Key Conclusions

The true non-China robotics leaders are not limited to humanoid robots. Mature leaders are mainly distributed across surgical robotics, industrial robotics, warehouse automation, collaborative robots, defense autonomous systems, and upstream supply chains. Examples include Intuitive Surgical, Teradyne / Universal Robots / MiR, FANUC, Yaskawa, ABB Robotics, Symbotic, AutoStore, Boston Dynamics, Anduril, Shield AI, Skild AI, Physical Intelligence, CMR Surgical, Locus Robotics, Exotec, as well as key upstream companies such as NVIDIA, Keyence, Cognex, SICK, Harmonic Drive, Nabtesco, maxon, Beckhoff, Bosch Rexroth, Schaeffler, and Jabil.

A First-Principles Decomposition of Robotics

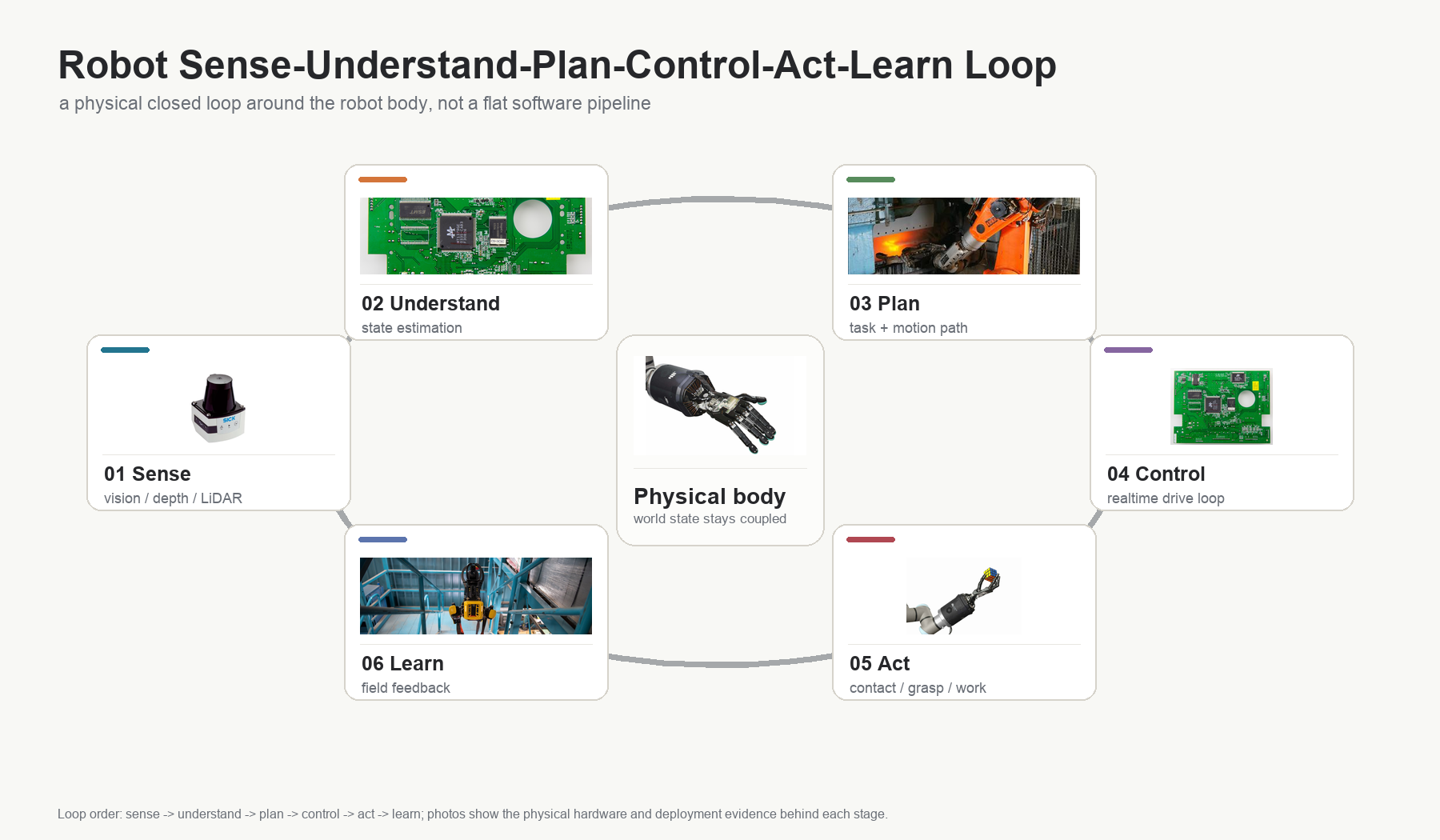

A robot is not "artificial intelligence that can move." It is a physical labor closed loop that connects perception, understanding, planning, control, execution, and feedback learning.

First, a robot must perceive the world. Cameras, LiDAR, millimeter-wave radar, force/torque sensors, tactile sensing, encoders, inertial navigation, microphones, and process sensors turn the real world into machine-readable signals.

Second, a robot must understand the world. It has to transform the environment into objects, spaces, semantics, task progress, risks, constraints, and failure-recovery paths.

Third, a robot must plan actions. It has to decide paths, grasp poses, action sequences, obstacle-avoidance strategies, priorities, and exception handling.

Fourth, a robot must control in real time. Motors, drives, joints, chassis, end effectors, balance, and safety boundaries all require millisecond-level control.

Fifth, a robot must execute real physical tasks. Reducers, motors, drives, grippers, hands, wheels/legs, structural parts, batteries, materials, and manufacturing processes turn algorithms into motion.

Sixth, a robot must keep learning. Failures in real deployments, human takeovers, teleoperation, simulation, customer logs, and maintenance records ultimately become iterative data for models, control policies, and hardware design.

The commercial value of robotics does not come from whether the form resembles a human, but from whether this closed loop can stably replace or augment human labor in real-world scenarios and generate verifiable economics: unit task cost, yield, downtime, maintenance cost, safety incident rate, deployment cycle, and asset payback period.

Illustration: a robot is not a single-point AI model, but a physical closed loop of "perception -> understanding -> planning -> control -> execution -> learning." The image uses real photos of sensors, control boards, robotic arms, dexterous hands, and deployment scenarios to represent each link.

Industry Chain Decomposition

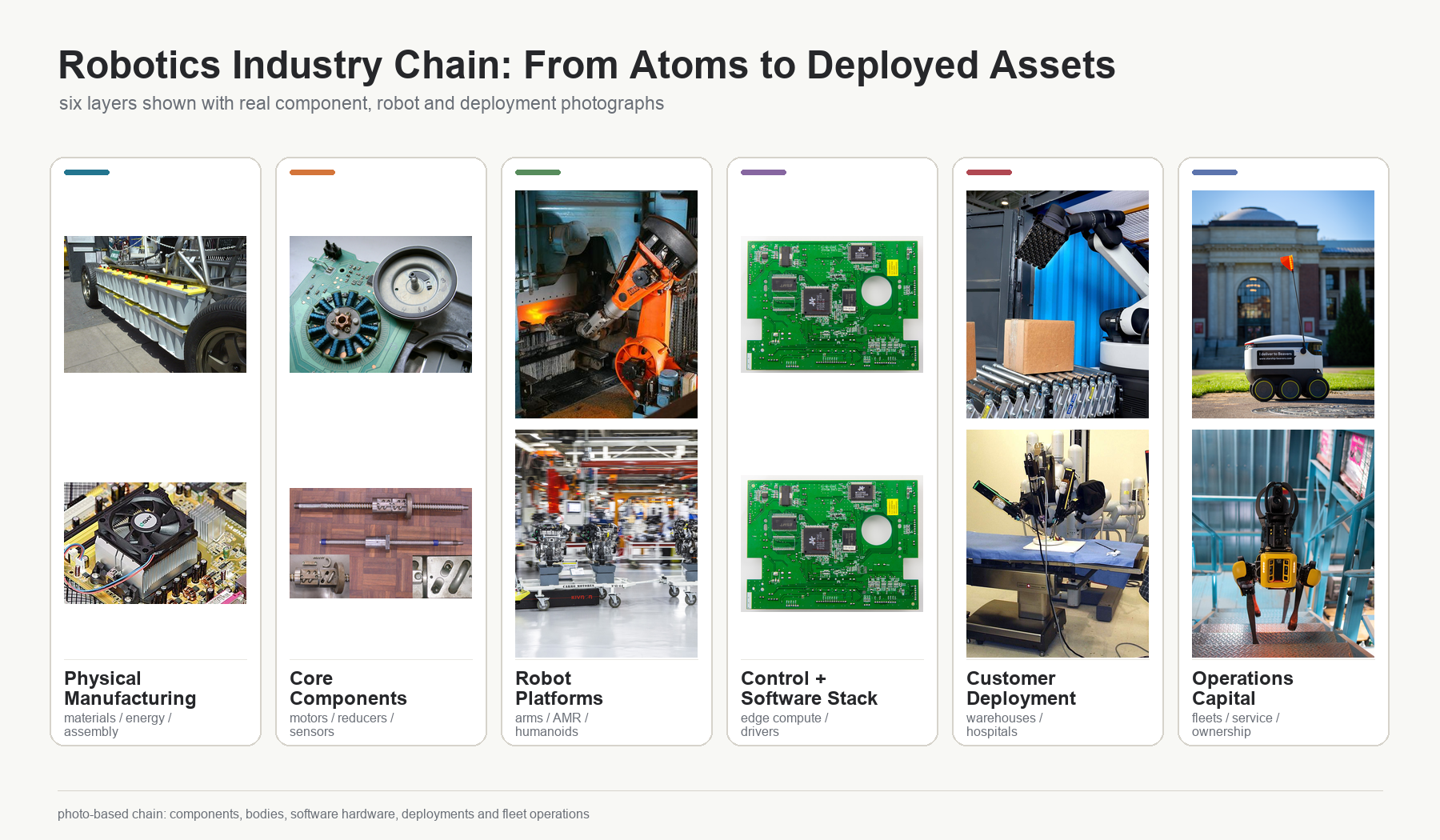

The robotics industry chain cannot be split only into four layers: "core components, robot body, applications, and capital." That split misses the most important directions of value migration: software stack, robot operating systems, simulation, data closed loops, and brain models. A more complete industry chain should be split into six layers.

Foundational physics and manufacturing, core components, robot body platforms, software stack and brain models, scenario integration and customers, and capital and operating infrastructure.

The first layer is foundational physics and manufacturing capability. This includes materials, structural parts, precision machining, molds, wire harnesses, connectors, sealing, thermal management, battery packaging, assembly processes, test fixtures, and quality systems. It determines whether robots can be manufactured stably, and it also determines the mass-production boundary of downstream robot-body companies.

The second layer is core components. This includes actuators, motors, reducers, servo drives, encoders, brakes, force/torque sensors, tactile sensors, cameras, LiDAR, millimeter-wave radar, inertial navigation, edge-computing modules, safety controllers, and battery management systems. It determines cost, lifetime, reliability, power density, perception accuracy, and supply stability.

The third layer is robot bodies and platforms. This is not a simple "list of robotics companies," but the packaging of core components into deployable machines: fixed robotic arms, collaborative arms, AMR/AGV, warehouse systems, mobile manipulators, humanoid robots, quadruped/biped robots, home/domestic/companion robots, scenario-specific service robots, surgical robots, drones, unmanned vehicles, unmanned vessels, and defense autonomous systems.

The fourth layer is the software stack and brain models. This includes robot operating systems, middleware, simulation, digital twins, data collection, teleoperation, SLAM, perception models, vision-language-action models, motion planning, task planning, control policies, fleet management, safety policies, logging systems, and training-data closed loops. Figure's Helix, NVIDIA Isaac / GR00T / Cosmos, Google DeepMind's robotics models, Skild AI, Physical Intelligence, and FieldAI all belong to this layer. Over the long term, value may migrate from single robot-body companies toward reusable software and model layers that work across bodies and scenarios.

The fifth layer is scenario integration and downstream customers. Robots ultimately enter automotive, electronics, metalworking, food and beverage, warehousing and logistics, retail delivery, hospitals, homes, energy inspection, agriculture, mining, national defense, and public safety. The key question here is not "can the robot be demonstrated," but whether it can connect into customer workflows, pass safety certification, run stably, reduce downtime, and generate economics on real KPIs.

The sixth layer is capital and operating infrastructure. This includes system integration, certification, repair and maintenance, spare-parts networks, RaaS, insurance, financing, secondary markets, SPVs, closed-end funds, DAOs, tokenized ownership, and other ownership instruments. Maquina and Robo Strategy both sit in this layer, but the underlying risks they bear come from robot-body platforms, software brains, supply chains, and real deployment data.

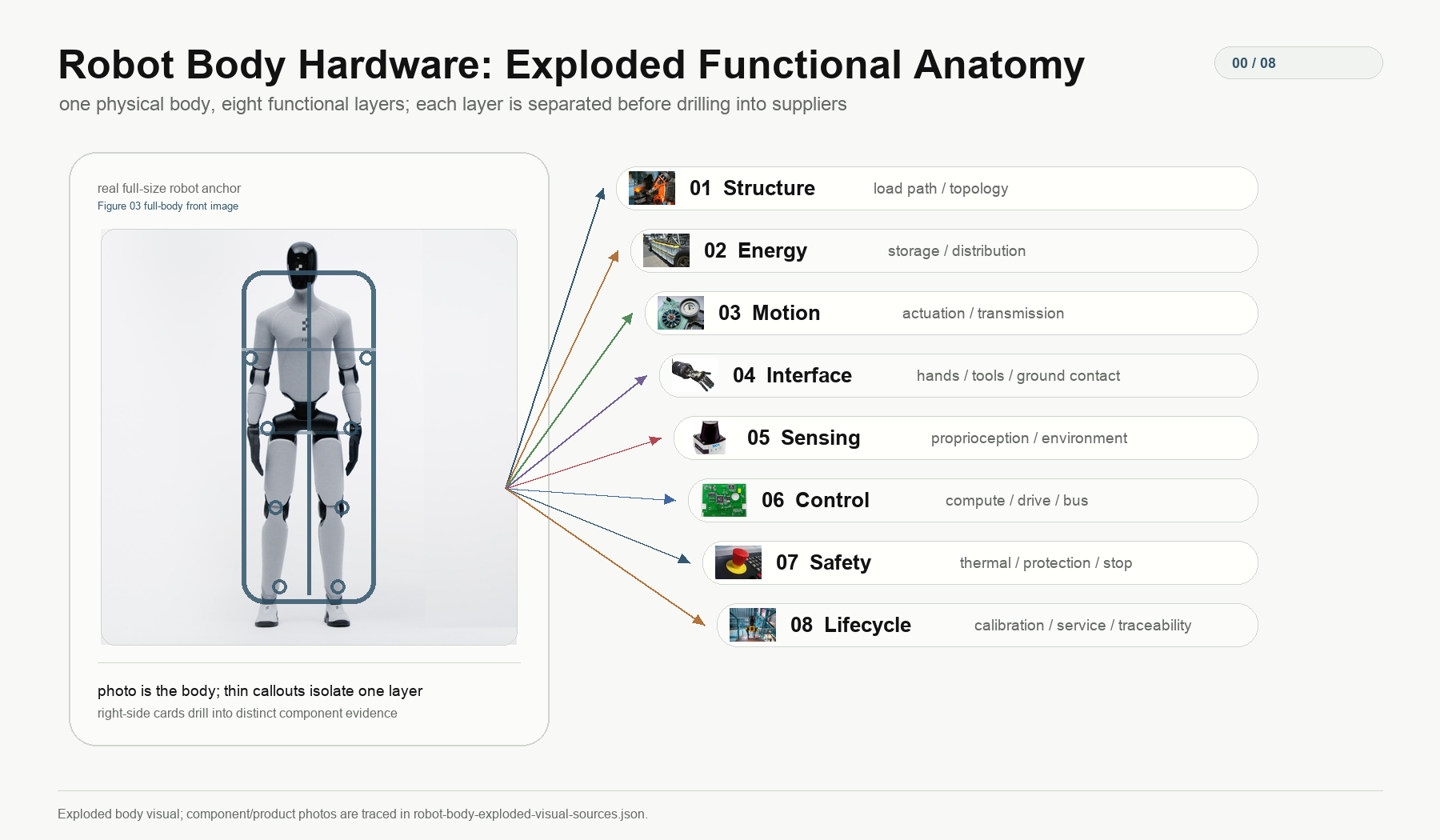

Decomposing a Robot Body

Robot-body decomposition cannot start from "what forms do robots have," and it also cannot mix actuators, motors, reducers, drives, joints, and grippers into the same layer. Industry-chain and BOM views can place these parts side by side because they map to different suppliers. But a first-principles body tree must drill down layer by layer according to the physical causal chain: carrying loads -> storing and distributing energy -> converting energy into controlled force/motion -> transmitting and constraining motion -> coupling with the environment to do work -> measuring state -> real-time closed loop -> heat dissipation, protection, manufacturing, and maintenance.

This section decomposes only "robot-body hardware." It does not put task scenarios, robot categories, software brains, cloud data closed loops, and capital infrastructure into the same tree. The validation rules are as follows:

- The same layer is split only by the same dimension. The first layer is split by physical function, the second by subfunction, the third by implementation principle, and only then down to parts and supply-chain categories.

- Parent-child relationships must be "functional requirement -> implementation path -> mechanism principle -> parts," not a "popular parts list."

- A part should be placed only under the closest functional node. If a reducer is packaged inside a joint/servo actuator, it belongs under the torque/speed matching mechanism inside the actuator; if it is a remote independent transmission gearbox, it belongs under output transmission.

- Robot forms do not enter the body tree. Humanoids, quadrupeds, AMRs, robotic arms, drones, and surgical robots are combinations of this tree in different task environments.

- Software brains do not enter the body-hardware tree. Main-control boards, real-time controllers, servo drives, and communication buses belong to body hardware; VLA/VLM, simulation, fleet learning, and task planning belong to the software stack and brain-model layer in the previous industry-chain section.

- Cross-layer subsystems should not be forced into a single node. Dexterous hands, mobile chassis, robotic arms, and surgical instrument arms can all be discussed as products or modules. But in the body tree, they should be decomposed back into structure, motion generation, environment coupling, perception, control electronics, thermal safety, and maintenance interfaces.

Under these principles, a robot body should be directly split into eight physical-function sections: structural load-bearing and kinematic topology, energy storage and power distribution, motion generation and transmission, environment coupling and work interfaces, perception and measurement, control/drive and communication electronics, thermal management/protection and functional safety, and manufacturing/calibration and maintenance interfaces. They are expanded layer by layer below.

Illustration: overview of a first-principles robot-body decomposition. The left side uses a real full-body front-view product image of Figure 03 collected from the web as the parent anchor for the same robot; the right side extracts the eight physical-function layers one by one. Each subsequent layer has its own image with corresponding real component photos.

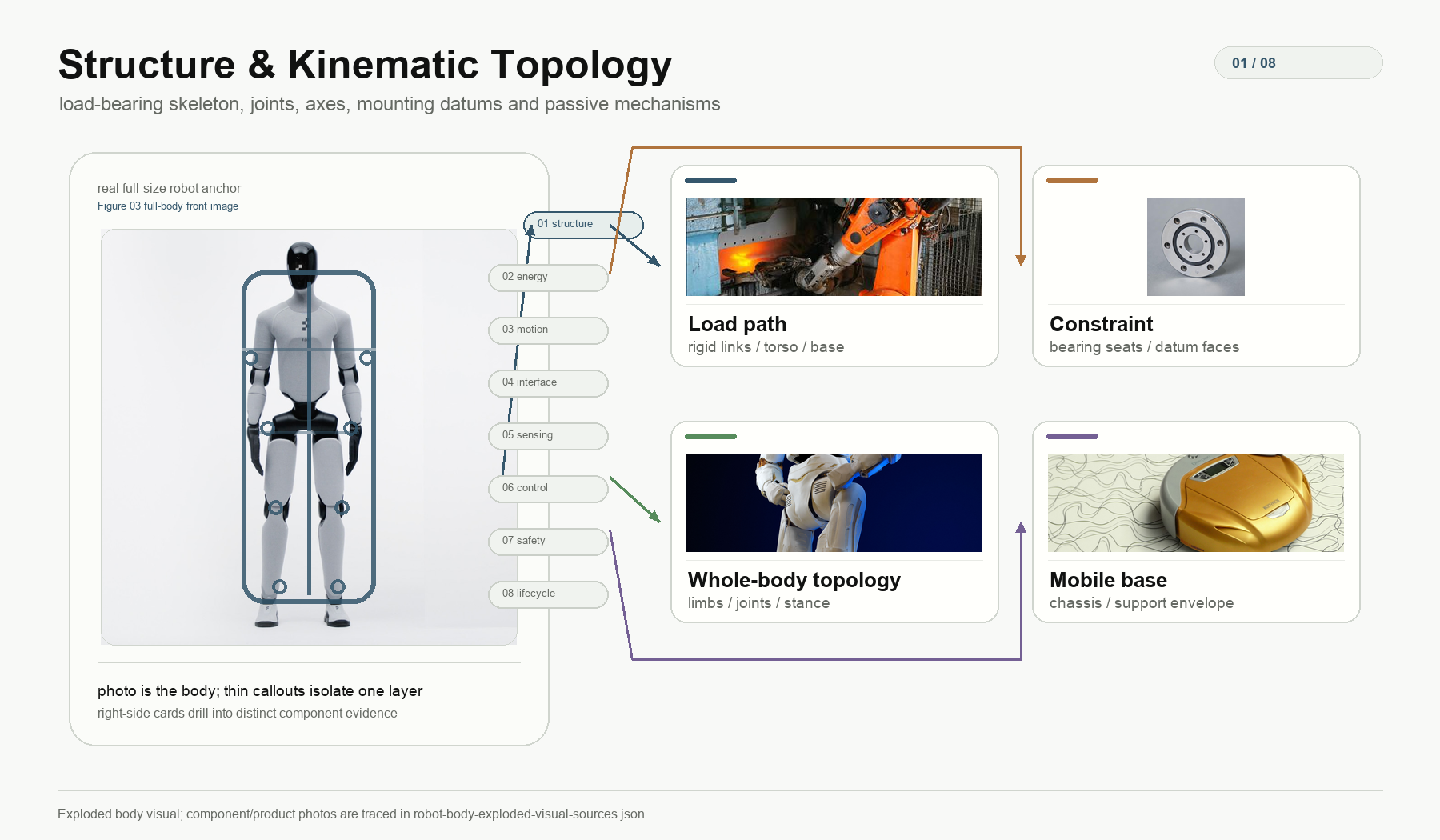

Structural Load-Bearing and Kinematic Topology

This layer answers how the robot maintains its shape, bears loads, defines degrees of freedom, and defines its range of motion. Parts that actively generate force do not belong here; motors, hydraulic cylinders, and pneumatic cylinders belong to motion generation and transmission. A reasonable decomposition is:

Illustration: single-layer decomposition of structural load-bearing and kinematic topology. The parent robot highlights only load-bearing paths, joint constraints, and topology datums, while the right side uses photos of a load-bearing robotic arm, bearings, whole-machine topology, and a mobile chassis to correspond to structural-layer subfunctions.

Structural Load-Bearing and Kinematic Topology

├─ Load path: torso, chassis, links, supports, load-bearing shells

├─ Degree-of-freedom topology: joint axes, motion chains, serial/parallel structures, mobile-chassis topology

├─ Mounting and positioning: joint seats, bearing seats, mounting surfaces, positioning datums, flange interfaces

├─ Hand/end structure: metacarpals, phalanges, finger joints, palm, end shells

├─ Passive mechanisms: springs, counterweights, compliant elements, limiters, damping and buffering structures

└─ Packaging and maintainability: shells, harness channels, quick-release structures, service openings

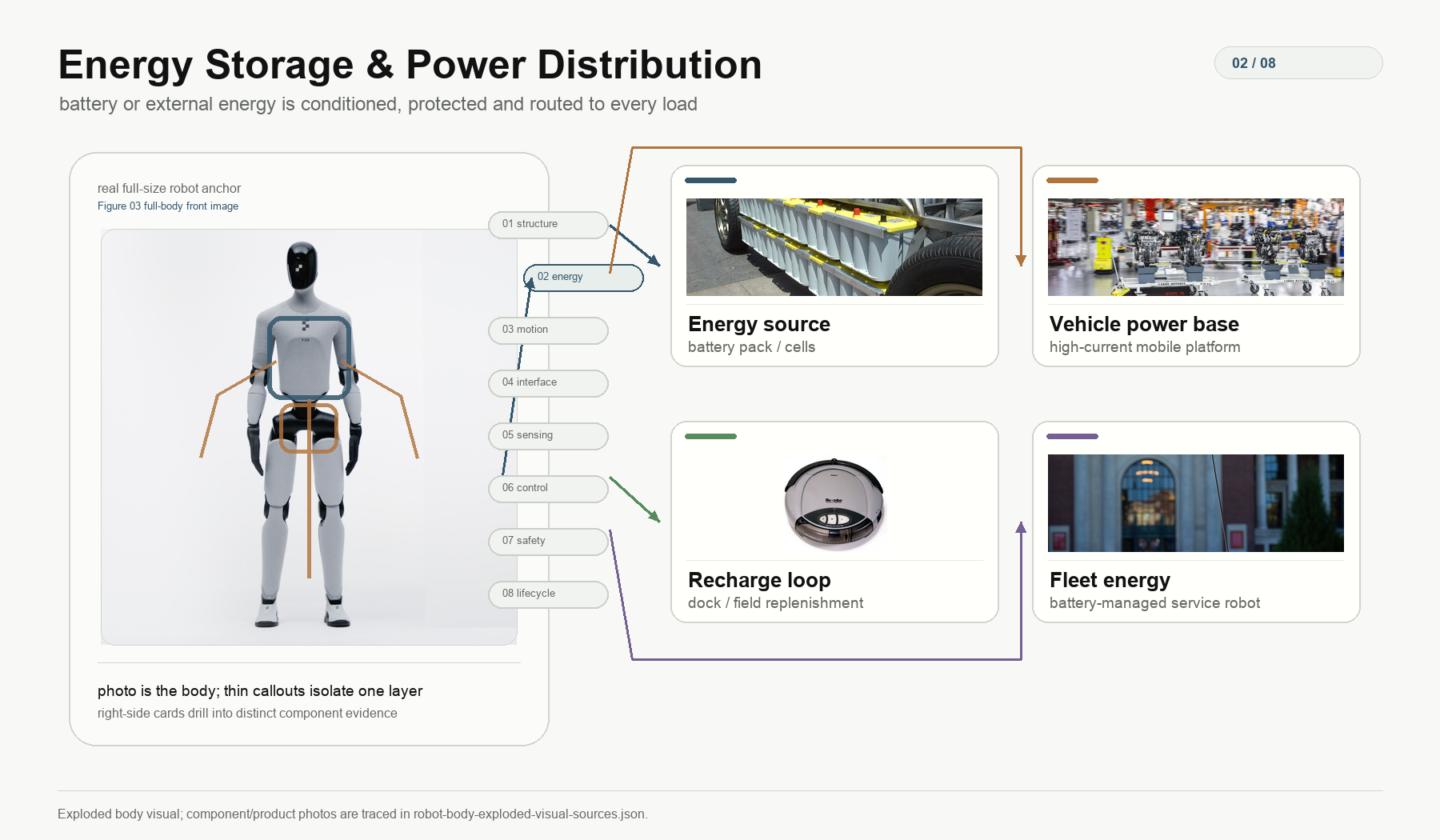

Energy Storage and Power Distribution

This layer answers where energy comes from and how it is safely delivered to execution, computing, and perception units. Servo drives and motor-control power stages belong to control, drive, and communication electronics. Battery-pack thermal dissipation can be marked under thermal management, but the battery pack mainly belongs to the energy layer.

Illustration: single-layer decomposition of energy storage and power distribution. The parent robot highlights only batteries, power paths, and replenishment direction, while the right side uses photos of battery packs, high-power AGV chassis, recharging robots, and delivery robots to show different implementations of the energy layer.

Energy Storage and Power Distribution

├─ Energy sources: battery pack, external power, pneumatic source, hydraulic source, fuel/generation unit

├─ Energy conditioning: BMS, DC/DC, PDU, contactors, fuses and protection devices

├─ Energy distribution: wire harnesses, connectors, busbars, slip rings, air tubes, hydraulic lines

├─ Replenishment systems: charging dock, automatic recharging, battery-swap interface, battery quick release

└─ Energy safety: isolation, overcurrent/overvoltage protection, thermal-runaway protection, pressure relief and power-cut strategy

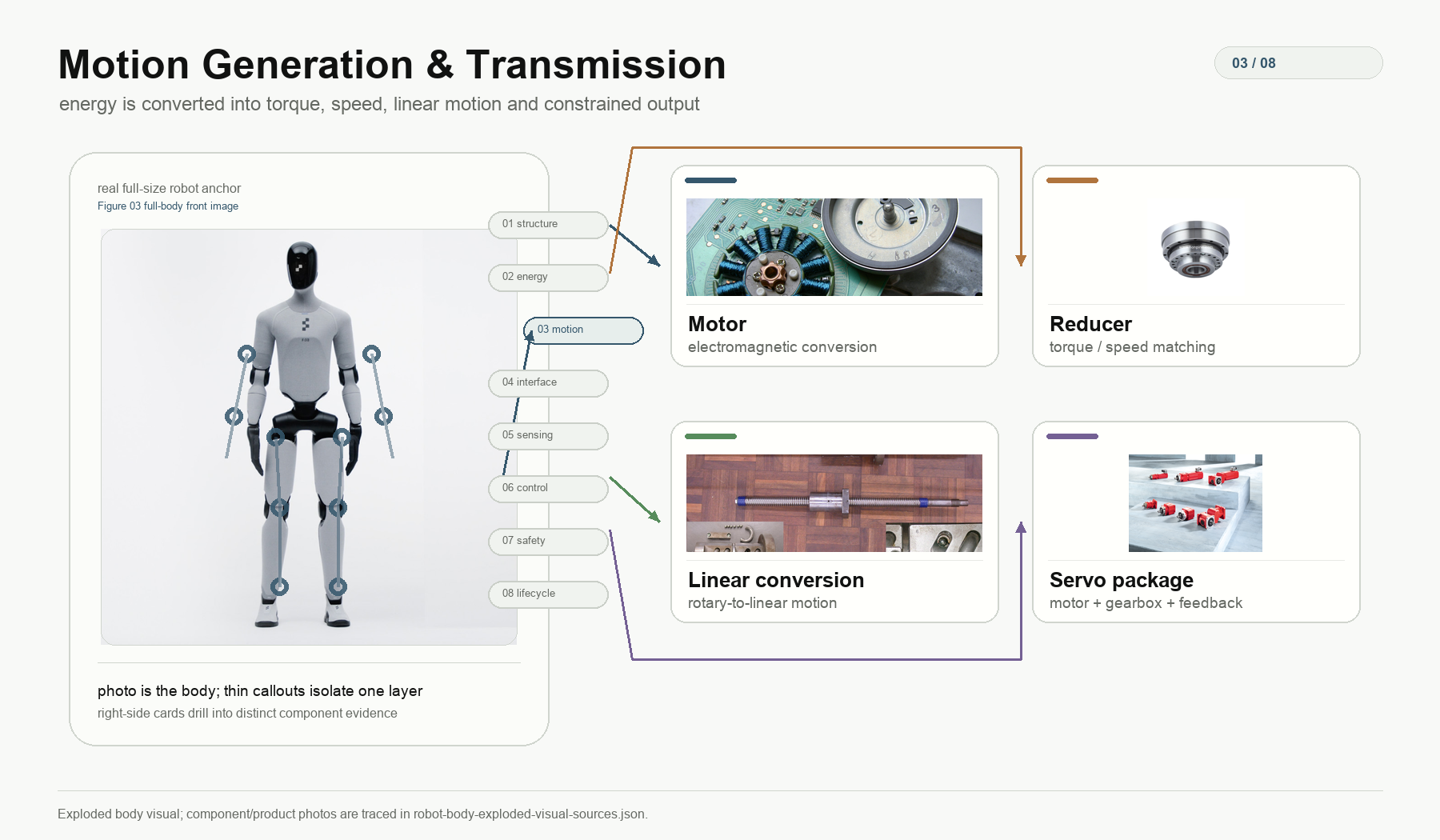

Motion Generation and Transmission

This layer answers how energy becomes controllable force, torque, speed, displacement, and posture. It is the center of the body-hardware tree and is also the easiest part to decompose incorrectly. The first drill-down for actuators is not "motor, reducer, encoder"; it should first split by output-motion form into rotary actuators and linear actuators, then drill down by energy-conversion method and internal mechanism to parts.

Illustration: single-layer decomposition of motion generation and transmission. The parent robot highlights only joints, output chains, and motion constraints, while the right side uses photos of motors, reducers, screws, and servo modules to correspond to energy conversion, torque/speed matching, rotary-to-linear conversion, and integrated actuators.

Motion Generation and Transmission

├─ Actuators: convert electrical/hydraulic/pneumatic energy into mechanical output

│ ├─ Rotary actuators

│ │ ├─ Motor-type rotary actuators

│ │ │ ├─ Energy conversion: BLDC motor, torque motor, servo motor, stepper motor

│ │ │ ├─ Torque/speed matching: direct drive, quasi-direct drive, harmonic reducer, planetary reducer, cycloidal/RV reducer, gear set, worm gear

│ │ │ ├─ State feedback: encoder, resolver, Hall, current/temperature, torque sensor

│ │ │ ├─ Holding and power-off safety: brake, clutch, locking mechanism

│ │ │ └─ Support packaging: bearings, seals, housing, thermal path, cable outlet structure

│ │ ├─ Hydraulic rotary actuators: hydraulic motor, swing cylinder, valve control, sealing and pressure feedback

│ │ └─ Pneumatic rotary actuators: pneumatic motor, rotary cylinder, valve island and position feedback

│ ├─ Linear actuators

│ │ ├─ Motor-driven linear actuators

│ │ │ ├─ Energy conversion: rotary motor or linear motor

│ │ │ ├─ Rotary-to-linear conversion: ball screw, roller screw, trapezoidal screw, rack and pinion, timing belt, cable/tendon, linkage/cam

│ │ │ ├─ Guidance and load-bearing: guide rail, slider, spline, support bearing

│ │ │ ├─ State feedback: position scale, encoder, force sensor, limit switch

│ │ │ └─ Holding and packaging: brake, mechanical limit, housing, sealing, drag chain/cable outlet

│ │ ├─ Hydraulic cylinder: cylinder body, piston rod, valve, pump/accumulator, pressure/position feedback

│ │ ├─ Pneumatic cylinder: cylinder body, piston rod, valve island, buffering and magnetic switch

│ │ └─ Linear motor: stator, mover, magnetic track, linear guide and position feedback

│ └─ Flexible/soft/special actuators

│ ├─ Tendon/cable drive

│ ├─ Series elastic actuator / variable-stiffness actuator

│ ├─ Shape-memory alloy, piezoelectric, electroactive polymer

│ └─ Pneumatic artificial muscle, soft chamber, fluid-elastic structure

├─ Output transmission and motion constraints: transmit actuator output to the target degree of freedom

│ ├─ Shafts, couplings, timing belts, chains, gears, differentials

│ ├─ Linkages, four-bars, parallel mechanisms, cable/tendon paths, underactuated mechanisms

│ ├─ Bearings, guide rails, sliders, splines, limiters and stops

│ └─ Springs, compliant elements, damping elements, backlash compensation and preload structures

└─ Joint and module packaging: package actuators and transmission constraints into assemblable units

├─ Integrated joint modules

├─ Hub/wheel-leg modules, ankle/knee/hip/shoulder/elbow/wrist modules

├─ Finger/wrist/gripper/dexterous-hand drive modules

└─ Quick release, sealing, thermal dissipation, harnesses and repair structures

The position of reducers is determined by function, not by supplier name. In robot joints, harmonic, planetary, cycloidal/RV and similar reducers are usually torque/speed matching mechanisms in motor-type rotary actuators, so their upward path is "Motion Generation and Transmission -> Actuators -> Rotary Actuators -> Motor-Type Rotary Actuators -> Torque/Speed Matching." Ball screws, roller screws, racks and pinions, timing belts, and tendons are rotary-to-linear conversion or output-transmission mechanisms inside linear actuators. Only when a gearbox is not part of the actuator internally but is a transmission box located away from the motor and separately connected to the load should it be placed under output transmission and motion constraints.

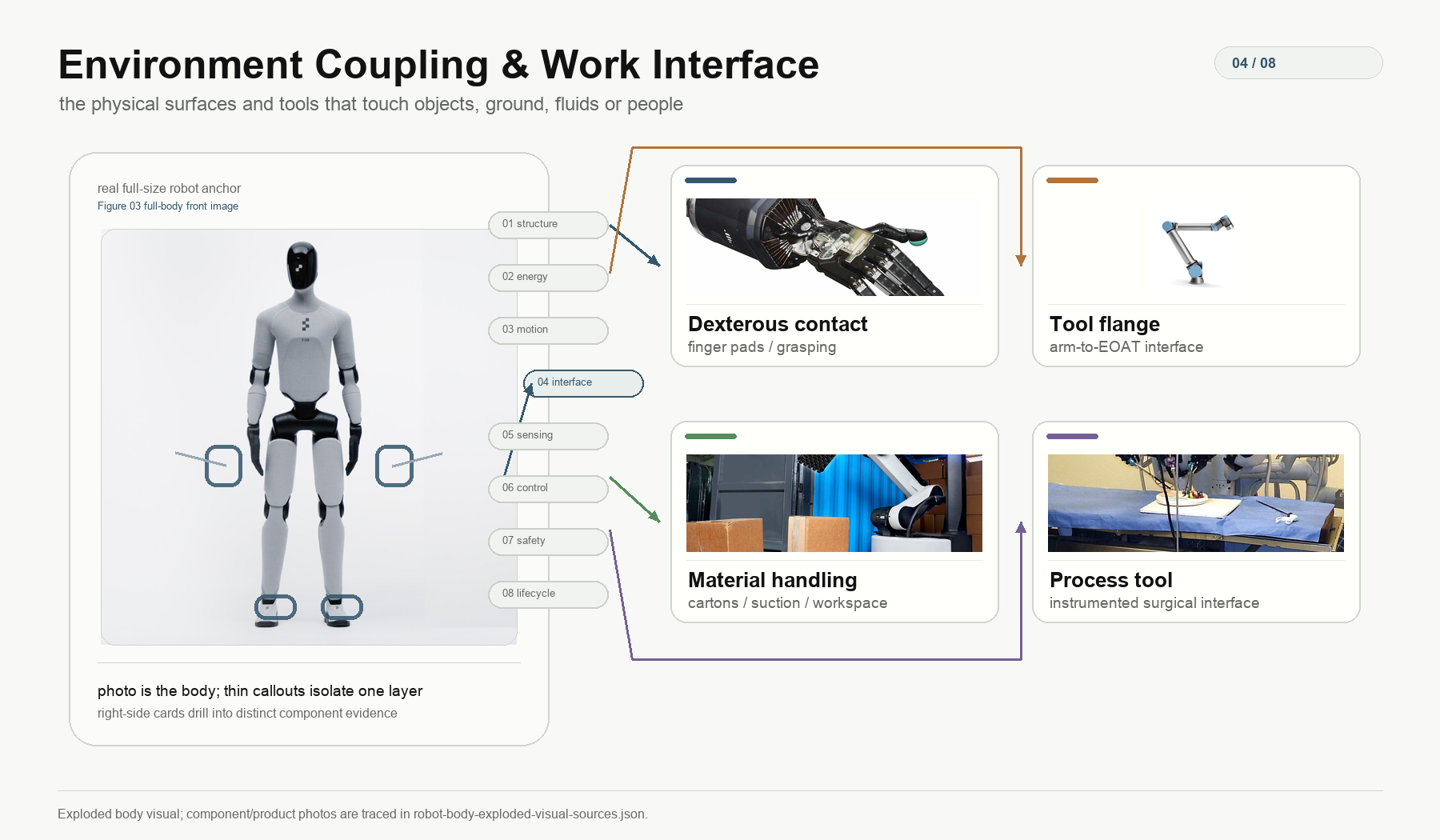

Environment Coupling and Work Interfaces

This layer answers through what interface the robot applies mechanical work to the environment. What belongs here are "external contact and work interfaces," not the full internal composition of a dexterous hand. In industry product terminology, a complete dexterous hand is often classified together with grippers, EOAT, and end effectors. But when decomposing the body by first principles, a dexterous hand is not a single environment-coupling node; it is a composite subsystem spanning structure, motion generation, contact interface, perception, control electronics, and maintenance interfaces.

Illustration: single-layer decomposition of environment coupling and work interfaces. The parent robot highlights only hands, feet, and outward-facing contact interfaces, while the right side uses photos of dexterous hands, tool flanges, mobile manipulation platforms, and surgical tools to distinguish contact, gripping, handling, and process tools.

Environment Coupling and Work Interfaces

├─ Mobile contact interfaces: wheels, feet, tracks, propellers, thrusters, tires, control surfaces

├─ Simple end effectors: grippers, suction cups, magnetic grippers, hooks, tray/cargo-bin interfaces

├─ Dexterous manipulation contact interfaces: fingertips, skin, friction materials, nails/hard contact surfaces, palm contact

├─ Tool/object interaction interfaces: grasping, pinching, twisting, insertion/removal, tool holding and human contact

├─ Process tools: welding torch, spray head, cutter, surgical instrument, cleaning/polishing tool

└─ Quick-change and tool interfaces: flange, tool changer, tool identification, pneumatic/electrical/hydraulic interfaces

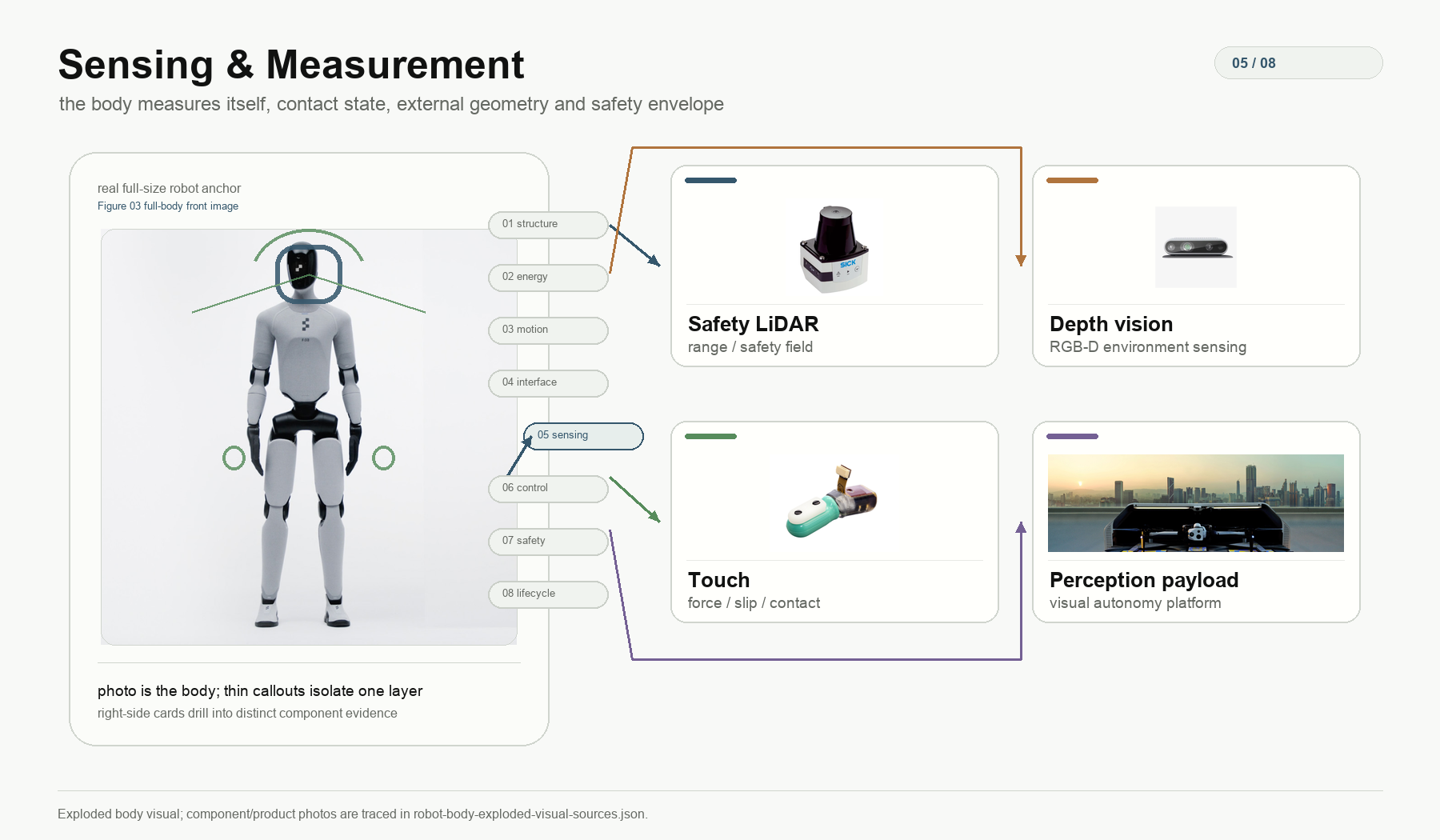

Perception and Measurement

This layer answers how the body measures itself, contact state, environment state, and safety boundaries. Perception algorithms do not belong here; sensor hardware, synchronization triggers, calibration parts, and safety scanners do.

Illustration: single-layer decomposition of perception and measurement. The parent robot highlights only head vision, hand/contact, and external perception boundaries, while the right side uses photos of safety LiDAR, depth cameras, tactile sensing, and vision-autonomy payloads to correspond to different measurement channels.

Perception and Measurement

├─ Proprioception: encoder, IMU, current, voltage, temperature, joint torque

├─ Contact sensing: tactile sensing, foot-end contact, end force/torque, pressure array, slip and contact detection

├─ Environment perception: RGB camera, depth camera, LiDAR, millimeter wave, ultrasound, microphone

├─ Safety perception: safety radar, safety light curtain, collision detection, proximity detection

└─ Calibration synchronization: time synchronization, trigger, calibration parts, sensor extrinsic-reference datum

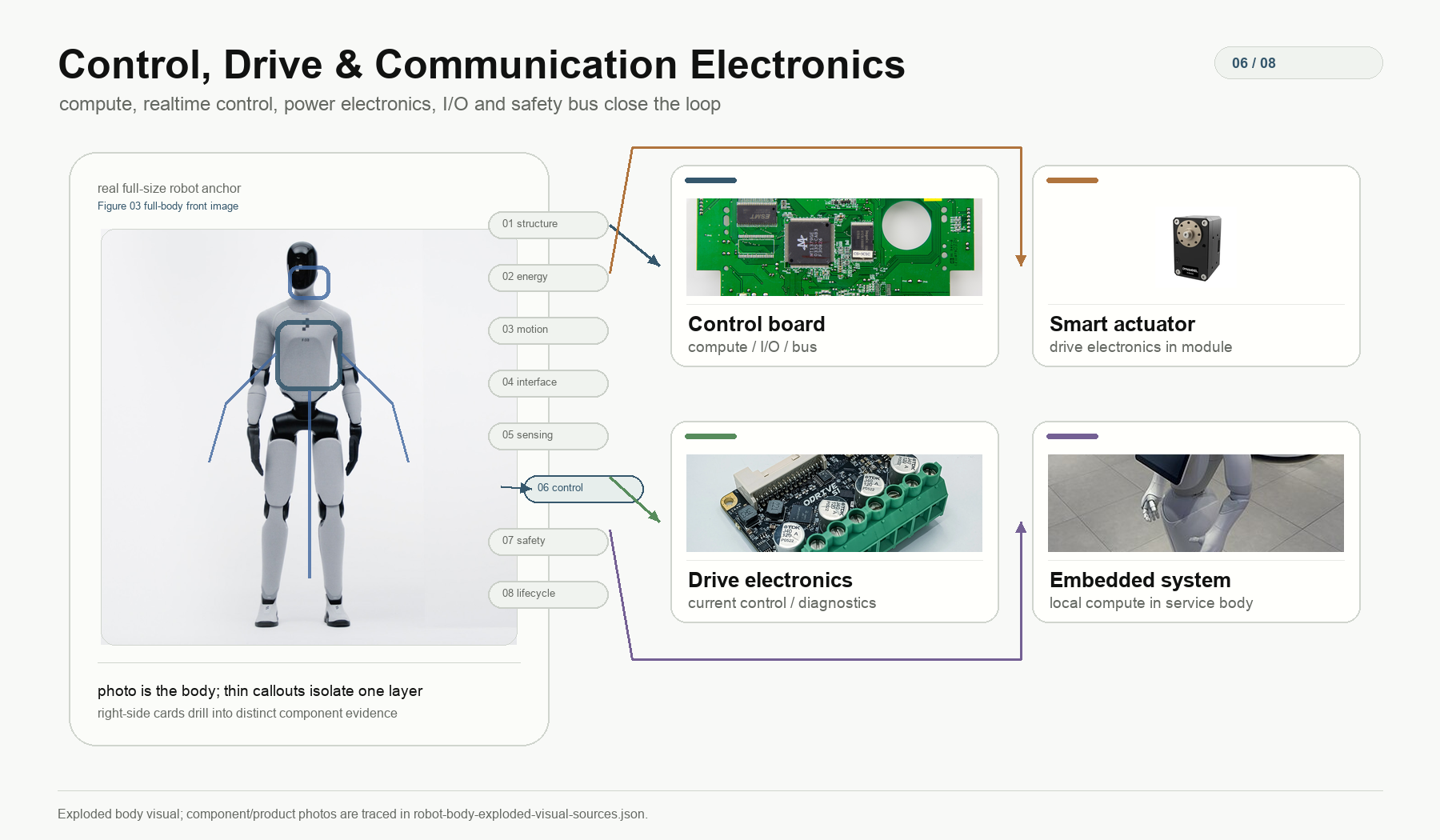

Control, Drive, and Communication Electronics

This layer answers how the body turns computation results into real-time current, valve control, braking, and safety actions. High-level software belongs to the software stack. Drives serve actuators, but functionally they belong to control and power electronics.

Control, Drive, and Communication Electronics

├─ Main computing: CPU, GPU, edge-computing module, AI accelerator

├─ Real-time control: MCU, motion controller, real-time control board, hand local closed loop, clock synchronization

├─ Actuation drive: servo drive, motor inverter, valve-control unit, brake control

├─ Communication buses: EtherCAT, CAN, Ethernet, serial bus, wireless connection

├─ I/O and diagnostics: sensor interfaces, logs, debug ports, status monitoring

└─ Safety control: safety PLC, emergency-stop loop, redundant control, fault-degradation control

Illustration: single-layer decomposition of control, drive, and communication electronics. The parent robot highlights only main control, torso controllers, drive wiring, and local closed loops, while the right side uses photos of control boards, smart actuators, ODrive S1 drives, and embedded systems in service robots to distinguish computing, drive, and communication hardware.

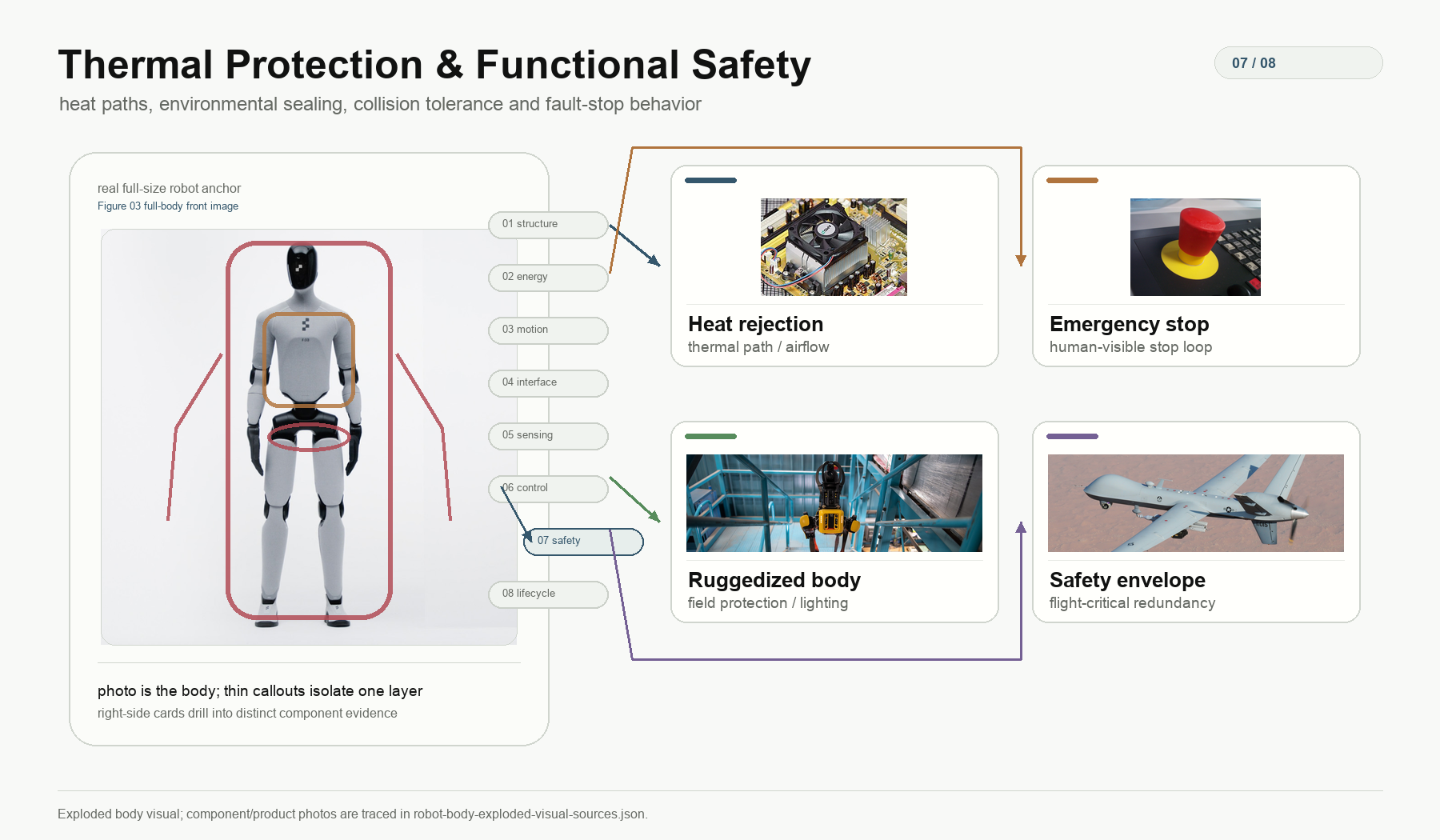

Thermal Management, Protection, and Functional Safety

This layer answers how the body keeps working under heat, dust, water, impact, EMI, and faults. Brakes, as internal holding parts inside actuators, can belong to motion generation and transmission. System-level emergency stops, safety loops, and fault degradation belong here or under control electronics.

Thermal Management, Protection, and Functional Safety

├─ Thermal path: heat source, thermal-conductive material, heat sink, air cooling, liquid cooling, thermal isolation

├─ Environmental protection: dustproofing, waterproofing, sealing, corrosion resistance, cleaning/disinfection resistance

├─ Impact protection: falling, collision, buffering, shell energy absorption, joint/finger protection

├─ Electrical protection: EMI, ESD, overcurrent, overvoltage, insulation, grounding

└─ Functional safety: emergency stop, braking, redundancy, speed/force limitation, pinch protection, fault degradation

Illustration: single-layer decomposition of thermal management, protection, and functional safety. The parent robot highlights only shell coverage, thermal/safety boundaries, and system-level protection paths, while the right side uses photos of thermal dissipation, emergency stops, reinforced bodies, and flight redundancy to correspond to different safety implementations.

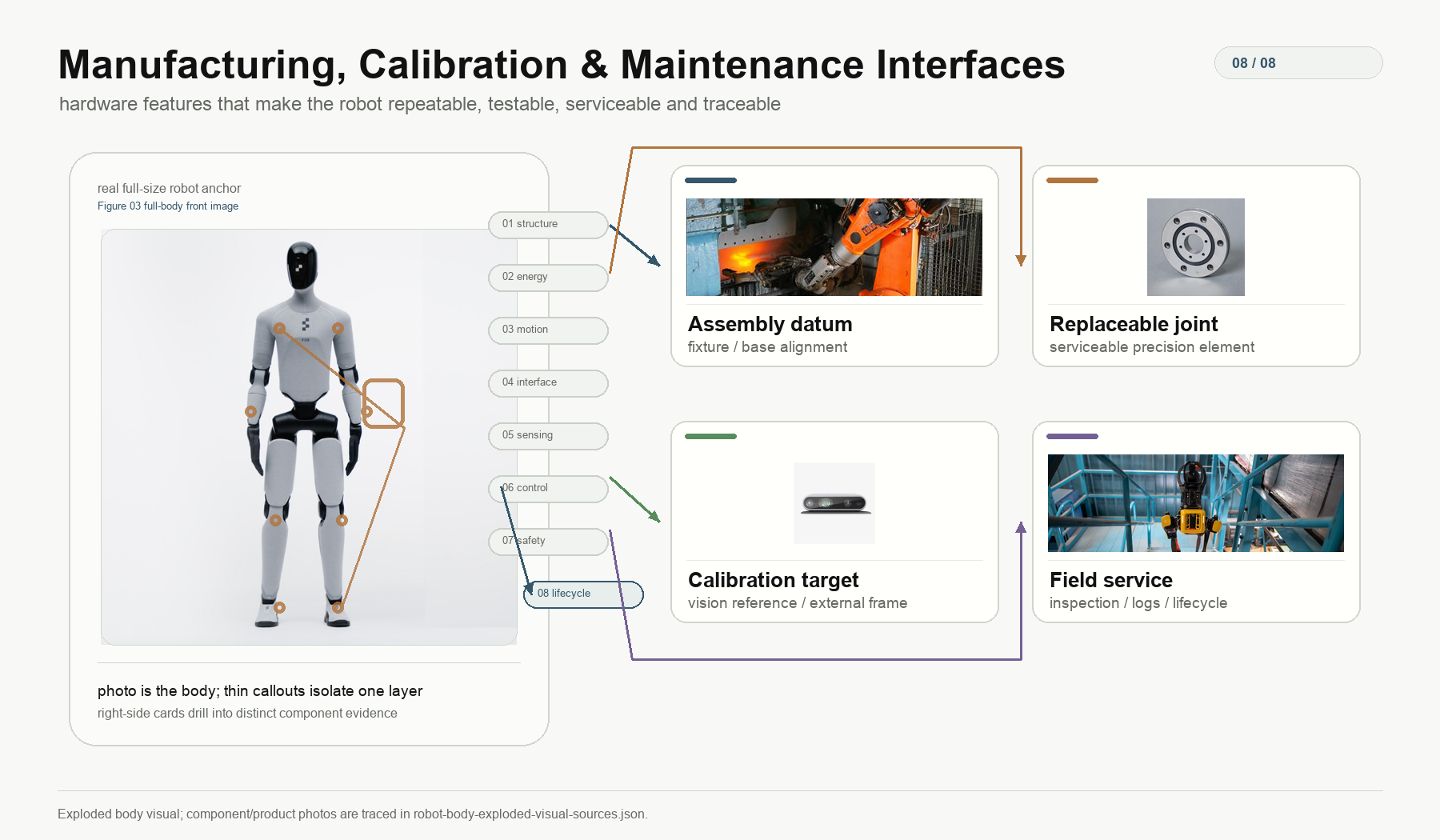

Manufacturing, Calibration, and Maintenance Interfaces

This layer answers how the body becomes a reproducible, repairable, traceable asset from a prototype. Contract manufacturers and repair-service providers belong to the manufacturing/deployment layer of the industry chain. Here, the reference is to hardware interfaces reserved on the body for manufacturing, calibration, and maintenance.

Manufacturing, Calibration, and Maintenance Interfaces

├─ Assembly datums: locating pins, assembly surfaces, fixture interfaces, assembly-sequence design

├─ Calibration interfaces: camera calibration, torque calibration, joint zero position, tactile calibration, tendon-tension calibration

├─ Final-test interfaces: test points, flashing ports, burn-in tests, EOL functional tests

├─ Maintenance interfaces: module quick release, spare-part compatibility, service passages, fingertip/skin replacement parts, field-replacement parts

└─ Traceability system: serial numbers, logs, part-lifetime records, maintenance records

Illustration: single-layer decomposition of manufacturing, calibration, and maintenance interfaces. The parent robot highlights only assembly datums, replaceable nodes, and maintenance paths, while the right side uses photos of assembly robots, bearings, calibration sensors, and field-service robots to correspond to hardware interfaces from prototype to reproducible asset.

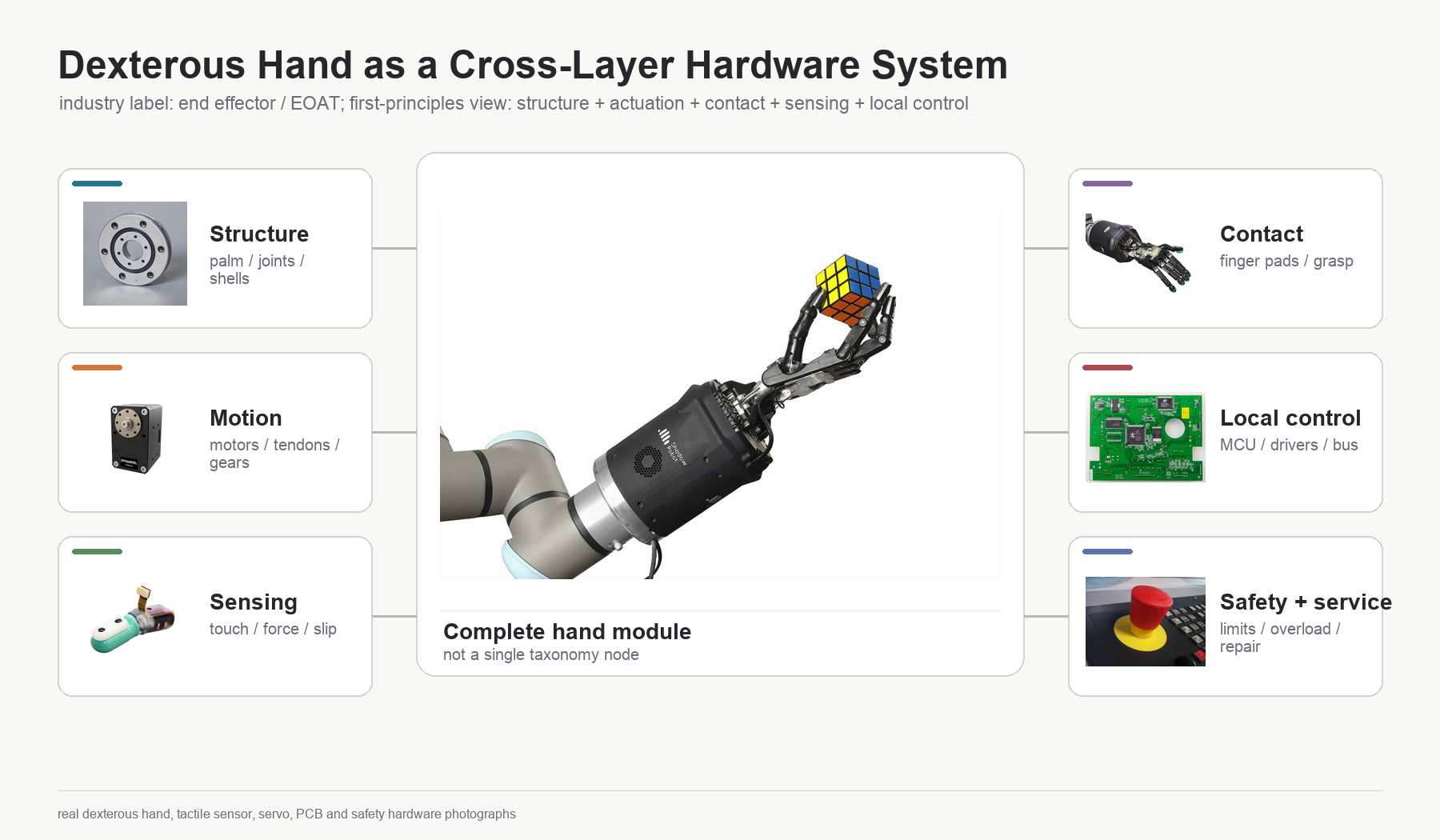

Dexterous Hands as a Cross-Layer Subsystem

Therefore, the most robust way to handle dexterous hands is a "dual lens." In industry/product classification, they can be called end effectors or EOAT because they are installed at the wrist end of robotic arms or humanoid robots and directly handle grasping and manipulation. But in the body-hardware tree, they must be decomposed into a cross-layer view and cannot be placed alone into any single physical-function section.

Dexterous Hand System (Cross-Layer View)

├─ Structural load-bearing and kinematic topology: metacarpals, phalanges, joints, palm, shell, finger-degree-of-freedom topology

├─ Motion generation and transmission: micro motors, tendons, gears, linkages, differentials, underactuation, elastic elements

├─ Environment coupling and work interfaces: fingertips, skin, friction materials, hard contact surfaces, tool-holding geometry

├─ Perception and measurement: tactile sensing, force sensing, joint position, temperature, slip, contact detection

├─ Control, drive, and communication electronics: MCU, drive board, sensor interfaces, communication, local closed loop

├─ Thermal management, protection, and functional safety: finger overload, pinch protection, temperature rise, skin/shell durability

└─ Manufacturing, calibration, and maintenance interfaces: fingertip replacement, tendon tension, tactile calibration, lifetime records

With this treatment, gripper/EOAT companies such as SCHUNK, Robotiq, and OnRobot can be classified as end-effectors in product taxonomy. The hand systems of Shadow Robot, Allegro Hand, qb SoftHand, Tesla / Figure / 1X, however, are restored as cross-layer hardware systems in body decomposition. When researching the supply chain, the question is not only "does this company make actuators," but also whether it controls hand motion generation, tactile sensing, contact materials, local control electronics, or a complete hand module.

Illustration: dexterous hands are cross-layer subsystems. Product terminology can call them end effectors or EOAT, but body decomposition must split them back into structure, motion generation, contact interface, perception, local control, safety durability, and maintenance interfaces.

This body tree does not overturn the research department's existing robotics-sector taxonomy. The research department's sector taxonomy solves "how should companies/product lines be classified": hardware subsystems, software intelligence, whole-machine systems, manufacturing validation, deployment operations, demand scenarios, and capital infrastructure. Body decomposition solves "how a robot is internally decomposed." It should be used as a hardware due-diligence base map: to penetrate where maxon, Harmonic Drive, Nabtesco, SICK, SCHUNK, HIWIN, and Jabil each sit in the body nodes; to analyze which layers Figure, Apptronik, Agility, and 1X self-develop and which layers they procure externally; to identify missing targets in actuators, dexterous hands, tactile sensing, safety, thermal management, manufacturing calibration, and so on; and to avoid misclassifying dexterous-hand companies as humanoid-robot companies.

Therefore, a first-principles body decomposition is not a supplier list, but a physical hierarchy tree. Supply-chain analysis can compare Harmonic Drive, Nabtesco, maxon, HIWIN, SICK, Jabil and other companies side by side. But in the body tree, they sit in different functional nodes such as reducer inside actuator, motion conversion/guidance, perception and measurement, and manufacturing/maintenance. Only by first decomposing this tree correctly can the later coverage rate, missing targets, and penetration of European and U.S. supply chains avoid misalignment.

The sources of the real product photos used in body-decomposition illustrations are listed in robot-body-exploded-visual-sources.json.

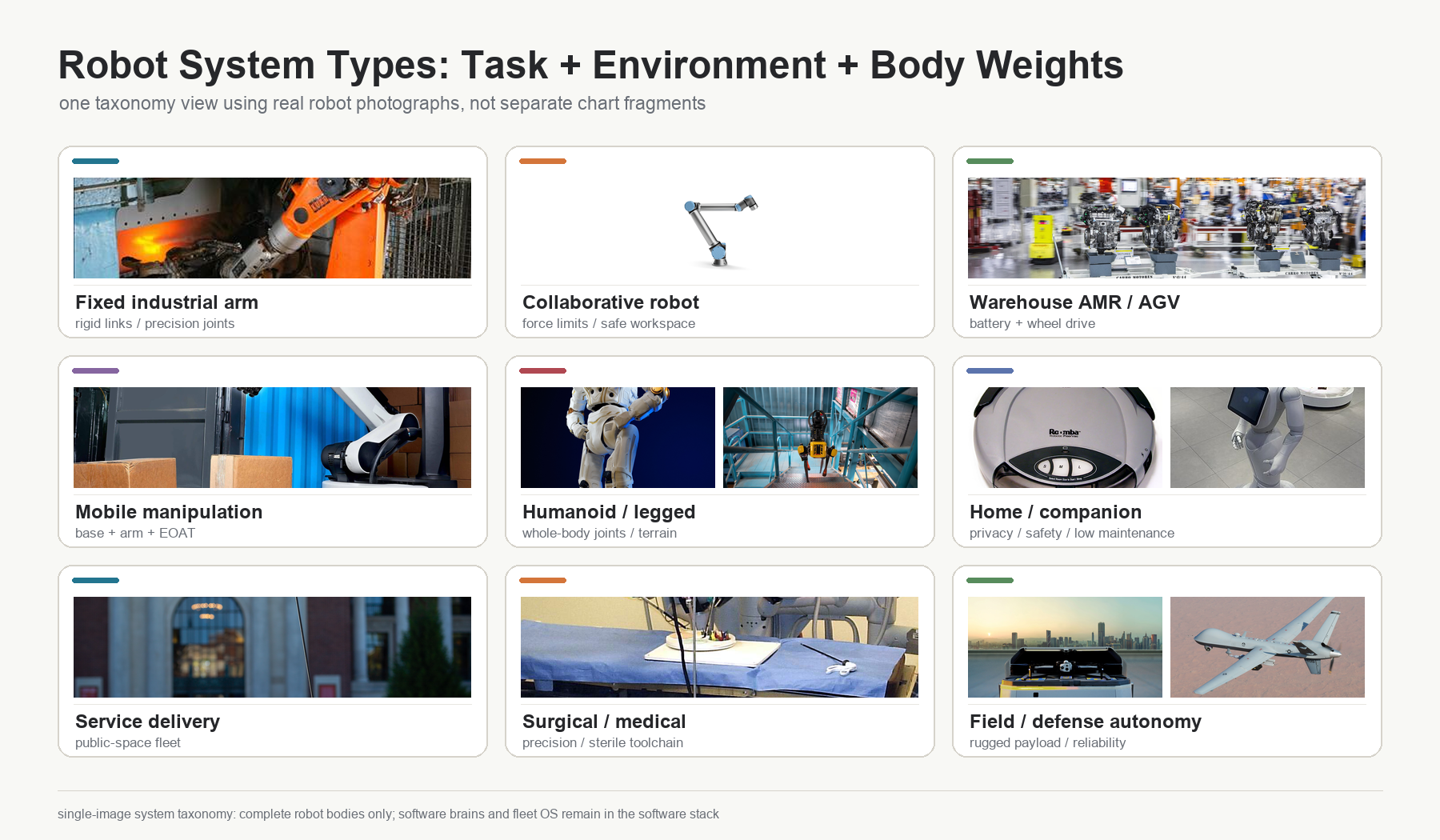

Robot Classification: Re-Examining Types by Complete Robot Systems

After body decomposition, robot classification becomes clearer: different categories are essentially different combinations of tasks, environments, actuators, modes of mobility, work interfaces, and regulatory constraints. This section classifies only complete robot bodies or platforms. It does not list robot foundation models, software brains, simulation, robot operating systems, or fleet OS as robot types; those belong to the software stack and brain-model layer in the industry chain.

Fixed industrial robots are the most mature robot bodies, mainly used for welding, handling, spraying, palletizing, machine tending, and precision assembly. Core players include FANUC, ABB Robotics, Yaskawa, Kawasaki, Mitsubishi, and KUKA.

Collaborative robots target more flexible automation in small and medium factories. Core players include Universal Robots, Doosan Robotics, FANUC CRX, ABB GoFa, and Standard Bots.

Warehouse automation and mobile robots target goods-to-person, whole-warehouse scheduling, picking, sorting, and handling. Core players include Symbotic, AutoStore, MiR, Locus Robotics, and Exotec.

Mobile manipulators combine a mobile chassis, robotic arm, and end effector, targeting warehousing, retail, laboratories, and light manufacturing. Dyna, Dexmate, Boston Dynamics Stretch, and Toyota Research's mobile manipulation direction are key observation targets.

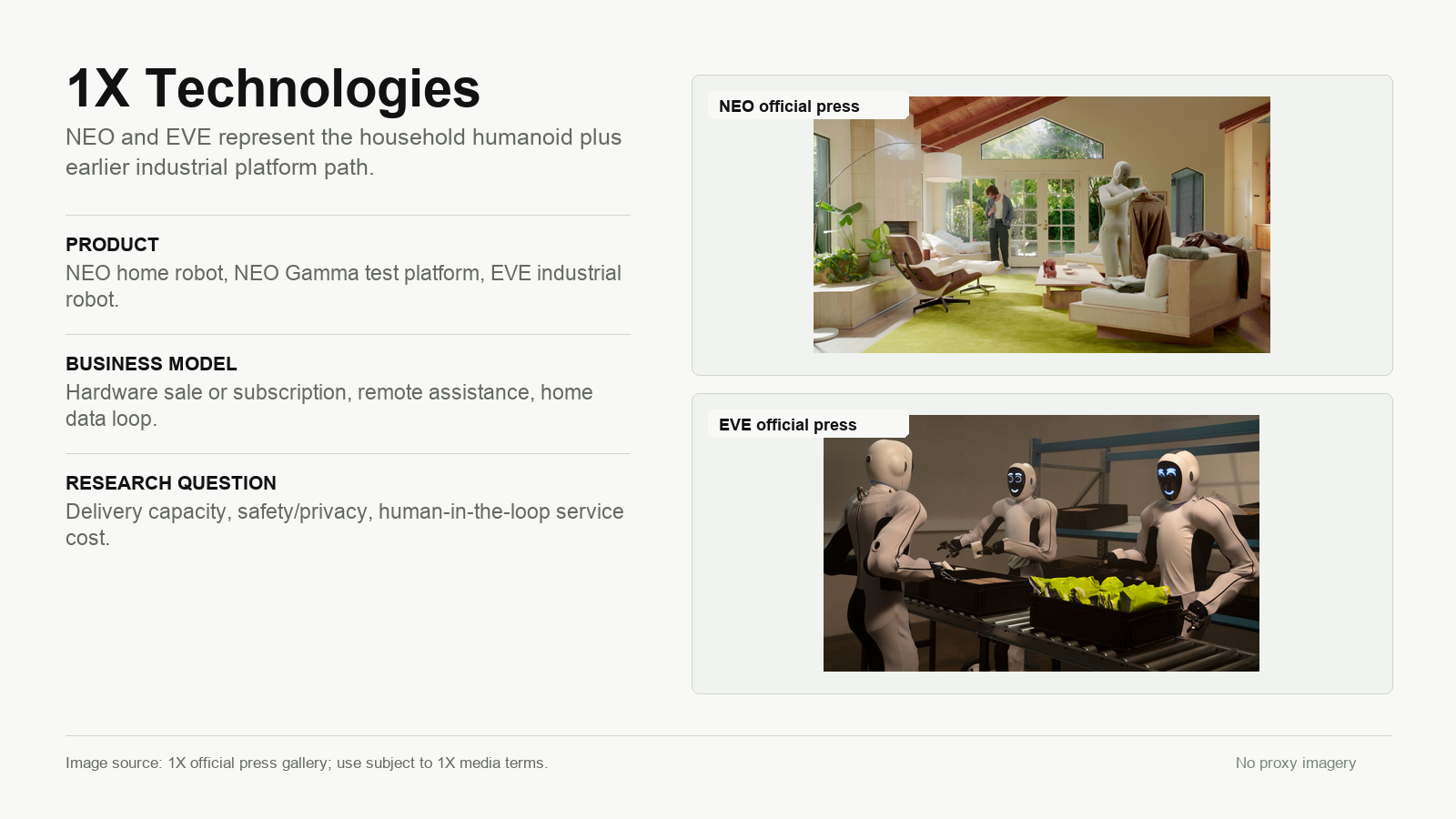

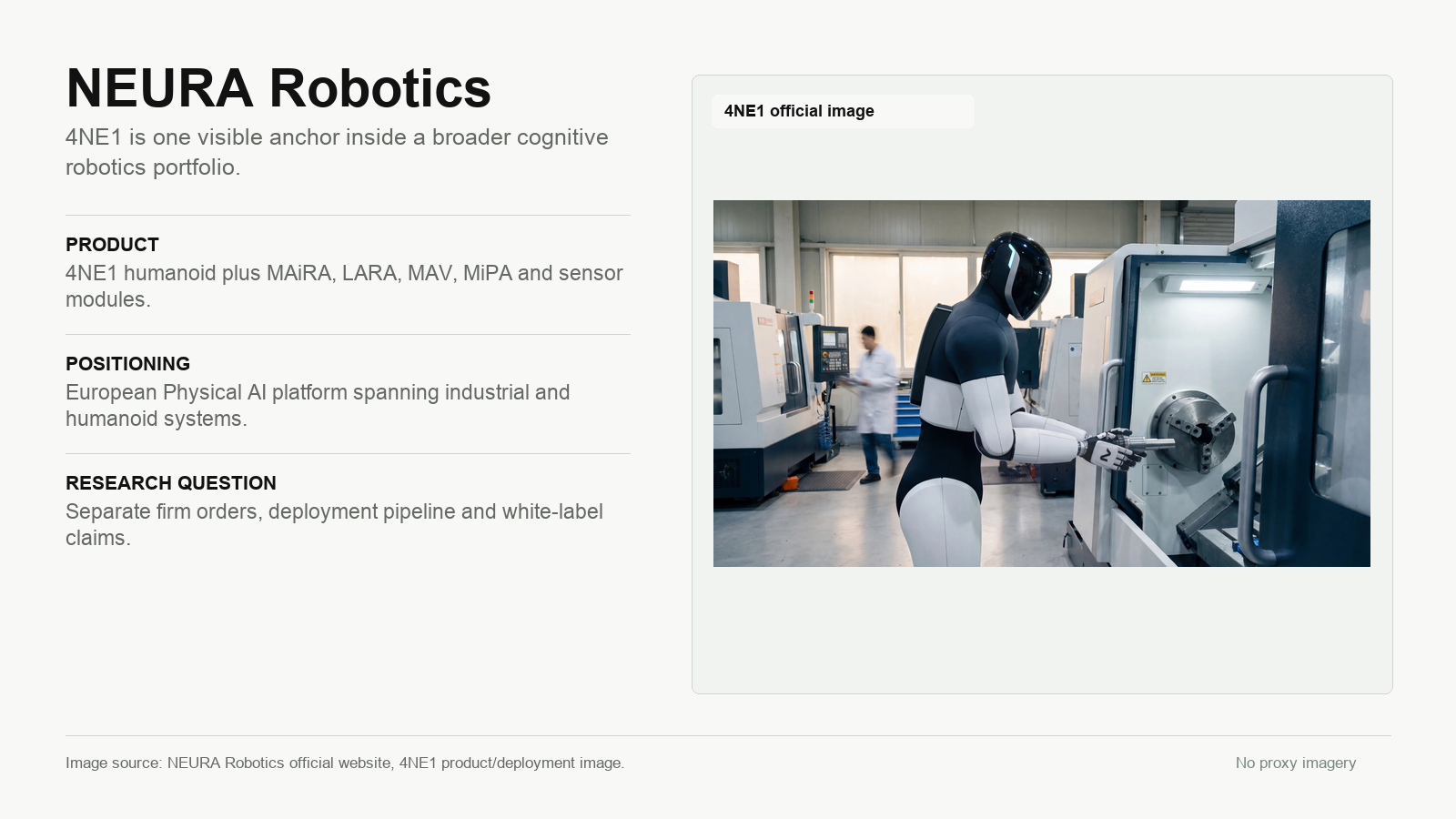

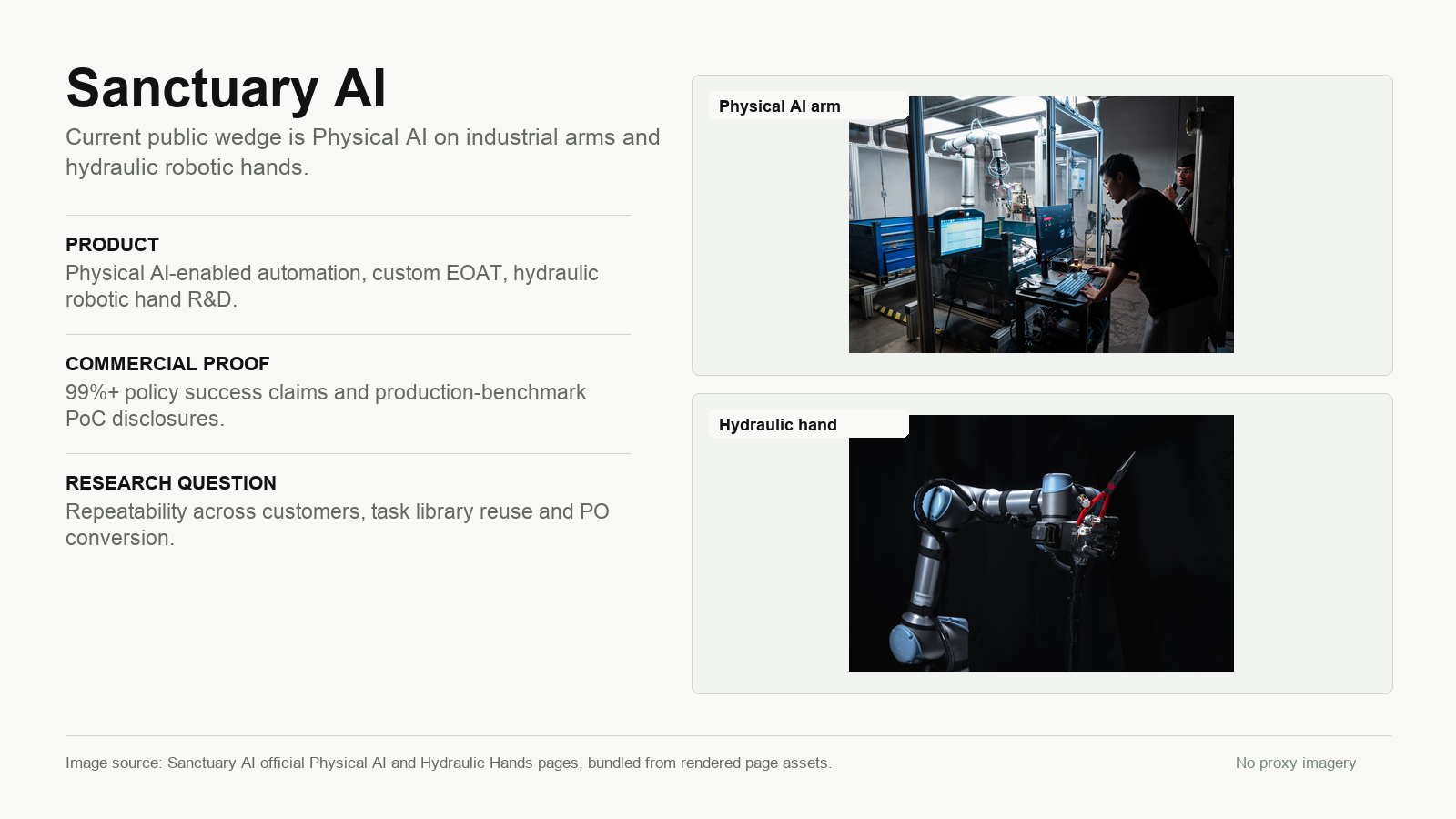

Humanoid and legged robots try to use a general-purpose body to enter spaces designed for humans. Figure, Apptronik, 1X, Agility, NEURA, Boston Dynamics, and Sanctuary AI are key non-China players. Sanctuary AI needs separate treatment: Phoenix is still part of the humanoid/general-purpose robot route, but the company's public commercial entry point in 2026 has shifted to Physical AI-enabled automation on existing industrial arms.

Home, domestic, and companion robots target residential and personal environments. Tasks include cleaning, organizing, delivery, care, companionship, home security, and remote assistance. The difficulty of this category is not a single demo, but privacy, safety, noise, maintainability, long-tail household objects, and the cost of remote takeover. 1X NEO, iRobot, Matic, and Intuition Robotics / ElliQ are key observation directions. Among them, 1X has both a "humanoid body" tag and a "home scenario" tag.

Scenario-specific service and delivery robots target public spaces, communities, restaurants, hotels, retail, and campuses. The core issues are low-speed mobility, cargo/delivery interfaces, public safety, regulatory permission, and operating density. Serve Robotics, CoCo Robotics, Starship, and Bear Robotics are representatives of this category.

Surgical and medical robotics is a high-regulation, high-gross-margin, high-installed-base-stickiness track. Intuitive Surgical is the absolute leader, while Stryker, Medtronic, CMR Surgical, and Johnson & Johnson are important challengers.

Defense and field autonomous systems include drones, unmanned ground vehicles, unmanned vessels, counter-UAS systems, border/base inspection platforms, and high-risk-environment work platforms. Anduril, Shield AI, Skydio, and AeroVironment are core U.S. players.

The Global Robotics Market Landscape

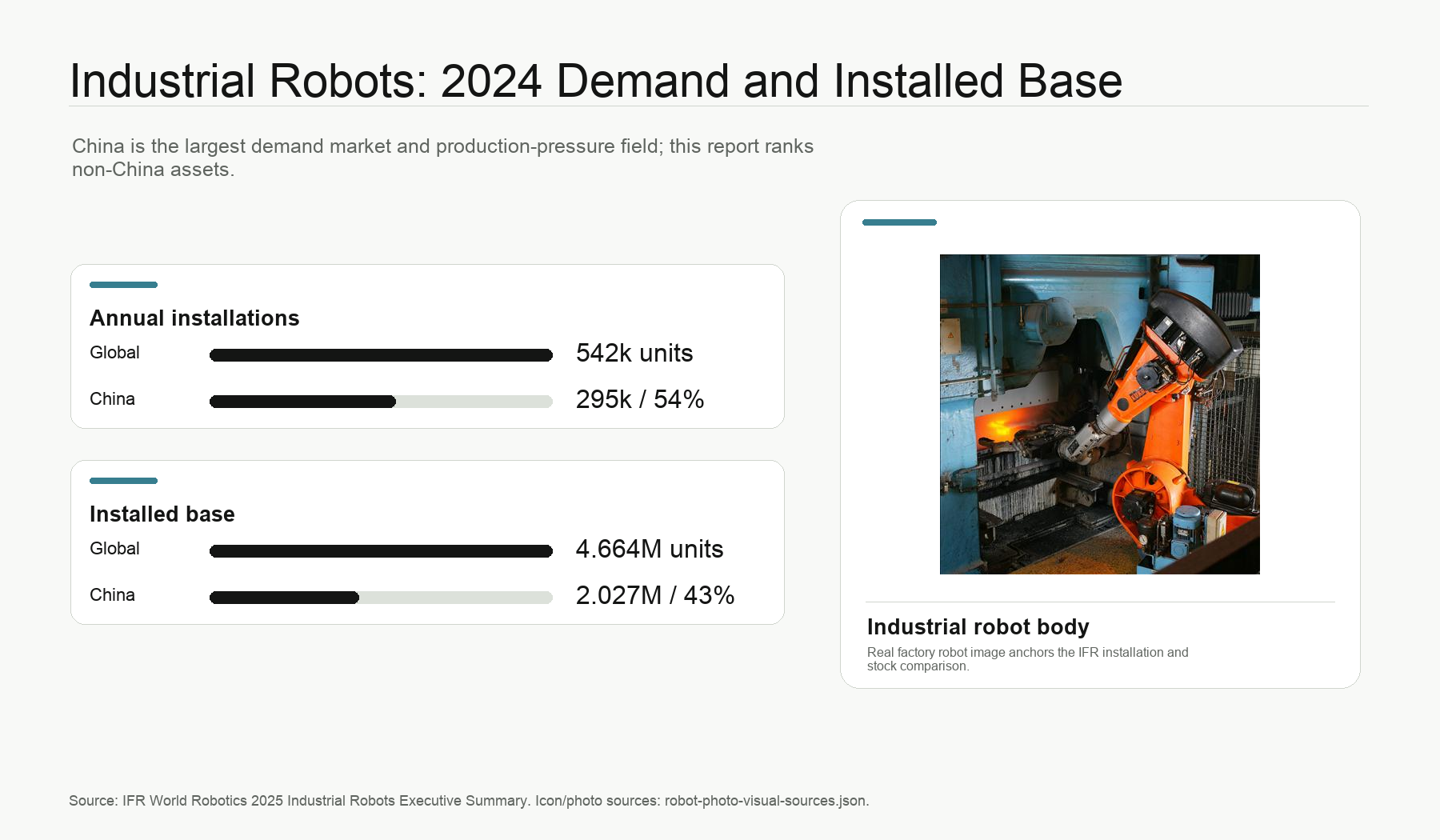

The International Federation of Robotics World Robotics 2025 industrial-robot summary shows that in 2024, global new industrial-robot installations were approximately 542,076 units, and global operational stock was approximately 4,663,698 units. China installed approximately 295,045 new units in 2024, accounting for about 54% of the global total; its operational stock was approximately 2,027,190 units, accounting for about 43% of the global total.

This shows that China is both the world's largest demand market and the largest mass-production pressure field. But this report uses Chinese companies only as competitive references and does not include them in the ranking. This report focuses on whether Maquina and Robo Strategy already cover leading robotics companies and supply-chain assets in the non-China markets of Europe, the United States, Japan, and Korea.

*Illustration: new installations and operational stock of global industrial robots show that China is both the largest demand market and the largest mass-production pressure field

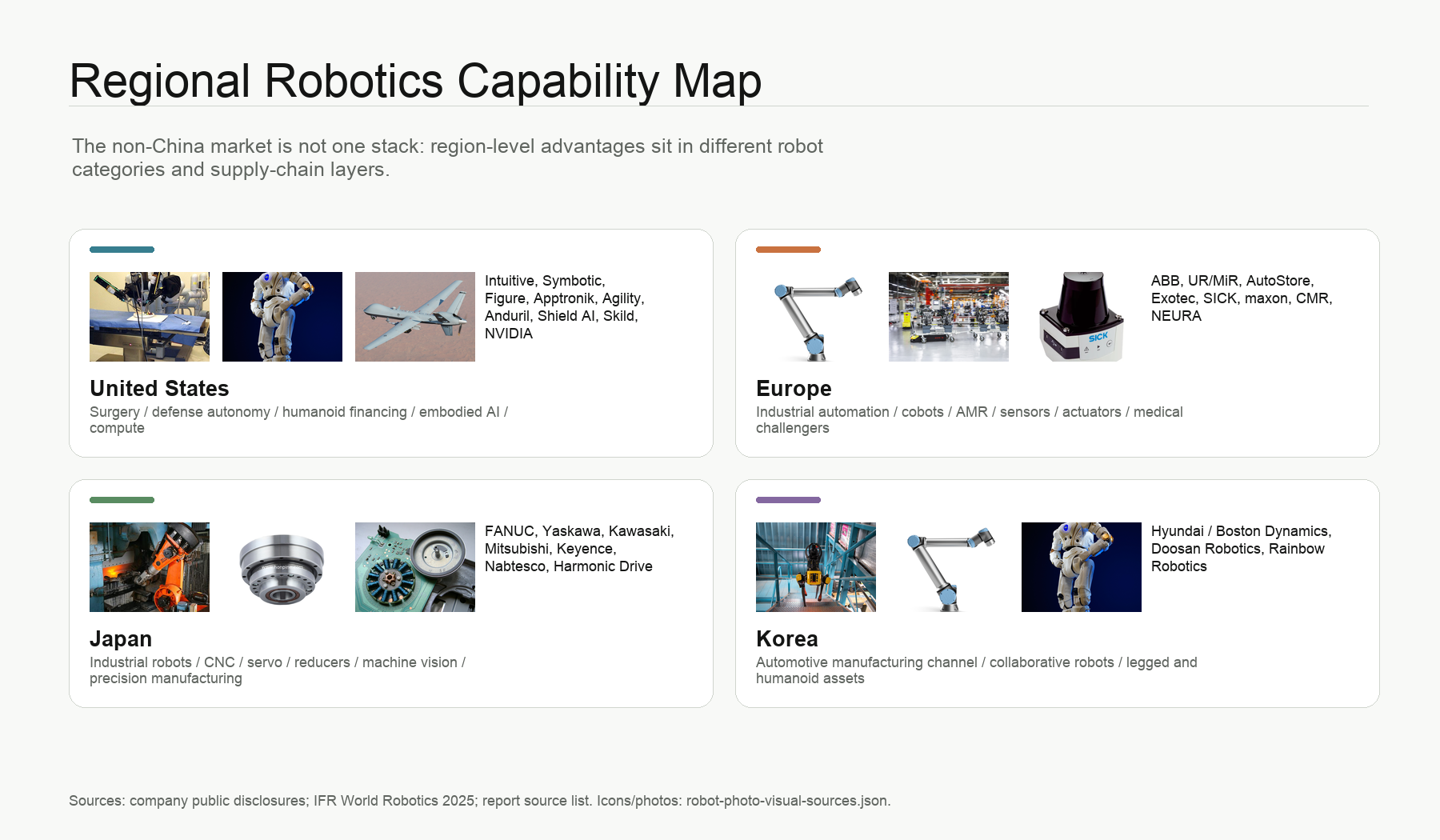

Regionally Differentiated Competition Across Europe, the United States, and Asia

The United States is strong in surgical robotics, warehouse automation, defense autonomous systems, humanoid-robot financing, robot foundation models, and computing platforms. Intuitive Surgical, Symbotic, Figure, Apptronik, Agility, Boston Dynamics, Anduril, Shield AI, Skild AI, Physical Intelligence, FieldAI, and NVIDIA are key nodes in the U.S. map.

Europe is strong in industrial robotics, collaborative robots, warehouse automation, sensors, actuators, industrial safety, and surgical-robot challengers. ABB Robotics, Universal Robots / MiR, AutoStore, Exotec, SICK, Bosch Rexroth, Schaeffler, maxon, CMR Surgical, and NEURA Robotics are core assets.

Japan is strong in industrial-robot bodies, CNC, servos, reducers, machine vision, and precision manufacturing. FANUC, Yaskawa, Kawasaki, Mitsubishi, Keyence, Nabtesco, and Harmonic Drive are foundational supply chains for the global robotics industry.

Korea is strong in automotive-manufacturing coordination, collaborative robots, and humanoid layout. Hyundai owns a core legged-robotics asset through Boston Dynamics, while Doosan Robotics and Rainbow Robotics also maintain presence in collaborative robots and humanoids.

Major Players in Non-China Markets

The following table is roughly ranked by the "latest observable capital size of robotics-related assets." Public companies use market-cap snapshots around 2026-07-02, while private companies use the latest financing or transaction valuations. Group companies are marked as not pure-play robotics businesses; group market cap cannot be directly equated with robotics-business value. Robot shipment, installed-base, and market-share figures are listed only where public measures exist.

| Rank | Company | Region | Category | Latest valuation / market-cap basis | Shipment, deployment, or installed-base basis | Market share or market position | Conclusion |

|---|---|---|---|---|---|---|---|

| 1 | Intuitive Surgical | U.S. | Surgical robotics | About $142.5B market cap; high robotics-business purity | Secondary sources say more than 11,000 da Vinci systems and more than 1,000 Ion systems; 431 da Vinci systems placed in Q1 2026 | De facto global surgical-robotics leader; secondary sources cite 60% to 70% share in robotic surgical systems | Most important uncovered listed robotics leader |

| 2 | Teradyne / Universal Robots / MiR | U.S. / Denmark | Collaborative robots, mobile robots, test equipment | About $66.9B group market cap; robotics business not valued separately | UR historical cumulative shipments have old measures; latest unified basis needs verification | Universal Robots is a core global collaborative-robot player | Core collaborative-robotics miss |

| 3 | Anduril | U.S. | Defense autonomous systems, unmanned systems | Secondary reports show 2026 financing valuation of about $60B | Delivery volume not disclosed | Core U.S. defense autonomous-systems unicorn | Core miss in defense robotics and autonomous systems |

| 4 | FANUC | Japan | Industrial robots, CNC, servos | About $42B market cap; robotics and automation business highly relevant | Common basis says cumulative robot shipments exceed 1M units; needs verification with latest company materials | One of the four major industrial-robot families | Core industrial-robotics miss |

| 5 | Figure AI | U.S. | Humanoid robots | About $39B post-money after 2025 Series C | Company says first BotQ line has annual capacity of 12,000 units; in April 2026 it said more than 350 Figure 03 units had been produced | Highest-valuation tier among private humanoid robotics companies | Covered, but valuation is already highly forward-priced |

| 6 | Symbotic | U.S. | Warehouse automation, system robotics | About $27.1B market cap | Single-robot shipments not disclosed; disclosed by systems and customer deployments | Core player in large-scale North American warehouse automation | Mature warehouse-robotics miss |

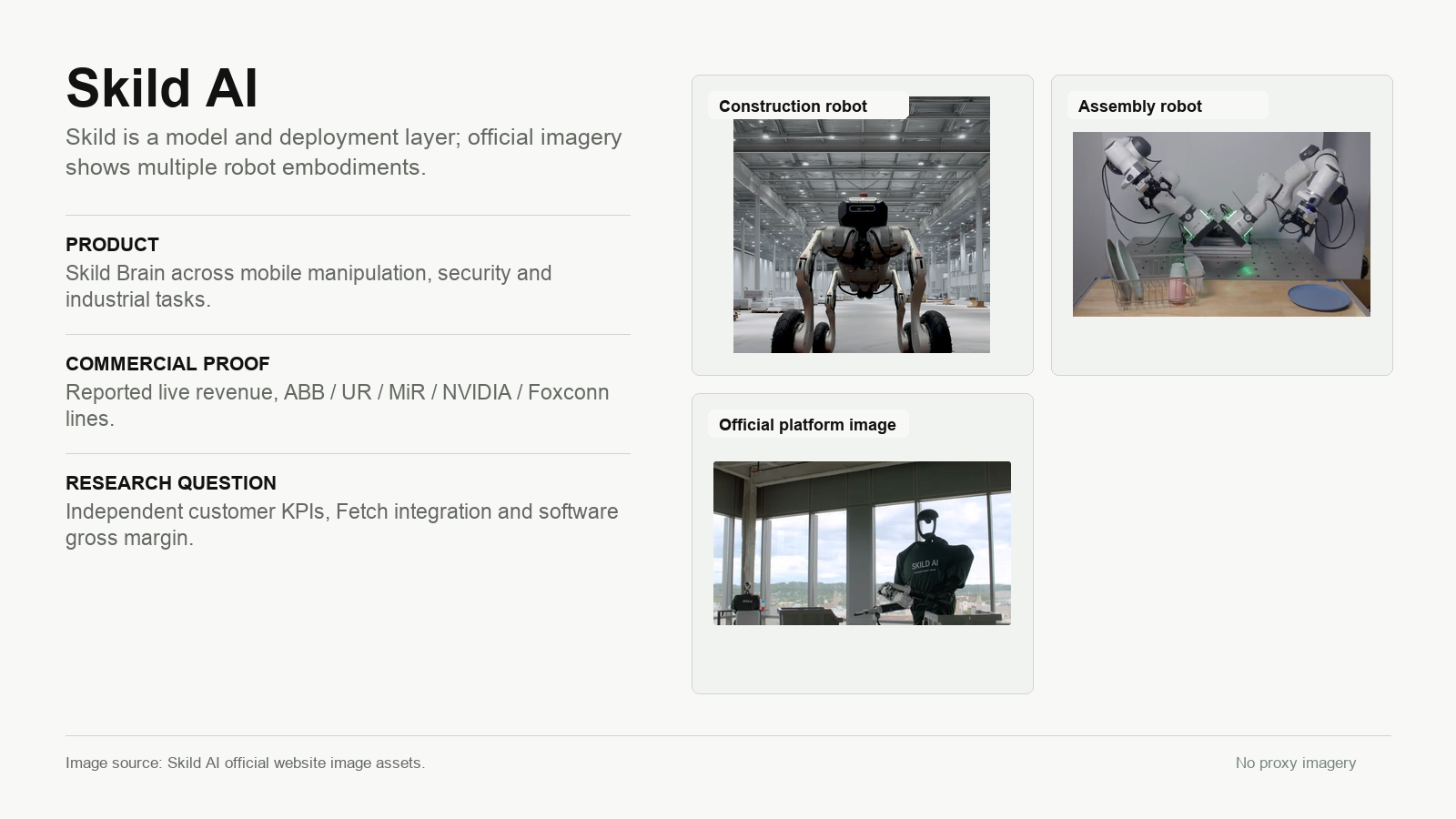

| 7 | Skild AI | U.S. | Robot foundation model, warehouse-deployment data layer | 2026 Series C raised $1.4B; valuation over $14B | 2025 live revenue about $30M; partnerships with ABB / UR / MiR / NVIDIA / Foxconn; acquired Zebra / Fetch robotics assets, with transaction terms undisclosed | Leading private robotics foundation-model company, extending into industrial and warehouse deployments | Important model-layer miss |

| 8 | Shield AI | U.S. | Defense AI, drone autonomy | Secondary reports say about $12.7B post-money in 2026 | V-BAT / Hivemind delivery volume not disclosed | Leading U.S. defense autonomy software company | Defense autonomous-systems miss |

| 9 | Yaskawa Electric | Japan | Industrial robots, servos, motion control | About $11.4B market cap | Motoman cumulative shipments have historical measures; latest unified basis not disclosed | One of the four major industrial-robot families; strong in upstream servos | Industrial and motion-control miss |

| 10 | Physical Intelligence | U.S. | Robot foundation model | Confirmed historical valuation about $5.6B; secondary reports say new financing may reach about $11B, pending verification | Software platform mainly; real deployment scale not systematically disclosed | Important private robot foundation-model company | Important model-layer miss |

| 11 | NEURA Robotics | Germany | Cognitive robots, collaborative robots, humanoids, mobile platforms | Official financing basis up to $1.4B; secondary reports once gave about $7B valuation | Company says order/deployment pipeline exceeds $1B; real delivery count not disclosed | Important European cognitive-robotics and humanoid private company | Robo Strategy miss |

| 12 | Apptronik | U.S. | Humanoid robots | Local draft and secondary basis around $5B to $5.5B | Customer pilots are clear; real mass-production deliveries not disclosed | First tier of U.S. enterprise humanoid robots | Covered; shared core asset |

| 13 | ABB Robotics | Switzerland / Sweden | Industrial robots, control, automation | SoftBank acquisition enterprise value about $5.375B to $5.4B; ABB group market cap is higher but does not represent robotics-business valuation | Robot cumulative installations need continued verification against latest company basis | One of the four major industrial-robot families | Mature industrial-robotics core asset missed |

| 14 | 1X Technologies | Norway / U.S. | Home humanoid robots | Maquina entry basis about $4.55B; higher valuation reports not fully confirmed | Preorder demand and capacity are company basis; revenue recognition and delivery not disclosed | Leading private home humanoid robotics company | Robo Strategy miss |

| 15 | AutoStore | Norway | Warehouse automation, cube storage | About $4.3B market cap | Company investor page basis is 1,950+ systems across 65+ countries | Global core player in cube-storage automation | Mature warehouse-automation miss |

| 16 | CMR Surgical | U.K. | Surgical robots | 2021 financing valuation about $3B; subsequent update needed | Historical public basis says Versius procedures exceeded 20,000; latest needs verification | European surgical-robotics challenger | Private medical-robotics miss |

| 17 | Agility Robotics | U.S. | Biped logistics robots | Signed de-SPAC basis about $2.5B pre-money, not yet completed | Company/transaction materials cite 65,000+ operating hours, 9 customer facilities, $300M+ orders, and 1,000 Digit v5 units under three-year leases | Relatively strong commercialization evidence for logistics biped robots | Robo Strategy miss |

| 18 | FieldAI | U.S. | General robot software, field autonomy | Secondary reports value it at about $2B | Reports say revenue and customer contracts exceed $100M; real robot count not disclosed | Important emerging company in robot software and field deployment | Software-layer miss |

| 19 | Locus Robotics | U.S. | Warehouse mobile robots | Old financing basis near $2B; update needed | Large-scale picking measures exist for customers such as DHL; single-unit shipments need verification | Mature warehouse AMR player | Mature warehouse AMR miss |

| 20 | Exotec | France | Warehouse automation, Skypod | Historical valuation around $2B level; update needed | Public materials say 135+ systems and more than one million daily pick/place operations; latest company basis needs verification | Important European warehouse-automation player | European warehouse-automation miss |

| 21 | Boston Dynamics | U.S. / Korea | Legged robots, mobile manipulation | Hyundai 2021 acquisition valuation about $1.1B; current value undisclosed | Real cumulative deliveries of Spot, Stretch, and Atlas not disclosed | Benchmark in dynamic control and legged robotics | One of the most important unlisted body-platform misses |

| 22 | Standard Bots | U.S. | Collaborative robots, factory automation | Local basis about $1B valuation | "Hundreds of robot units/workstations" type basis needs continued verification | Representative of new-generation U.S. collaborative robots | Covered by Robo Strategy; missed by Maquina |

| 23 | Serve Robotics | U.S. | Sidewalk delivery robots | Small-cap listed company | Fleet size and active deployments need continued verification through quarterly filings | Listed target in small delivery robots | Missed, but lower priority |

| 24 | Dyna Robotics | U.S. | Mobile manipulation, embodied intelligence | Series A amount about $120M; valuation undisclosed | Commercial deployments are mostly company self-disclosed; unified unit count not disclosed | Early mobile-manipulation-arm asset | Covered by Robo Strategy; missed by Maquina |

| 25 | Dexmate | U.S. / Turkey | Mobile manipulation arms, grippers | Undisclosed | Undisclosed | Early hardware platform; less certain than leaders | Covered by Robo Strategy; missed by Maquina |

Investment Analysis of Maquina and Robo Strategy

The core of this chapter is not "who invested in robots," but to clarify how the two capital machines turn private robotics equity into tradable assets, and what risks investors actually bear. Maquina's risks come from the DEUS token, DAO governance, on-chain/off-chain asset mapping, and SPV attestations. Robo Strategy's risks come from the 1940 Act closed-end fund, Level 3 private-security valuation, BOT stock premium/discount to NAV, and the large-scale stock issuance mechanism.

Different Investment Models

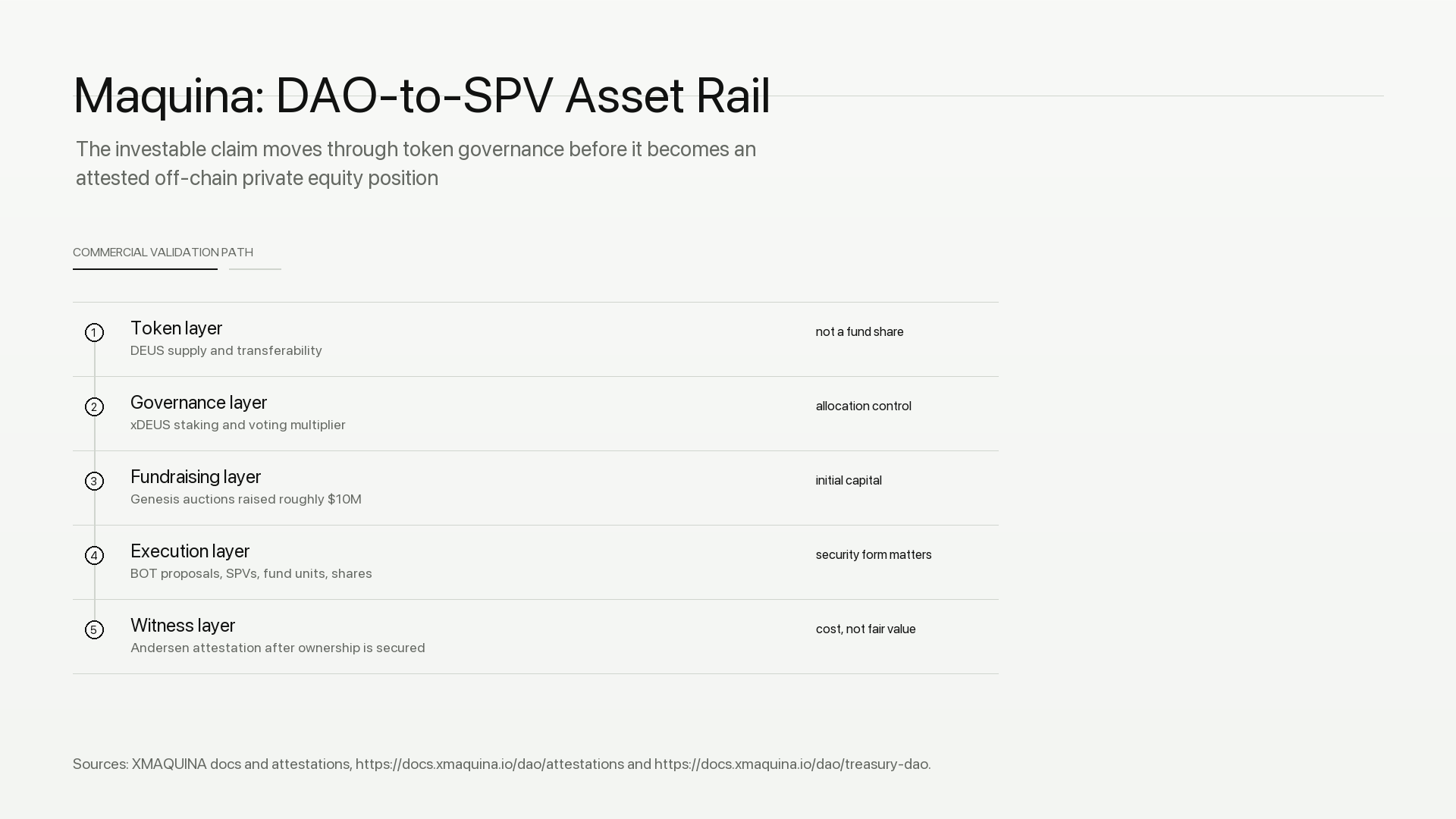

Maquina: DAO Token, On-Chain Governance, and Off-Chain SPV Combination

Maquina is an investment vehicle that wraps private robotics equity exposure with crypto rails. Its asset and rights chain can be split into five layers:

| Layer | Mechanism | Investment implication |

|---|---|---|

| Token layer | DEUS, 1B maximum supply, fully transferable after the 2026-05-27 TGE | Investors buy a governance/economic-exposure token, not redeemable fund shares |

| Governance layer | DEUS is staked into xDEUS, receiving non-transferable governance rights and vote multipliers that accrue with staking time | Asset allocation, buybacks, staking rewards, and future investment direction are driven by governance |

| Fundraising layer | Five Genesis Auction rounds raised about $10M in total and distributed 23.24% of DEUS supply | This is the source of early robotics-investment capital, but it is not current NAV |

| Execution layer | Investments are approved through DAO proposals such as BOT-01, BOT-03, BOT-04, BOT-06, BOT-07, and BOT-09, then executed through SPVs, fund units, membership interests, or company shares | The security form in investment documents matters; fund units, SPV membership, preferred shares, and ordinary shares cannot be mixed together |

| Attestation layer | Andersen LLP issues attestation after investment execution and ownership are formally secured | What is attested is funded capital / ownership record, not current fair value, and not assets redeemable by DEUS holders |

Illustration: Maquina's asset chain must be traced from DEUS / xDEUS governance all the way to specific SPVs, fund units, or company shares, then checked for whether Andersen completed attestation; governance approval, user forms, and attested cost base cannot be mixed.

Maquina's long-term mechanism also includes RCM Protocol and SubDAO. The SubDAO idea is that each public auction raises capital for one specific robotics company; after success, it mints a tradable token anchored to an SPV that holds that company's equity. Each SubDAO returns 5% of token supply to the DAO and brings the DAO issuance fees, trading fees, and operating revenue. This makes Maquina more than a holdings table: it is trying to split private robotics equity into tradable, governable, composable on-chain capital-market assets.

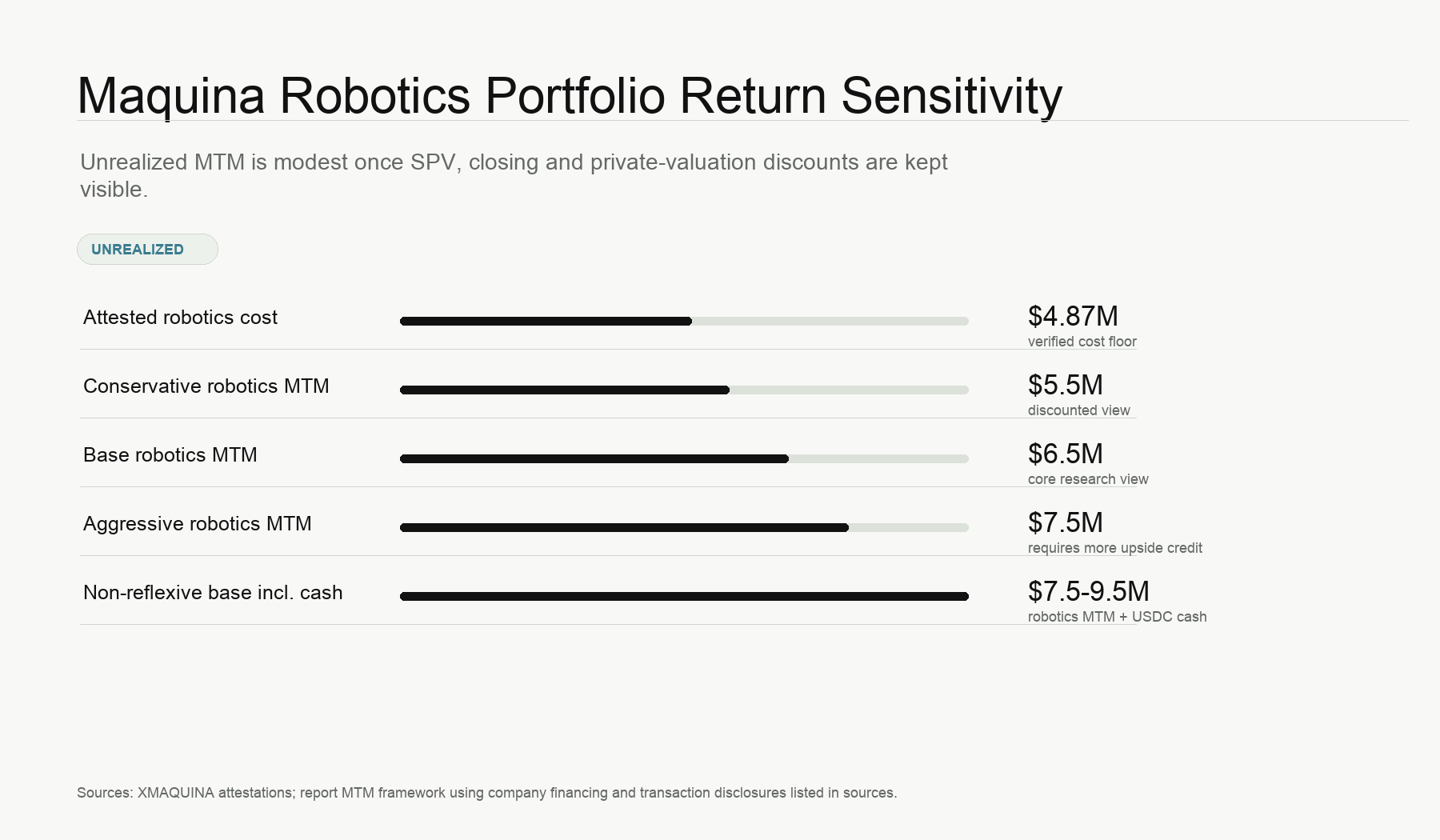

But Maquina's biggest research risk is also here. It has no official audited NAV. A third party once gave a headline treasury NAV of about $32M, but most of it was DEUS held by the DAO itself and is reflexive. After stripping out DAO-owned DEUS, the most reliable non-reflexive asset base is approximately $2M in USDC cash plus the $4.8728M Andersen-attested robotics-equity cost base. If marked to market, the robotics equity is about $6.5M to $7.5M; with a conservative discount, about $5.5M to $6.0M. Therefore, Maquina's real non-reflexive asset backing is closer to a single-digit millions of dollars level, not headline NAV.

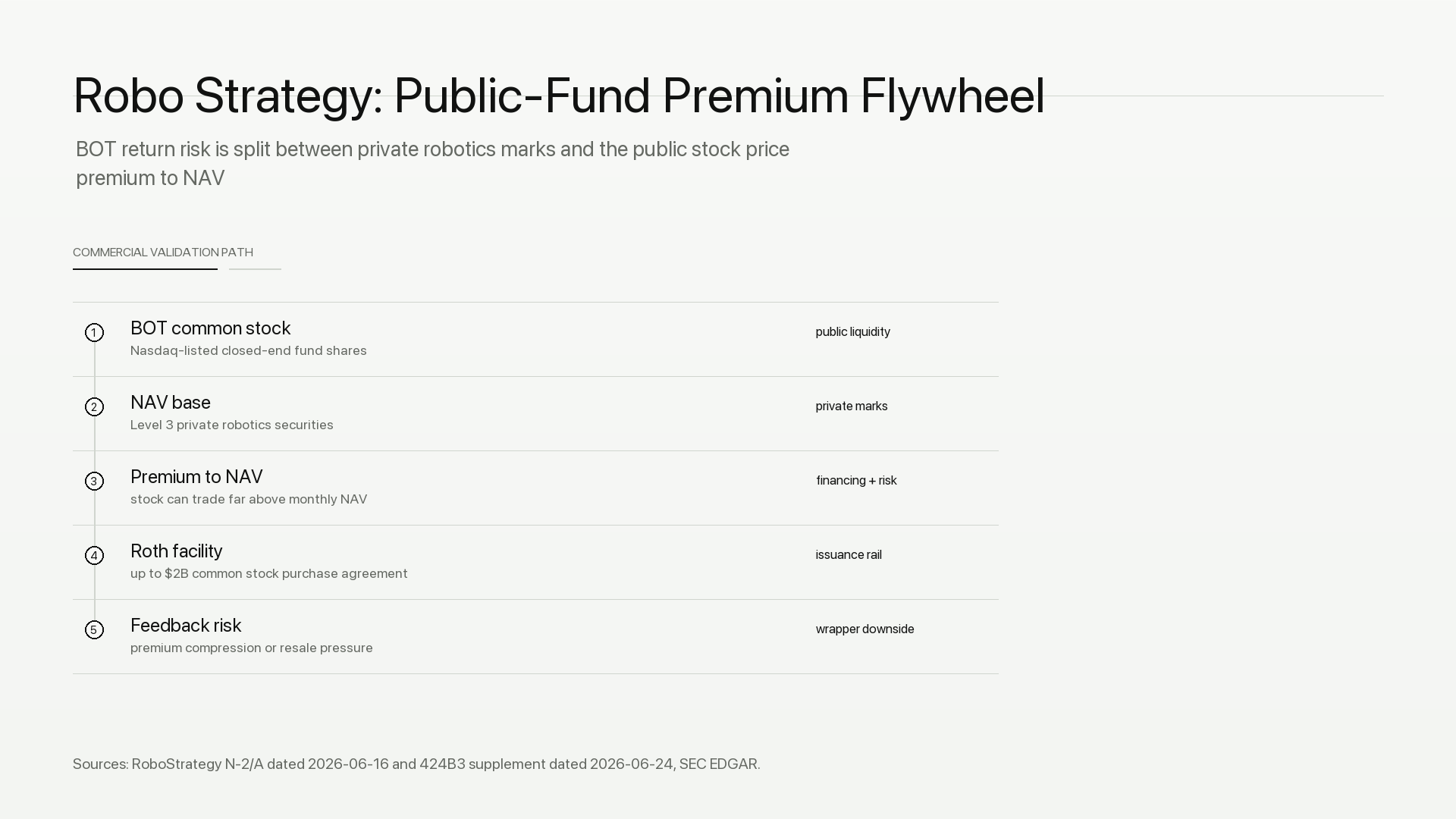

Robo Strategy: Listed Closed-End Fund and Public-Market Financing Flywheel

Robo Strategy is a completely different structure. It is an SEC-registered, Nasdaq-listed, non-diversified closed-end management investment company under ticker BOT. It is not a DAO and not a crypto DAT. It wraps private robotics and embodied-intelligence securities in a listed closed-end fund.

| Mechanism | Robo Strategy disclosure basis | Investment implication |

|---|---|---|

| Legal entity | RoboStrategy, Inc., CIK 0002081119, Maryland corporation, 1940 Act closed-end management investment company | Investors hold listed common shares, not the private-company equity itself |

| Listing/trading | BOT began trading on Nasdaq Global Market on 2026-05-11 | Liquidity comes from the stock market; price can deviate materially from NAV |

| Investment scope | Under normal market conditions, at least 80% of net assets are invested in robotics / embodied-AI technology companies primarily located in the United States; long-term target of 20-30 positions | More like a public-market version of a private robotics fund than Maquina |

| Fees | 2.5% annual management fee, paid monthly in arrears based on average gross assets | Fees are based on gross assets; if leverage or balance-sheet expansion is used in the future, the fee base also grows |

| NAV disclosure | NAV calculated monthly and planned to be released within 30 days after month-end; quarterly portfolio investments disclosure, including SPV underlying share class / share count and portfolio percentage | More transparent than Maquina, but valuations are still mainly Level 3 private securities |

| Stock issuance | On 2026-05-11, signed a common stock purchase agreement of up to $2B with Roth Principal Investments; on 2026-06-16, N-2/A registered Roth to resell up to 14.10M shares | If BOT trades at a high premium, issuing stock may accrete NAV; but it also brings dilution, selling pressure, and premium-collapse risk |

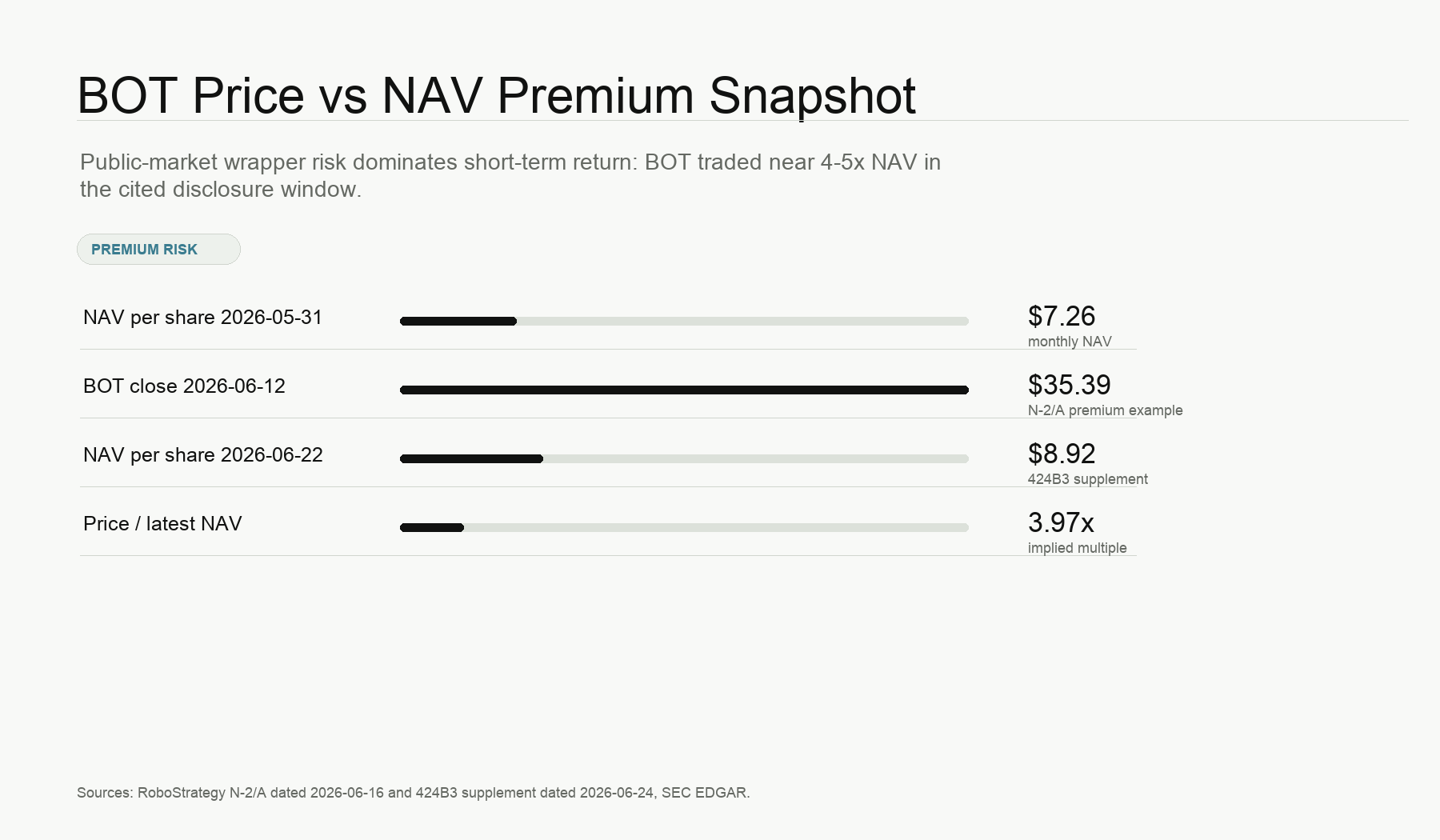

The key question for Robo Strategy is not "whether it invested in Figure / Apptronik / Dyna," but whether the public-market wrapper can continue converting a high premium in BOT stock into new private robotics assets. The example in SEC filings is intuitive: on 2026-06-12, BOT closed at $35.39, while 2026-05-31 NAV was $7.26, implying a 387.5% premium to NAV, or about 4.875x NAV. If recalculated using the latest available 2026-06-22 NAV of $8.92, $35.39 is still about 3.97x NAV.

Therefore, Robo Strategy's investment return consists of two layers: one is the fair-value change of private assets such as Figure, Dyna, Apptronik, and Dexmate; the other is the BOT stock premium/discount to NAV and refinancing capacity. The latter is more important in the short term and also more dangerous.

Illustration: Robo Strategy's core is not simply "holding robotics companies," but using the high-premium stock-financing capacity of a listed closed-end fund to expand private robotics assets; when the premium falls, the same mechanism amplifies risk in reverse.

Mechanism Comparison

| Comparison item | Maquina | Robo Strategy |

|---|---|---|

| What investors buy | DEUS token / governance and economic exposure | BOT listed common stock |

| Asset container | DAO treasury + SPV + SubDAO / RCM | 1940 Act closed-end fund |

| Key disclosures | DAO proposals, Andersen attestation, docs / portal, third-party treasury research | SEC N-CSRS, N-2/A, 424B3, monthly NAV |

| NAV nature | No official audited NAV; part of headline NAV is driven by DEUS self-held position and is highly reflexive | SEC-disclosed NAV, but private assets are mostly Level 3 fair value |

| Redeemability | DEUS is not a hard redemption right against NAV | BOT common shares are also not a redemption right against NAV |

| Expansion mechanism | DEUS premium, DAO treasury, SubDAO auctions, RCM fees | BOT high-premium stock issuance, up to $2B Roth facility |

| Advantages | Globally open participation, on-chain governance, ability to split single-company equity into tradable tokens | Strong compliance disclosures, larger asset scale, strong public-market financing capability |

| Core risks | Small asset scale, reflexive NAV, off-chain equity cannot be verified on-chain, DEUS liquidity and governance risks | Fragile high premium, Level 3 valuation, concentrated positions, stock-issuance dilution |

Current Investment Coverage of the Two

Coverage must be layered by basis. If we only look at "number of names," Robo Strategy is broader. If we look at "core private non-China humanoid robotics," Maquina is more complete. If we look at the "global non-China robotics industry chain," both are far from complete.

Maquina's Coverage

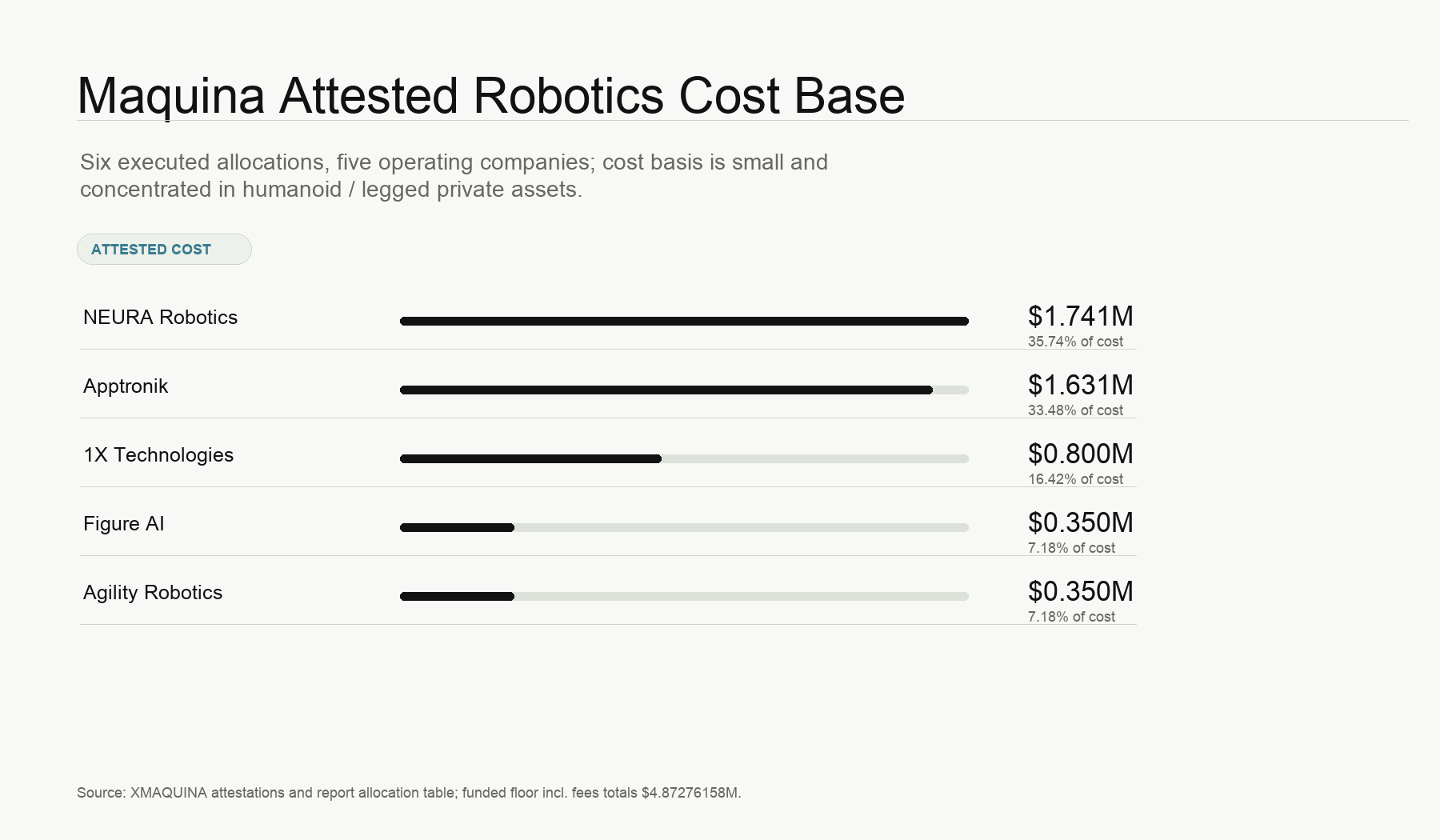

Maquina's attested robotics-equity cost base consists of 6 executed allocations covering 5 operating companies: Apptronik, Figure AI, Agility Robotics, 1X, and NEURA. Total funded floor incl. fees is $4,872,761.58.

| Company | Proposal / execution | Holding path | Attested cost | Share of Maquina attested robotics-equity cost base |

|---|---|---|---|---|

| NEURA Robotics | BOT-09, executed 2026-03-06 | InterAlpen Partners LLC; Series C Preferred Stock | $1,741,425 | 35.74% |

| Apptronik | BOT-01 + BOT-06, executed 2025-05-27 and 2025-10-14 | Forge / Fund FG-NMO fund units, 55,702 units total | $1,631,336.58 | 33.48% |

| 1X Technologies | BOT-07, executed 2025-11-12 | 1X Holding AS, 200 ordinary shares | $800,000 | 16.42% |

| Figure AI | BOT-03, executed 2025-09-11 | AI Robotics Investments LLC, 5.6429% SPV membership interest | $350,000 | 7.18% |

| Agility Robotics | BOT-04, executed 2025-08-14 | WPX Fund I / Second Market Growth, 4,799 preferred-share exposure | $350,000 | 7.18% |

| Total | 6 executed allocations | 5 robotics operating companies | $4,872,761.58 | 100.00% |

Illustration: Maquina's attested robotics-equity cost base is concentrated in NEURA and Apptronik, while Figure and Agility are only small positions around the $350,000 level; this is why "name coverage" cannot replace "capital coverage."

This shows that Maquina's coverage is not "large and comprehensive," but "small in scale, highly concentrated, and humanoid-tilted." NEURA and Apptronik together account for about 69.22% of the cost base. 1X accounts for 16.42%. Figure and Agility are both only smaller positions around the $350,000 level. Skild AI, Sanctuary AI, Robotico, and Genki Robotics are not counted in the attested cost base in this report: Skild only has approved / pending clues; Sanctuary and Genki lack public Maquina investment documents and Andersen attestation; Robotico has an officially disclosed pre-seed 20% equity allocation from XMAQUINA / DEUS Labs, but lacks amount, transaction documents, and Andersen attestation, so it can only be treated as an ecosystem-incubated equity and market-intelligence infrastructure observation item.

Based on the 25 core non-China player sample above, Maquina has attested coverage of 5, or about 20%. If Skild is included as potential / pending exposure for observation, coverage becomes 6, or 24%, but that is not current deployed-equity coverage. Among the top ten players by capital size, Maquina currently has confirmed coverage only of Figure AI; Skild can only be treated as a pending observation item. In the "humanoid/legged/embodied private core sample," Maquina covers Figure, Apptronik, Agility, 1X, and NEURA, clearly better than Robo Strategy.

Robo Strategy's Coverage

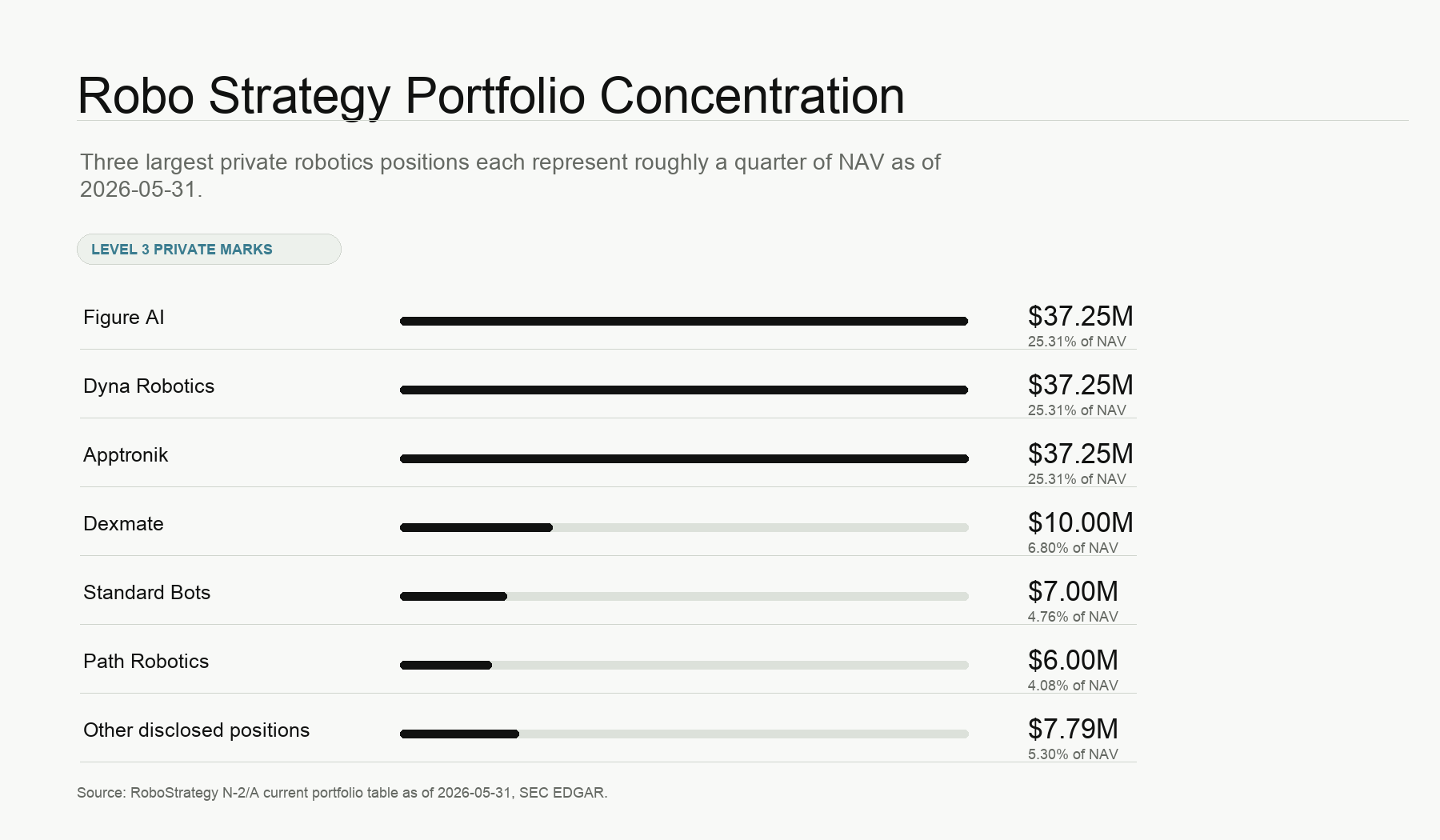

Robo Strategy's SEC-disclosed portfolio is larger and more concentrated. The 2026-05-31 N-2/A current portfolio table shows that its disclosed robotics/embodied-intelligence and adjacent assets had a total fair value of about $142,541,470, covering 13 portfolio companies.

| Company | Instrument / path | 2026-05-31 fair value | Share of net assets |

|---|---|---|---|

| Figure AI | NV FigureAI Series B QP Partners LLC LP interest, economic exposure to Figure AI Series B Preferred | $37,250,000 | 25.31% |

| Dyna Robotics | Direct Series A Preferred Stock, 1,491,163 shares | $37,249,997 | 25.31% |

| Apptronik | SPV LP interest + direct Series Seed 1 Preferred | $37,250,002 | 25.31% |

| Dexmate | Direct Series 1 Seed Preferred, 1,740,280 shares | $9,999,997 | 6.80% |

| Standard Bots | Direct Series C Preferred, 234,190 shares | $6,999,986 | 4.76% |

| Path Robotics | Direct Series D-2 Preferred, 773,660 shares | $5,999,996 | 4.08% |

| REK | Direct Series 1 Seed Preferred, 1,875,891 shares | $2,500,000 | 1.70% |

| S | SAFE, convertible into Series B Preferred at next financing | $2,000,000 | 1.36% |

| Cyan / CoCo Robotics | RoboStrategy DDGR LLC SPV interest in SAFE | $1,500,000 | 1.02% |

| Nox Metals | SAFE, convertible into equity at next financing | $750,000 | 0.51% |

| Endiatx | Direct Series A Preferred, 285,322 shares | $499,998 | 0.34% |

| Allonic | Direct Pre-seed Preferred, 154,798 shares | $291,494 | 0.20% |

| Purple Rhombus | LP interest in PU-1003 Fund I, underlying Purple Rhombus SAFE | $250,000 | 0.17% |

| Total | 13 disclosed portfolio companies | ~$142,541,470 | About 96.87% |

Illustration: Robo Strategy's scale is much larger than Maquina's, but the portfolio is also highly concentrated in three roughly $37.25M positions: Figure, Dyna, and Apptronik. Together they account for about 75.93% of NAV.

Robo Strategy's "broad coverage" is mainly reflected in early-stage U.S. private robotics and robotics-adjacent assets: Dyna, Dexmate, Standard Bots, Path, CoCo, Endiatx, Purple Rhombus and others are directions Maquina does not have. But its coverage of top non-China humanoid/embodied private companies is actually weaker than Maquina's: it does not have Agility, 1X, or NEURA, and it has no disclosed Skild, Physical Intelligence, Boston Dynamics, or Sanctuary.

Based on the 25 core non-China player sample in this report, Robo Strategy covers Figure, Apptronik, Dyna, Dexmate, and Standard Bots, or about 20%. If Path is included as a disclosed robotics-automation asset that did not enter the top-25 sample in Chapter 2, the portfolio has more names, but its coverage of "global non-China leaders" is still not high. Among the top ten players by capital size, Robo Strategy also covers only Figure AI. From the perspective of mature industrial, medical, warehouse automation, and supply-chain leaders, Robo Strategy and Maquina basically do not cover Intuitive Surgical, Teradyne / Universal Robots / MiR, FANUC, Yaskawa, ABB Robotics, Symbotic, AutoStore, Locus, Exotec, and key upstream component companies.

Coverage Conclusion

| Basis | Maquina | Robo Strategy | Conclusion |

|---|---|---|---|

| Number of verified robotics / embodied-intelligence companies | 5 operating companies / 6 allocations | 13 portfolio companies | Robo Strategy has more names |

| Verified robotics equity / portfolio scale | $4.87M attested cost; MTM about $6.5-7.5M | $142.54M disclosed fair value | Robo Strategy is far larger than Maquina |

| Coverage of the 25 core non-China players above | 5/25 = 20%; 6/25 if Skild observation item is included | 5/25 = 20% | Similar count, but different composition |

| Coverage of top ten capital-size players | Figure; Skild pending | Figure | Both are very low |

| Core humanoid/legged/embodied private coverage | Figure, Apptronik, Agility, 1X, NEURA; Skild pending | Figure, Apptronik; Dyna/Dexmate are mobile manipulation / manipulation platforms, not humanoid bodies | Maquina is more complete |

| Early U.S. private robotics coverage | Less broad, concentrated in Apptronik / Figure / Agility / 1X | Figure, Dyna, Apptronik, Dexmate, Standard Bots, Path, CoCo, etc. | Robo Strategy is broader |

Current Portfolio Return Situation of the Two

Maquina: Paper Returns Concentrated in Apptronik, Other Positions Need Discounts

Maquina's returns cannot be simply replaced with DEUS headline NAV. The correct method is to first look at the Andersen-attested robotics-equity cost, then mark to market by each company's latest financing/transaction basis, distinguishing closed rounds, reported rounds, unclosed de-SPACs, and SPV discounts.

| Company | Maquina cost base | Current research-department valuation basis | Estimated multiple | Estimated MTM | Return quality |

|---|---|---|---|---|---|

| Apptronik | $1.631M | 2026 Series A-X1/A-X2 about $5B post; media basis >$5.5B | About 1.6-2.0x blended; first tranche about 3x | $2.6-3.3M | Cleanest closed upside source |

| NEURA | $1.741M | Series C-era mark, financing up to $1.4B, media valuation about $7B | About 1.0x | ~$1.7M | Bought in the current round; short-term re-rate not proven |

| 1X | $0.800M | Maquina basis $4.55B entry; $9-10B financing reports unconfirmed/unclosed | About 1.0-2.0x, depending on whether the new round can be confirmed | $0.8-1.6M | Large upside, but requires high discount |

| Figure AI | $0.350M | About $39B post after 2025 Series C; Maquina entered near high valuation | About 0.85-1.0x | $0.30-0.35M | Not an early low-price position |

| Agility Robotics | $0.350M | Signed de-SPAC with Churchill XI, $2.5B pre-money, not yet completed | About 1.2x headline; closing / redemption risk must be deducted | ~$0.4M | Best liquidity path, but transaction not closed |

| Total | $4.873M | Conservative $5.5-6.0M; aggressive $6.5-7.5M | Conservative about 1.13-1.23x; aggressive about 1.33-1.54x | $5.5-7.5M | Unrealized, non-redeemable, dependent on private valuations |

Illustration: Maquina's real alpha currently mainly comes from Apptronik's paper upside. If DEUS self-holdings and reflexive NAV are removed, the non-reflexive asset base is closer to $7.5M to $9.5M rather than headline treasury NAV.

Therefore, Maquina's portfolio has not "already multiplied many times." Under the current research basis, its real alpha mainly comes from Apptronik. 1X is an unconfirmed upside option. Agility is an uncompleted liquidity event. Figure entered at a high valuation. NEURA is a large position but close to current-round cost. After discounting these, it is more reasonable to mark Maquina's attested robotics-equity cost base from $4.87M cost to $5.5M to $7.5M, rather than directly citing headline treasury NAV.

If approximately $2M of USDC cash is also included in non-reflexive assets, Maquina's verifiable non-reflexive asset base is about $7.5M to $9.5M. DEUS self-held tokens, future SubDAO fees, RCM fees, and governance premium can form additional option value, but they cannot be mixed with deployed robotics equity.

Robo Strategy: Underlying Portfolio Has Not Yet Proven Large Appreciation; Stock Premium Is the Core Variable

Robo Strategy's return analysis must be split into two layers: "fund NAV" and "BOT stock price."

| Date | Metric | Value | Explanation |

|---|---|---|---|

| 2026-02-28 | Investments at fair value / cost | $134.80M | N-CSRS shows tax cost equals fair value; unrealized appreciation is 0 |

| 2026-02-28 | Cash | $12.03M | Still some cash in the early period |

| 2026-02-28 | Net assets | $146.21M | Fund net-asset base |

| 2026-02-28 | Shares outstanding | 19,908,968 | Used to calculate NAV |

| 2026-02-28 | NAV per share | $7.34 | SEC disclosure |

| 2026-05-31 | Total assets | $148.03M | N-2/A current portfolio table |

| 2026-05-31 | Disclosed portfolio fair value | ~$142.54M | Total across 13 portfolio companies |

| 2026-05-31 | NAV per share | $7.26 | SEC disclosure |

| 2026-06-12 | BOT stock close | $35.39 | Used in N-2/A premium example |

| 2026-06-12 vs 2026-05-31 NAV | Premium to NAV | 387.5% | Stock price about 4.875x NAV |

| 2026-06-22 | NAV per share | $8.92 | 424B3 supplement disclosure |

| $35.39 vs $8.92 | Implied price / NAV | About 3.97x | Even using updated NAV, the premium remains very high |

Illustration: Robo Strategy's short-term return risk comes not only from the private valuations of Figure / Dyna / Apptronik, but also from whether BOT stock can sustain a 3.97x to 4.875x premium to NAV.

Looking at the underlying portfolio, Robo Strategy's SEC filings do not prove that the portfolio has already achieved significant investment returns. The 2026-02-28 schedule shows total cost equal to fair value and unrealized appreciation of 0. The 2026-05-31 current portfolio table gives issuer fair value, not third-party exit prices. What is truly aggressive is the listed wrapper: BOT once traded near 4-5x NAV, giving it a financing flywheel of "issuing high-priced shares to buy more private assets."

If this flywheel works, it creates two positive feedback loops. First, issuing shares at a high premium increases per-share NAV or at least does not dilute NAV. Second, new capital continues to buy private robotics assets such as Figure / Apptronik / Dyna / Dexmate, expanding fund scale. But it also has two negative feedback loops. First, if BOT's premium falls, shareholder returns will first be swallowed by valuation compression. Second, the Roth facility registers resale of up to 14.10M shares; if market absorption is insufficient, it can create persistent selling pressure.

Return Conclusion

Maquina's return profile is "small principal, real robotics equity, and a few positions generating paper gains." Its portfolio return can be roughly estimated at a 1.13-1.54x unrealized multiple, depending on whether one recognizes 1X's reported valuation and Agility's de-SPAC headline. Its risks are too-small asset size, reflexive DEUS NAV, and non-redeemable SPV equity.

Robo Strategy's return profile is "large principal, SEC disclosure, underlying Level 3 assets + public-market high premium." The underlying portfolio has not yet proven large appreciation through SEC filings, but BOT stock once traded at 3.97-4.875x NAV. That premium itself is the largest source of both return and risk. Robo Strategy is more like a capital machine of "private robotics assets + public-fund premium financing" than a simple robotics ETF.

Final judgment: if the question is "who has better coverage of the first tier of humanoid robots," Maquina is better. If the question is "who has larger scale and stronger public-market financing capacity," Robo Strategy is stronger. If the question is "whose real investment returns are more verifiable," Maquina's Apptronik upside is easier to explain, while Robo Strategy's returns depend more on whether the BOT premium can persist.

Company-by-Company Analysis of Maquina and Robo Strategy Investments

This chapter is organized by companies' core business categories rather than by Maquina / Robo Strategy investment coverage. The coverage relationship is first organized in a table, then expanded by business category below, to avoid mixing together "which layer of the robotics industry chain this company belongs to" with "who invested in it and what the evidence grade is."

| Core business category | Company | Maquina coverage | Robo Strategy coverage | Investment / evidence treatment |

|---|---|---|---|---|

| Full-size humanoid, biped body, and general robot OEM | Figure AI | BOT-03 indirect fund interest at about the $350,000 level | Disclosed core holding | Covered by both; representative of non-China humanoid-robot beta |

| Full-size humanoid, biped body, and general robot OEM | Apptronik | BOT-01 / BOT-06 total investment of about $1.63M | Disclosed core holding | Shared core asset; one of the clearest sources of Maquina paper appreciation |

| Full-size humanoid, biped body, and general robot OEM | Agility Robotics | Attested holding | Not covered | Maquina target closest to a public-listing exit and order validation |

| Full-size humanoid, biped body, and general robot OEM | 1X Technologies | Attested holding, BOT-07 investment of about $800,000 | Not covered | High-upside home-robotics position, but hardest to prove |

| Full-size humanoid, biped body, and general robot OEM | NEURA Robotics | Attested holding | Not covered | European cognitive robotics and multi-product-line Physical AI platform |

| Robot foundation models, Physical AI, and manipulation policies | Skild AI | Maquina has disclosed / approved or potential SAFE, not counted in deployed cost base | Not covered | Skild Brain horizontal model layer + Fetch/Symmetry warehouse deployment-data entry; no attestation yet; if completed, it can fill the foundation-model-layer gap |

| Robot foundation models, Physical AI, and manipulation policies | Sanctuary AI | Maquina disclosed / user mNAV observation item, not verified as an attested holding | Not covered | Not counted in cost base for now; more accurately represents industrial manipulation policies, dexterous Physical AI, and software deployment on existing industrial arms rather than a pure humanoid-body position |

| Robot foundation models, Physical AI, and manipulation policies | Dyna Robotics | Not covered | Disclosed core holding, about $37.25M and about 25.31% of NAV | Robo Strategy's core alpha in robot foundation models and commercial manipulation |

| Mobile manipulation, collaborative robots, and industrial skill automation | Dexmate | Not covered | Disclosed holding, about $10M and about 6.80% of NAV | Mobile manipulation and gripper hardware-platform option |

| Mobile manipulation, collaborative robots, and industrial skill automation | Standard Bots | Not covered | Disclosed Series C Preferred, about $7M and about 4.76% of NAV | U.S. domestic collaborative-robot and SMB manufacturing-automation position |

| Mobile manipulation, collaborative robots, and industrial skill automation | Path Robotics | Not covered | Disclosed holding | Industrial welding automation and skill-automation position |

| Service, medical, defense, and consumer robotics applications | Cyan / CoCo Robotics | Not covered | Disclosed SPV / SAFE exposure | Low-speed outdoor delivery robots and fleet-operations position |

| Service, medical, defense, and consumer robotics applications | Endiatx | Not covered | Disclosed holding | Long-duration option in medical microrobotics |

| Service, medical, defense, and consumer robotics applications | Purple Rhombus | Not covered | Disclosed SPV / SAFE small-percentage asset | Defense robotics / UAS hypothesis position; public product and customer evidence is not closed-loop |

| Service, medical, defense, and consumer robotics applications | REK | Not covered | Disclosed early-stage asset | Observation position in robotics entertainment, competition, teleoperation, or consumer experience |

| Computing power, manufacturing materials, market infrastructure, and targets pending verification | GMI Computing | Not covered | Disclosed SAFE exposure | Physical AI computing-adjacent asset; not counted as robot-body coverage |

| Computing power, manufacturing materials, market infrastructure, and targets pending verification | Nox Metals | Not covered | Disclosed small-percentage holding | Advanced manufacturing and materials-adjacent asset; robotics supply-chain relevance needs verification |

| Computing power, manufacturing materials, market infrastructure, and targets pending verification | Allonic | Not covered | Disclosed small-percentage early holding | Early robotics infrastructure / structural-innovation option; information remains limited |

| Computing power, manufacturing materials, market infrastructure, and targets pending verification | Robotico | XMAQUINA / DEUS Labs first incubation; official pre-seed 20% equity allocation disclosed, but no Andersen attestation / amount / transaction documents, so not counted in attested cost base | Not covered | Humanoid robotics market intelligence, index, RCM distribution, and capital-market transparency infrastructure; not a robot body |

| Full-size humanoid, biped body, and general robot OEM | Genki Robotics | User mNAV once showed about 5.4% basis, not attested; website/LinkedIn show it is positioned as mission-critical humanoid robots, with investors self-disclosed by the company but no financing details | Not covered | Stealth / early full-size humanoid watchlist; not counted in attested cost base or coverage rate |

If names such as Skild AI, Robotico, Sanctuary AI, and Genki appear in Maquina with only governance, ecosystem, user-form, or unauthenticated signals, they are not counted in deployed equity cost base. But because Maquina has publicly mentioned them or related research has already formed, this chapter still keeps them as separate company sections.

Path Robotics, REK, GMI Computing, Cyan / CoCo Robotics, Nox Metals, Endiatx, Allonic, Purple Rhombus and similar names are small/mid-sized positions disclosed by Robo Strategy for which local research does not yet have company deep dives of the same grade.

Full-Size Humanoid, Biped Body, and General Robot OEM

Figure AI

Company Background and Founding Team

Figure AI is a U.S. humanoid robotics company founded by Brett Adcock. It is not a single hardware company; it is simultaneously betting on four things: the Figure 03 body, the Helix embodied model, the BotQ manufacturing system, and the enterprise-scenario data closed loop. In September 2025, its Series C financing exceeded $1B, with a post-money valuation of about $39B. Investors included Parkway, Brookfield, NVIDIA, Macquarie, Intel, LG, Salesforce, T-Mobile, Qualcomm and others. Both Maquina and Robo Strategy have Figure AI exposure, but their entry bases differ: Robo Strategy has a larger-scale direct/fund-like holding, while Maquina BOT-03 is an indirect fund interest at about the $350,000 level.

From an investment perspective, Figure is the non-China humanoid-robotics target with the "highest valuation, strongest industrial partners, and also the greatest execution pressure." Its core question is not whether it has demos, but how quickly enterprise deployment, manufacturing yield, robot uptime, and unit economics all need to work behind a $39B valuation.

Product Lines and Business Model

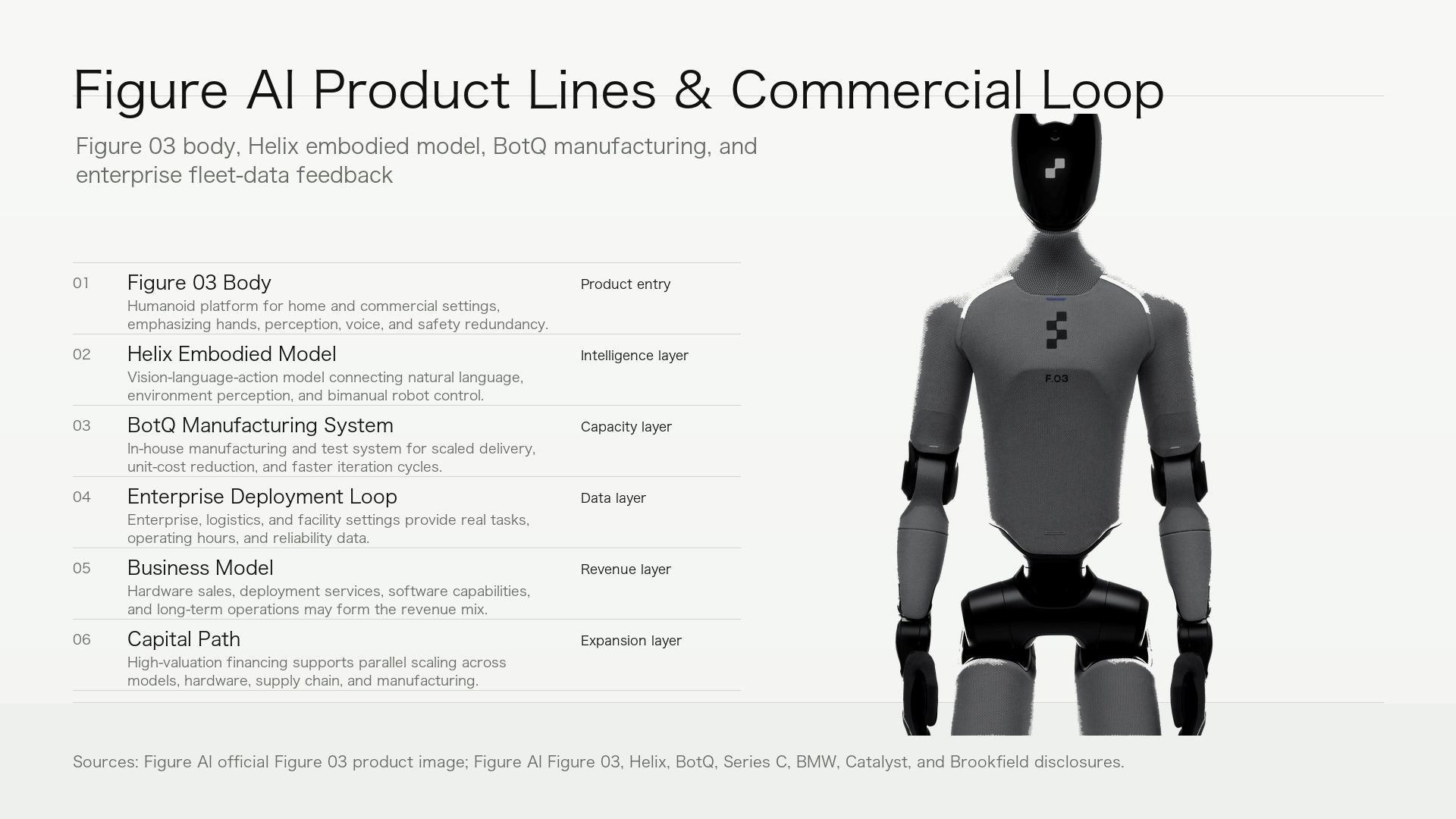

Figure's product line should not be understood as "four product layers." A more accurate decomposition is: body product generations are Figure 01, Figure 02, and Figure 03; the current true external commercialization carrier is the Figure 03 body; Helix is an embodied model embedded in the body and iterated with fleet data; BotQ and the enterprise-scenario data closed loop are manufacturing and commercialization infrastructure, not separate product lines.

Illustration: the product image on the right uses Figure AI's official Figure 03 product image. Structure and data sources are Figure AI website disclosures on Figure 03, Helix, BotQ, Series C, and BMW / Catalyst / Brookfield.

- Figure 01: early prototype, used to validate the full-size humanoid platform and motion capabilities.

- Figure 02: a generation of work robot for industrial pilots; public materials show it entered BMW scenarios. NVIDIA disclosed that Figure 02 uses Omniverse / Isaac Sim, NVIDIA GPUs, and six RGB cameras, and achieves about 3x inference improvement versus Figure 01 through a second NVIDIA RTX GPU.

- Figure 03: current main platform, about 5'8" tall, about 20 kg payload, about 61 kg weight, about 5 hours of battery life, and about 1.2 m/s speed. Figure 03's focus is not exterior iteration, but redesign for Helix, home scenarios, commercial scenarios, and mass manufacturing, including fewer parts, moldability, internal battery/actuator/sensor modules, and adaptation to the BotQ line.

Helix / Helix 02 is Figure's vision-language-action model and robot-control intelligence. It should not be listed alongside Figure 01/02/03 as a body product generation. Early Helix's upper System 2 performs high-level understanding and action planning at about 7-9 Hz, while lower System 1 performs motion control at about 200 Hz. Helix 02 adds a roughly 1 kHz System 0 for whole-body balance, contact, and low-level control. In other words, Figure 03 is the body, Helix is control and generalization capability, and enterprise-site data in turn trains and validates Helix.

In terms of business model, Figure currently looks more like an "enterprise robot fleet operator" than a pure robot seller. Its closed loop is: Figure 03 enters enterprise scenarios such as BMW, Catalyst Brands, and Brookfield; real tasks generate data; data feeds back into Helix; BotQ improves body manufacturing, quality, and delivery capability; more deliverable robots then enter more enterprise scenarios. Revenue may come from enterprise deployments, robot leasing or sales, Fleet Management / OTA, customer integration, operations and maintenance, and the data closed loop. But public materials have not yet disclosed unit price, lease fee, SLA, gross margin, customer contract amount, or backlog. Therefore, Figure's commercial quality still needs to be validated through the scale of paying customers, robot uptime, task success rate, human takeover rate, and fleet repeat purchase.

Upstream Supply-Chain Vendors

Figure's supply chain has a clear tendency toward "key module internalization." Under the Figure 03 basis, actuators, batteries, sensors, structural parts, and electronics all emphasize self-development or internal design, while BotQ is the core of its manufacturing scale-up. BotQ's first line targets annual capacity of up to 12,000 units. The company has disclosed that more than 350 Figure 03 units have been delivered from BotQ into internal/external fleet categories, that line demonstrations reached a cadence of about 1 unit/hour, and manufacturing signals such as 9,000+ actuators, 500+ battery packs, 80+ EOL functional tests, 50+ in-process inspection points, and a 99.3% first-pass yield on the battery line.

Among external upstream partners, NVIDIA is the clearest key partner: Omniverse / Isaac Sim for simulation, H100 and other training infrastructure for model training, RTX GPUs for body inference, and Figure is also within the NVIDIA Humanoid Robot Developer Program ecosystem. Brookfield is more of a data/scenario/infrastructure partner and should not be misread as a BOM supplier.

Supply-chain nodes still requiring penetration include harmonic/planetary/cycloidal reducers, motor magnetic materials and windings, encoders, hand tactile sensing, camera modules, battery cells, wire harnesses, structural parts, PCBs, thermal management, safety controllers, field repair parts, and yield-ramp cadence. If Figure internalizes all key BOM, potential gross margin and control are stronger, but capex, manufacturing-failure risk, and after-sales pressure also become more concentrated.

Downstream Buyers, Revenue, and Orders

Figure's downstream validation mainly comes from three types of scenarios:

- BMW: a commercial agreement was reached in 2024, with Figure 02 participating in production tasks in BMW scenarios. Public research materials mention that Figure 02 supported BMW vehicle-assembly-related processes in 2025, while Figure 03 entered BMW Spartanburg's Hall 52 for more complex logistics tasks such as sequencing / logistics.

- Catalyst Brands: Figure disclosed a deployment agreement with Catalyst Brands, targeting the Distribution Logistics Center in Reno, Nevada. Catalyst's brands include JCPenney, Aeropostale, Brooks Brothers and others.

- Brookfield: the collaboration focuses on real-world humanoid-robot pretraining data and potential deployment spaces. Brookfield's asset pool includes residential, office, and logistics real estate. The theoretical scenario space is huge, but for now it should be viewed more as a scenario and data entry point than a confirmed order.

On revenue quality, Figure has not yet disclosed robot unit price, lease fee, gross margin, recognized revenue, customer payment scale, or renewals. Its advantages are very strong capital, brand, enterprise partners, and manufacturing ambition. The risk is that the valuation has already priced in "BotQ can mass-produce + Helix can generalize + enterprises are willing to pay at large scale." For Maquina / Robo Strategy, Figure is the position that best represents non-China humanoid-robot beta, but it is not the position easiest to verify with financial metrics.

Apptronik

Company Background and Founding Team

Apptronik originated from the University of Texas at Austin Human Centered Robotics Lab and has long participated in projects such as NASA Valkyrie. Its DNA is more engineering-, hardware-, industrial-deployment-, and enterprise-customer-oriented than Figure's. It does not start from consumer-level imagination, but from definable tasks in logistics, manufacturing, retail, automotive and similar scenarios. Maquina and Robo Strategy both hold it, making it a shared core asset for the two.

In financing and valuation, Apptronik's appreciation path is very clear: 2022 Seed of about $14.6M, post-money about $53.4M; 2023 Seed Plus of about $13.9M, post-money about $101.7M; February 2025 Series A of about $350M, post-money about $1.75-1.78B; October 2025 Series A extension bringing total to about $403M; after 2026 Series A-X1/X2, total Series A funding exceeded $935M, post-money about $5B, with media basis mentioning above $5.5B. Maquina BOT-01 / BOT-06 invested about $1.63M in total, making it one of Maquina's most important potential book-value appreciation sources.

Product Lines and Business Model

Apptronik's core product is Apollo. Its product generations and commercial route lean more toward enterprise pilots to fleet deployment: