacancy of just 1.1%. The Johor state government has approved 51 projects totaling RM 182.96 billion in investment. Cushman & Wakefield projects Johor will become a 1 GW market by end of 2026.

Key projects:

| Operator | Capacity | Investment | Status |

|---|---|---|---|

| YTL Data Centers | 600 MW | RM 10 billion | Operational / Under construction |

| Bridge Data Centres MY07 | 400 MW | — | Under construction |

| AirTrunk JHB1+JHB2 | 420 MW+ | RM 9.7 billion | Operational / Under construction |

| Princeton Digital JH1+ | 350 MW+ | — | Operational / Under construction |

| Microsoft | Multi-phase | US$2.2 billion | Under construction / Planned |

| Currenc Group | 500 MW | — | Planned |

TNB (Tenaga Nasional) grid expansion is the critical bottleneck. TNB has signed 31 ESAs totaling 4,700 MW of demand and received new DC applications exceeding 11,000 MW (over 40% of Peninsular Malaysia's existing installed capacity). Actual DC utilization is only 47% of allocated capacity, raising waste concerns. Base electricity rates were raised to 45.62 sen/kWh from July 2025, but remain among the lowest in Asia-Pacific (~US$0.10/kWh vs. Singapore's US$0.27/kWh).

Core risk — water constraints: Johor has mandated that DC investors defer water-cooled expansion by at least 18 months (to mid-2027) and has stopped approving Tier 1/2 data centers. 2024 DC water allocation was just 6.10 MLD — only 21% of the amount requested. Projected 2030 DC water demand reaches 384 MLD.

The JS-SEZ (Johor-Singapore Special Economic Zone), signed in January 2025, offers qualifying enterprises a 5% corporate tax rate (up to 15 years). Singapore-Johor fiber latency is <5 ms. Singapore enterprises are broadly adopting a "dual hub" strategy: latency-sensitive workloads remain in Singapore, while GPU training and AI inference migrate to Johor.

Indonesia, Thailand, Vietnam, and the Philippines Each Occupy Distinct Positions

Indonesia: Jakarta's market stands at approximately 660 MW in 2025, with vacancy declining from 36% to 31%. DCI Indonesia (DCII) is the largest operator with 155 MW of 2025 capacity, revenue of IDR 2.54 trillion (+40.1%), and EBITDA margin of 61%. DCI-H3 Sky Bintan is planned for over 1,000 MW. Telkom is seeking strategic investors, potentially unlocking a ~US$1 billion opportunity — a notable M&A target.

Thailand: H1 2025 saw 28 approved projects totaling $16.1 billion investment (20x YoY growth). BOI offers 8-year corporate income tax exemption for high-efficiency DCs, with 100% foreign ownership permitted. Construction cost of only $7.1M/MW, though power at $108/MWh is mid-range.

Vietnam: Market is emerging with 41 DCs and 221 MW. 100% foreign ownership became effective January 2025. Construction cost is among Asia-Pacific's lowest at $6–8M/MW. Power supply reliability remains the core challenge.

Philippines: Manila at approximately 560 MW in 2025, with power costs of $154/MWh among the highest in Southeast Asia. SM Investments' August 2025 exit from the DC business, citing power costs and natural disaster risk, is a signal M&A buyers should note.

India — 3 GW Ambition and 60% Idle GPUs

Four Markets Drive 1.5 GW of Operational Capacity

India's 2025 data center operational IT load capacity reaches 1,123–1,530 MW (JLL/CBRE), with national vacancy at just 4.3% — extremely tight. Investment commitments from 2019–2025 exceed $94 billion cumulatively. Construction cost is among the world's lowest at approximately $5–5.5M/MW.

| Metric | Mumbai | Chennai | Hyderabad | Pune |

|---|---|---|---|---|

| Operating capacity | ~594 MW | ~550 MW | ~50 → rapid growth | ~90–100 MW |

| Market share | 41–54% | 20–23% | ~13% | ~5% |

| Power bottleneck | 36-month backlog | Grid delays | Relatively better | Better than Mumbai |

| Submarine cable connectivity | 2+ landing stations | 7+ cables / 420+ Tbps | None direct | None direct |

Chennai's core advantage is submarine cable connectivity — 7+ active cables with aggregate bandwidth of 420+ Tbps, positioning it as the top choice for latency-sensitive use cases such as gaming and financial trading.

Operator Landscape: GPU Concentration Is Striking

Yotta Infrastructure (Hiranandani Group) confirmed in a February 2026 CNBC interview that it holds 60–70% of India's GPU capacity. Currently operating approximately 10,000 H100 GPUs, with thousands of B200s deployed and 20,736 Blackwell Ultra B300 GPUs planned for August 2026 deployment. IPO target valuation: $4 billion.

AdaniConneX (Adani 50:50 EdgeConneX JV) is targeting 1 GW by 2030. Most notably, it signed a $15 billion AI data center partnership with Google (Visakhapatnam, GW-scale), including submarine cable and renewable energy infrastructure.

Reliance Jio has planned the world's largest single data center — Jamnagar 3 GW, with $20–30 billion investment, powered by a 5,000-acre green energy complex, targeting 24-month completion. Jio IPO is planned for H1 2026 at a target valuation of $120 billion.

Indian Policy: Interstate Competition Is Fierce; National Framework Pending

India classified data centers in the "Harmonized Master List" in 2022, granting infrastructure status and access to long-term, low-cost financing. The latest 2025 draft national policy proposes up to 20-year conditional tax exemptions, 100% electricity duty exemption, and data center SEZs. However, significant state-level policy variation persists, with no unified national policy.

100% FDI is open through the automatic route, but border-country entities (China, etc.) require government approval. In practice, approximately 30 separate approvals are needed. Key reference transactions: Equinix acquired GPX at 15x forward EBITDA ($161 million), and Blackstone + Panchshil committed $2.3 billion (500 MW).

Australia — The AirTrunk Benchmark and NEXTDC Deep Dive

Sydney Vacancy Falls to 5.2%; Western Sydney Becomes the New Engine

Australia's operating capacity stands at approximately 1.3–1.5 GW (2025), with a total pipeline of ~2.8 GW. Sydney H1 2025 vacancy plummeted from 9% to 5.2%, with average lease-up time compressing from 40 months (2020) to 13 months.

AirTrunk was acquired by Blackstone + CPP for A$24 billion (US$16.1 billion) — the largest data center transaction in history. Five Australian campuses total over 1.2 GW, with 800+ MW committed to customers. Reports from April 2026 indicate AirTrunk is planning a REIT-style IPO in Singapore to raise $1.5 billion.

NEXTDC (ASX:NXT) — Australia's Only Large-Scale Independent Pure-Play Data Center Stock

NEXTDC is the key reference for understanding Australian data center valuations.

| Metric | FY25 | 1H26 |

|---|---|---|

| Revenue | A$350.2M (+14%) | A$189.2M (+13%) |

| EBITDA | A$216.7M (+6%) | A$115.3M (+9%) |

| Contracted utilization | 244.8 MW (+42%) | 416.6 MW (+137%) |

| Billed utilization | 110.9 MW | 119.8 MW |

| Forward order book | — | 296.8 MW (FY26–29 conversion) |

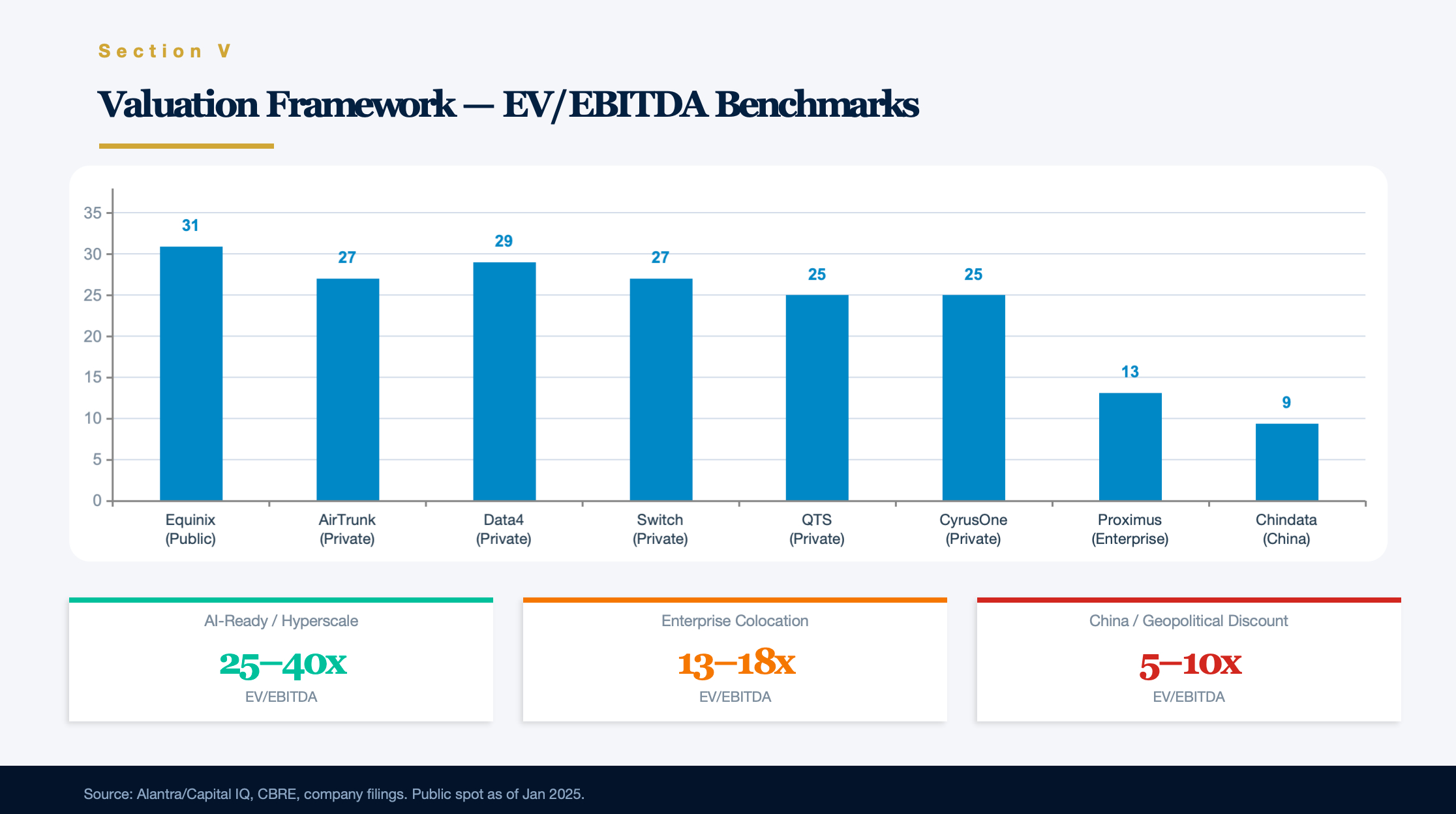

Market cap of approximately A$8.9–9.3 billion; EV/EBITDA ~55x (TTM) — well above Equinix's 25–30x and Digital Realty's 20–25x, reflecting high growth expectations. Development pipeline totals over 3 GW, including S7 Eastern Creek (550+ MW, OpenAI MOU) and M4 Port Melbourne (150–162 MW, $2 billion AI Factory with liquid cooling). A full acquisition of NEXTDC would require approximately A$10–12 billion, which is feasible relative to AirTrunk's A$24 billion.

South Korea — Nuclear Advantage and Grid Bottlenecks

Seoul Vacancy Is Asia-Pacific's Second-Lowest; Power Limits Drive Decentralization

South Korea's data center operating capacity stands at approximately 850 MW (58 colocation facilities), with Seoul accounting for 52.1% and vacancy below 6% (Asia-Pacific's second-lowest after Singapore). Construction costs run approximately $10–11M/MW.

Seoul faces severe power supply constraints. KEPCO has announced restrictions on new power supply in the Seoul metropolitan area, extending power supply confirmation times to approximately 12 months. KEPCO debt exceeds KRW 202 trillion, severely constraining grid upgrade budgets.

SK + AWS Ulsan 1 GW Project: Asia-Pacific's Largest AI Data Center Partnership

Total investment of KRW 7 trillion (~$5.11 billion), with AWS contributing approximately $4 billion. First phase 41 MW (November 2027), second phase 103 MW (February 2029), long-term target 1 GW, deploying 60,000 GPUs — Korea's largest-scale deployment. Groundbreaking on August 29, 2025.

South Korea's nuclear fleet generates approximately 31% of total electricity, with 25 operating reactors totaling 30,054 MW. The government has reversed its predecessor's nuclear phase-out policy, planning 2 new reactors plus 1 SMR.

China — Accelerating Domestic Substitution and C-REIT Breakthrough

GDS and VNET Diverge; DayOne Could Reach $5 Billion Valuation

GDS Holdings FY2024 China revenue of RMB 10.322 billion (+5.5%), adjusted EBITDA margin of 47.2%. In Q1 2025, GDS secured 152 MW of AI-related orders — the largest single domestic booking ever. International operations, rebranded DayOne, raised over $2 billion in Series C funding (Coatue-led), with valuation potentially reaching $4–5 billion.

VNET Group FY2024 revenue of RMB 8.259 billion (+11.4%), with wholesale IDC revenue surging +125.4% in Q4. Turned to net profit (RMB 248 million) for the first time.

Chindata was taken private by Bain Capital for $3.16 billion (~9.4x EV/FY23E EBITDA). In March 2026, Bain is considering selling up to 70% of its stake (Citigroup/JPMorgan advising) — a significant M&A opportunity signal.

East-to-West Computing: 63% Rack Utilization Exposes Regional Imbalance

Across eight national hub nodes, total compute stands at 215.5 EFLOPS, with AI compute accounting for 80.8% and rack utilization of approximately 63% — meaning roughly half of installed cabinets remain idle. The core contradiction: eastern regions face undersupply while western regions lack sufficient local demand.

Domestic Chip Substitution Rate Surges from 15% to 30%

In China's 2024 AI accelerator market of 2.7+ million units: NVIDIA 66%, Huawei HiSilicon 23%, AMD 5%. Domestic brands shipped 820,000 units (penetration rate 30%, up from 15% in 2023). Jensen Huang acknowledged NVIDIA's China share fell from 95% four years ago to 50%. The April 2025 U.S. ban on H20 exports to China will further accelerate domestic substitution.

Huawei Ascend 910C (2025 mass production): FP16 peak 800 TFLOPS, HBM 128 GB. Inference performance reaches 60–80% of H100. Ascend holds 79% market share in municipal smart computing centers.

C-REIT Breakthrough: First Two Data Center REITs Approved

On June 18, 2025, the China Southern GDS Data Center REIT and China Southern Runze Technology REIT received CSRC registration approval — officially breaking the ice for China's public data center REITs. Globally, only 6 pure data center REITs exist (5 in the U.S. + 1 in Singapore); China's DC REITs are at a nascent stage, facing valuation challenges from rapid technology iteration and short hardware depreciation cycles (3–5 years).

The DeepSeek Effect: Jevons Paradox Drives Demand Up, Not Down

DeepSeek-V3 training cost was only $5.576 million (1/10th of Meta's open-source models); R1 inference costs are 95% lower than OpenAI o1. Yet the industry consensus holds: efficiency gains → cost reductions → broader enterprise adoption → net demand increase (Jevons Paradox). DeepSeek-V3.1 adopts UE8M0 FP8 Scale precision, specifically designed for domestic chips.

M&A Decision Framework: Key Takeaways

Tier 1 — Priority Focus

Osaka, Japan

Core thesis: Best risk-adjusted entry point in developed Asia.

Power access timeline of 3–5 years (far superior to Tokyo's 8–10 years), brownfield factory conversions with existing power capacity, yen depreciation lowering acquisition costs, and METI offering 50% capex subsidies. Domestic companies (NEC et al.) showing increased willingness to divest assets.

Key considerations:

- Japanese enterprise customer relationships are dominated by NEC, Fujitsu, and NTT — foreign operator go-to-market capability is the critical success factor. Partnership or JV with a local incumbent may be required for customer access.

- Osaka construction cost, while lower than Tokyo ($15.2/W, global highest), remains significantly above Southeast Asian markets. AI-ready retrofit costs (liquid cooling, high-density power distribution) may be underestimated.

- FEFTA review for "critical infrastructure" category is tightening — timeline and conditions require early legal engagement.

- Exit channels: Mature capital markets, but limited data center REIT universe. Trade sale to hyperscaler or infrastructure fund is the primary path. Tokyo Stock Exchange J-REIT structure available but underutilized for data centers.

Johor, Malaysia

Core thesis: Singapore overflow market with structural cost advantages at the earliest stage of hypergrowth.

1.1% vacancy and a 5.8 GW pipeline indicate a market in the early stages of explosive growth. Bridge Data Centres (Bain exploring sale of up to 70%) is an explicit, actionable M&A target. JS-SEZ's 5% corporate tax and electricity at $0.06–0.08/kWh (vs. Singapore $0.15+) provide structural cost advantages that are difficult to replicate.

Key considerations:

- The strategic value is defined by geographic substitution — Singapore itself is nearly impossible to acquire new capacity (see Tier 3), making Johor the de facto expansion corridor for Singapore-centric workloads.

- Water resource constraints are real but addressable through liquid cooling adoption (which is becoming standard for AI workloads regardless).

- TNB grid capacity is the binding constraint — validate grid upgrade commitments and timelines before committing capital.

- Bridge Data Centres (9 facilities, Bain Capital–backed, $2.8B secured financing in 2025) is the most clearly defined M&A opportunity in Southeast Asia. Valuation will likely reflect the 2024 AirTrunk benchmark (~25–30x EBITDA) given scarcity premium.

- Exit channels: Limited public market options in Malaysia. Primary exit via secondary PE sale or strategic acquisition. Singapore REIT listing (Keppel DC REIT model) is a viable cross-border exit structure.

Tier 2 — Strategic Positioning

Mumbai / Chennai, India

Core thesis: Largest long-term TAM in Asia-Pacific, but risk premium is real, not mispriced.

4.3% vacancy and $5–5.5M/MW construction cost present compelling unit economics. Yotta IPO ($4 billion), Sify IPO, and potential CtrlS IPO provide valuation anchors. The GPX transaction at 15x EBITDA serves as a reference multiple. Chennai's submarine cable infrastructure is uniquely differentiated.

Key considerations:

- The 15x EBITDA (GPX transaction) vs. 25–30x in developed markets reflects genuine risk premium, not pure valuation arbitrage. Grid reliability (frequent outages in secondary markets), land title complexity, and regulatory uncertainty in value-added telecom licensing for foreign investors are real discount factors.

- Mumbai 4.3% vacancy requires granular analysis — distinguish Navi Mumbai/Airoli campus-level data from broader metro averages. Indian market internal dispersion is extreme.

- Yotta's $4B IPO valuation requires scrutiny of underlying GPU asset composition — its reliance on NVIDIA H100 clusters and Huawei Ascend creates technology iteration risk analogous to CoreWeave's depreciation challenges.

- AdaniConneX (1 GW planned, $10B+ investment) and NTT India (292 MW, 20% market share) are reshaping the competitive landscape — new entrants face both opportunity and intensifying competition.

- Exit channels: Active IPO window (Yotta/Sify/CtrlS in pipeline). BSE/NSE listing is viable for scaled assets. Strategic sale to hyperscalers (AWS India expansion) provides alternative exit. InvIT (Infrastructure Investment Trust) structure available as REIT-equivalent.

Australia

Core thesis: Mature market with scarcity premium, but watch for valuation overextension.

AirTrunk's A$24 billion transaction (~A$30M/MW) establishes the valuation benchmark. NEXTDC (A$8.9 billion market cap, 3 GW pipeline) is the only large-scale independent target on the ASX. Sydney's 5.2% vacancy supports rental upside.

Key considerations:

- AirTrunk's ~30x EBITDA was a peak-cycle Blackstone acquisition — using it as a floor valuation for other assets risks overpayment.

- DigiCo REIT (Global Switch Australia) declined 65% post-IPO (A$5.00 → ~A$1.74) — a cautionary signal that Australian public markets do not uniformly support data center REIT premiums.

- NEXTDC's A$8.9B market cap already prices in significant growth expectations from its 3 GW pipeline. Margin of safety is limited at current levels.

- Melbourne and Perth are emerging as lower-cost alternatives to Sydney, with improving power availability.

- Exit channels: Deep ASX liquidity. A-REIT structure well-established. Trade sale to global PE (Blackstone/KKR precedent) highly viable. Most liquid exit market in Asia-Pacific.

Tier 3 — Selective Participation

Indonesia

Core thesis: Potentially the most undervalued pure-play opportunity in Southeast Asia.

DCI Indonesia (DCII, listed, 32% market share, 61% EBITDA margin) is one of Southeast Asia's most attractive listed targets. Telkom's strategic investor search could unlock a ~$1 billion opportunity. 280 million population with early-stage digitalization provides the largest untapped demand pool in ASEAN.

Key considerations:

- DCII's 61% EBITDA margin and 32% market share combination is exceptional — superior to most listed global peers. The listed status provides transparency and liquidity rare in emerging Southeast Asian markets.

- Telkom's strategic investor process, if executed, could offer entry at 15–18x EBITDA — attractive relative to 25–30x in developed markets.

- Long-term growth ceiling is higher than South Korea given demographic scale and digitalization trajectory.

- Regulatory environment (data localization requirements, foreign ownership limits in telecom) requires careful structuring.

- Exit channels: IDX listing provides liquidity for DCII. For private assets, exit depends on strategic sale or secondary PE transaction. No established REIT structure for data centers.

South Korea

Macquarie's Hwanam transaction ($580–720 million) provides valuation reference. Mid-cap operator consolidation opportunities exist. However, KEPCO grid bottlenecks and Seoul construction restrictions are binding constraints. Samsung SDS and LG CNS dominate enterprise relationships, limiting foreign operator customer access.

Exit channels: KOSPI/KOSDAQ listing viable but data center sector coverage is thin. K-REIT structure underdeveloped for digital infrastructure. Trade sale is primary path.

Singapore

Extremely scarce but nearly impossible to acquire new capacity. KKR's STT GDC 82% acquisition (S$6.6 billion) establishes valuation benchmark. Keppel DC REIT's S$1 billion internal transaction merits monitoring. DC-CFA2 and Jurong Island's 700 MW are the only new supply entry points.

Strategic note: Singapore's capacity scarcity is precisely what makes Johor (Tier 1) strategically valuable. Consider Singapore positioning through Johor assets with Singapore connectivity.

Exit channels: SGX is the premier REIT market in Asia for data centers (Keppel DC REIT, NTT DC REIT precedents). Highest exit liquidity for REIT-structured assets in the region.

Cross-Cutting Strategic Notes

Exit channel liquidity directly impacts achievable IRR. The ranking above implicitly factors in exit feasibility: Australia and Singapore offer the deepest public markets, India has an active IPO window, Japan has mature capital markets but limited DC REIT vehicles, while Johor and Indonesia depend primarily on private transactions.

The "Singapore + Johor" corridor should be evaluated as a single strategic unit. Singapore provides the demand anchor (financial services, regional HQs), Johor provides the supply capacity. Assets spanning both markets command a structural premium.

Hyperscaler capex allocation is the leading indicator. AWS, Google, and Microsoft's announced investments in specific markets (India $10B+, Japan $7B+, Malaysia $2B+, Indonesia $1.5B+) serve as demand validation. Markets without hyperscaler commitments carry higher demand risk regardless of supply-side attractiveness.

Five Structural Themes

Power is the binding constraint on everything. From Tokyo's 8–10 years to Seoul's 12+ months to Navi Mumbai's 36 months, power interconnection timelines determine project viability. Existing assets with secured power command premiums of up to 770% (Tokyo). TNB Johor has signed 4,700 MW but received 11,000 MW of applications — the gap is stark.

The AI density revolution is transforming the construction paradigm. Rack densities are leaping from 8–10 kW toward 20–40 kW (and as high as 140 kW at Princeton Tokyo). Liquid cooling is shifting from optional to standard. This means existing air-cooled facilities face costly retrofits, capex intensity for new builds is rising sharply, but per-square-meter revenue is rising commensurately.

REIT-ification is accelerating capital recycling. NTT DC REIT's SGX listing ($773 million), AirTrunk's planned REIT IPO ($1.5 billion), China's first C-REITs, and DigiCo REIT's ASX listing — REITs are becoming the core instrument for data center operators to recycle capital and fund expansion.

Domestic chip substitution creates unique risk and opportunity in the China market. Huawei Ascend penetration has moved from 15% to 30%, with further acceleration inevitable following the H20 export ban. Domestic chips' "volume-for-quality" strategy is driving mega-cluster and higher-density power demand. However, technology iteration uncertainty and geopolitical risk demand cautious assessment of China market exposure.

Water is scarcer than power. Johor has mandated an 18-month deferral of water-cooled expansion, with 2024 water allocation at just 21% of requested volumes. Singapore has only 733 km² of land area. This will drive zero-water cooling technologies (air cooling, closed-loop liquid cooling) to become a source of competitive differentiation and M&A valuation premiums.